We view any equity weakness (possible) post-March CPI as chance to BTD given magnitude of "trapped bears" and softening inflation trends

On the eve of the March CPI report (released on 4/12 at 8:30am ET), few investors have conviction on what to expect from the actual report — in other words, most are “flat” going into a report with an uncertain outcome.

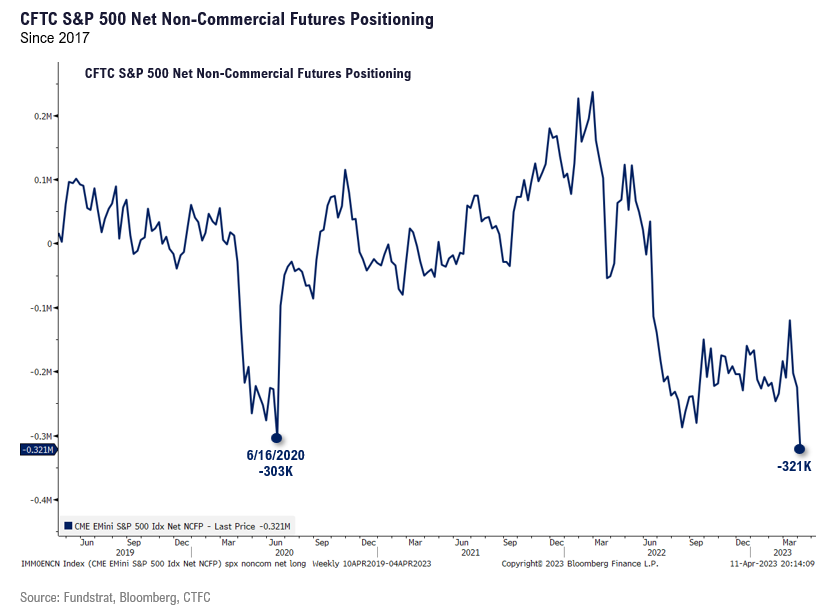

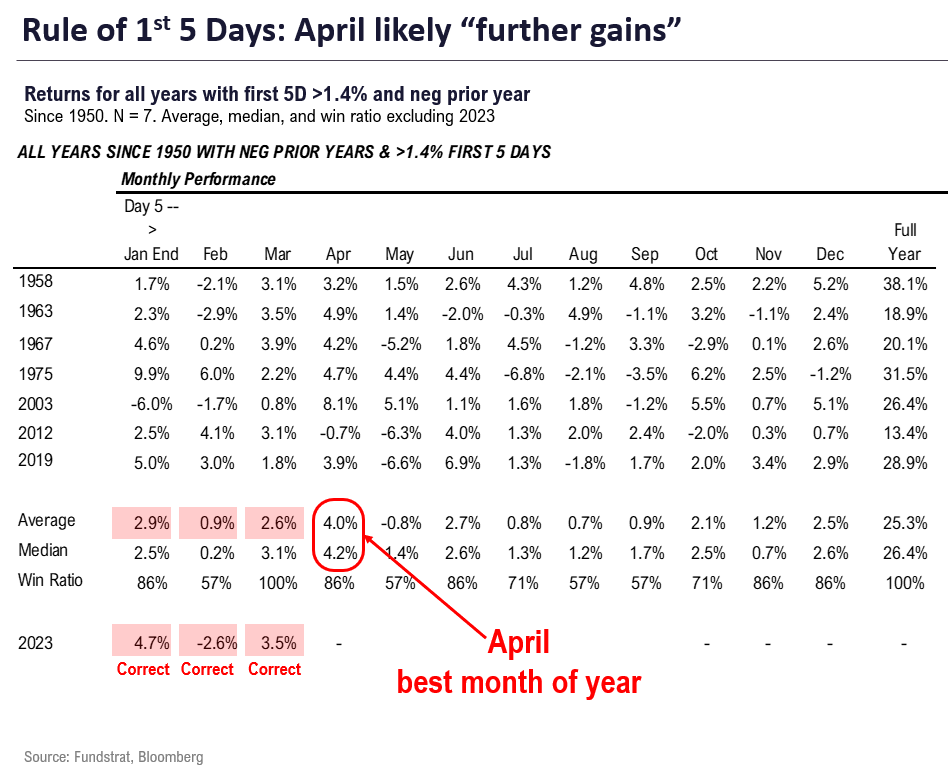

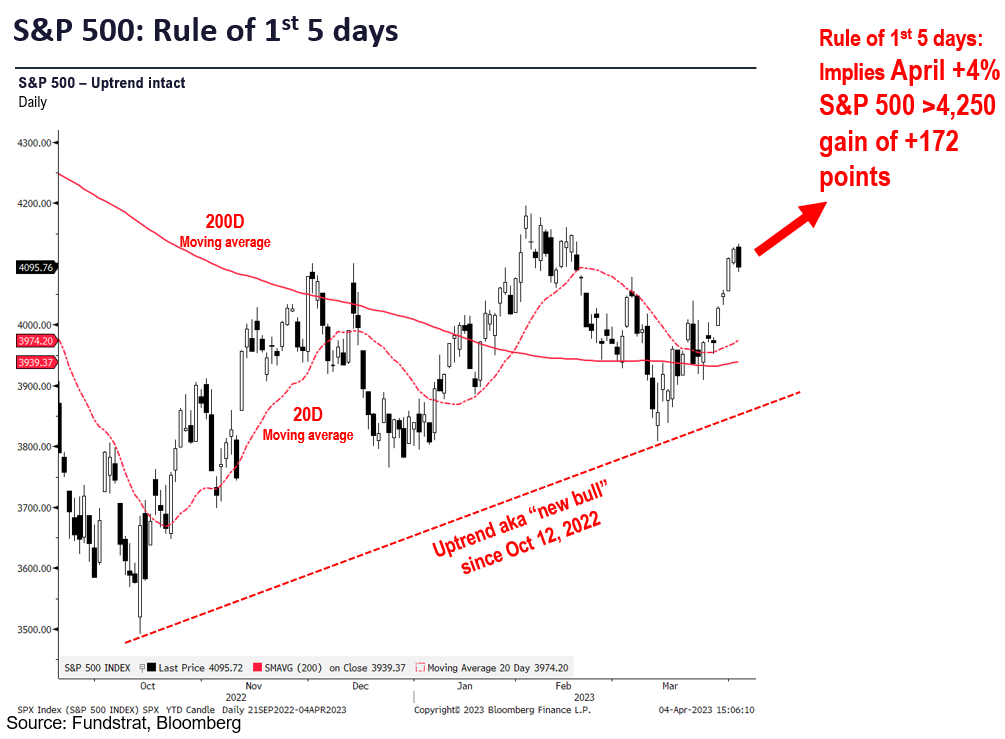

- On the other hand, investor positioning still leans negative. This was discussed Monday by our Head of Technical Strategy, Mark Newton, who showed speculative S&P 500 futures net positioning is the most negative since 2011. That is a 12-year high. Wow. Moreover, the seasonals are positive with April expected to post a median +4% gain (83% win-ratio) based upon the “rule of 1st 5 days” and is the strongest month of the calendar year.

- We see March CPI’s report as another possible catalyst for the “trapped bears” to cover their short positioning. And this could in turn, create a sizable upside equity rally. This is something that Newton has referred to in his report Monday, noting that in the short-term this could push the S&P 500 above 4,200 and then some.

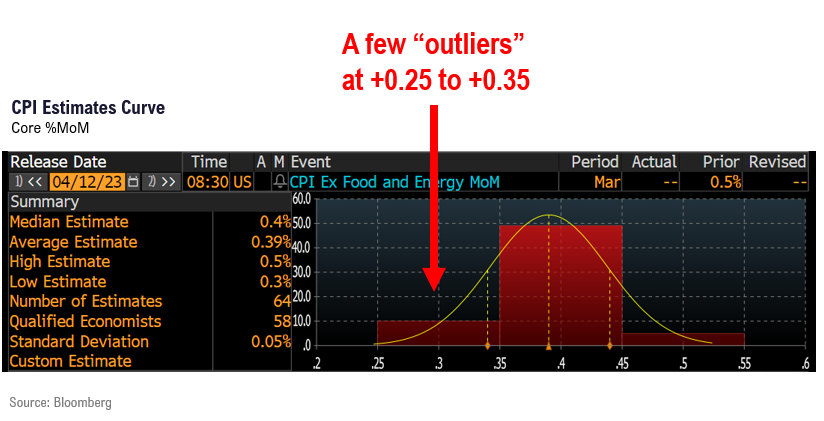

- Street consensus (per Bloomberg, 64 estimates) is +0.39% Mar Core MoM (+0.5% Feb) and Mar YoY of +5.6% (+5.5% Feb). And there are 10 of 64 with an estimate between +0.25% and +0.35%, so there are a fair number expecting a downside read. The widely followed UBS economist, Samuel Coffin, expects +0.4%, or consensus. The less reliable Cleveland Fed InflationNOW forecast is +0.45% for core.

- Why isn’t a +0.4% (4.8% annualized) a bad outcome? We expect the bulk of this rise to be driven by shelter/owners equivalent rent, which is a lagged measured and we do not believe is reflective of the prevailing trend in inflation. After all, as we pointed out last week, consumers see inflation at +3.6%, while official CPI is considerably higher at >5%. Who is right? Our base case remains that inflationary pressures are easing faster than consensus expects (Jan was the only “hot inflation” print since Oct 2022) and the credit tightening post-SVB failure will further weaken inflation.

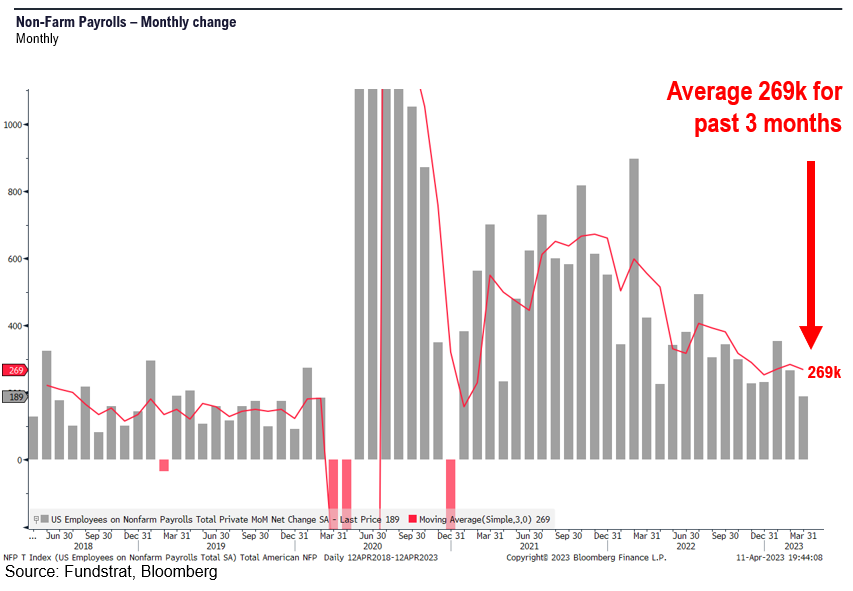

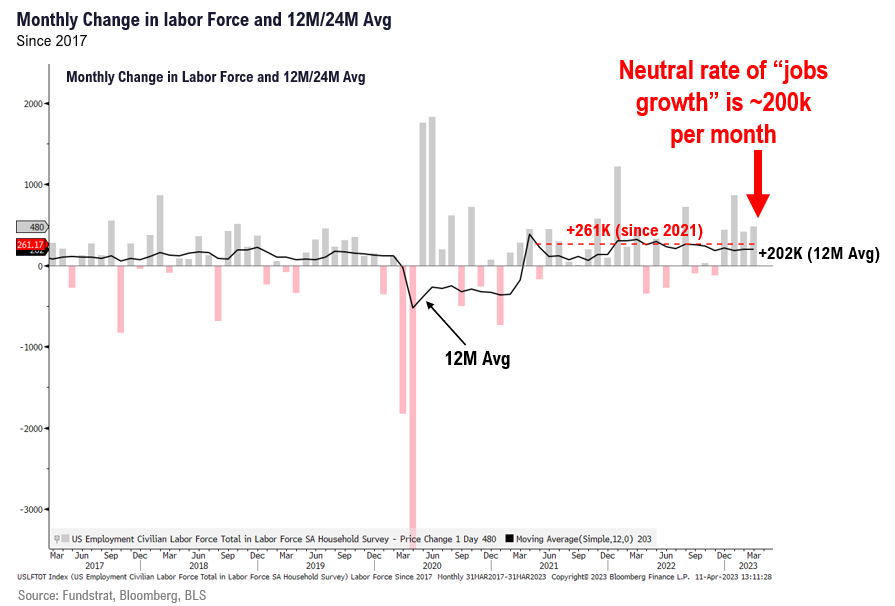

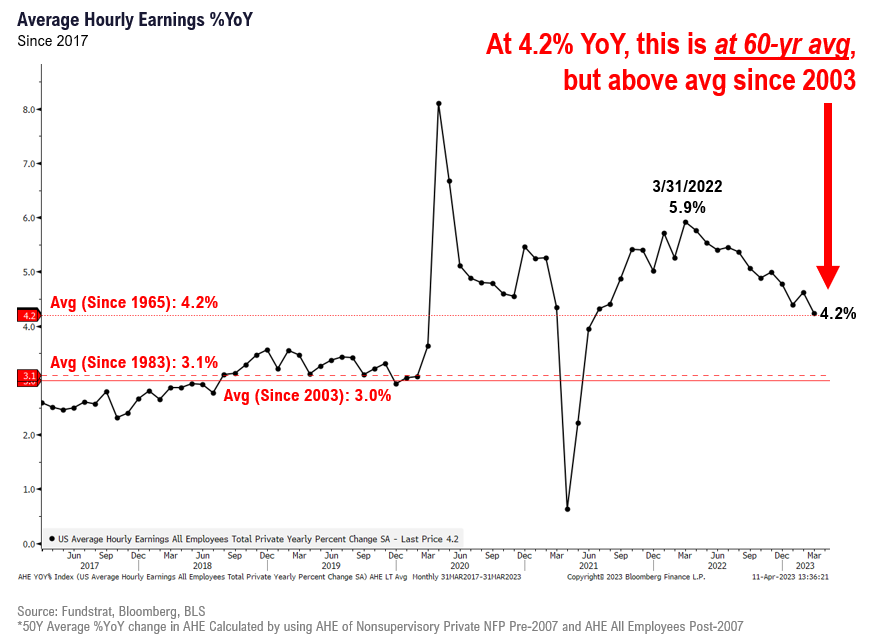

- In fact, the March jobs report (last Fri) showed average hourly earnings growing at 4.2%, the lowest since mid-2021 and now sitting at the long-term average since 1965. And the 3-month average for NFP (private) is +269k, which is only a touch above 202k avg increase in labor force (household survey). Thus, the labor market is coming back into alignment, easing the last of the labor market pressures. In fact, in the March report, the monthly increase in labor force was an even stronger +480k.

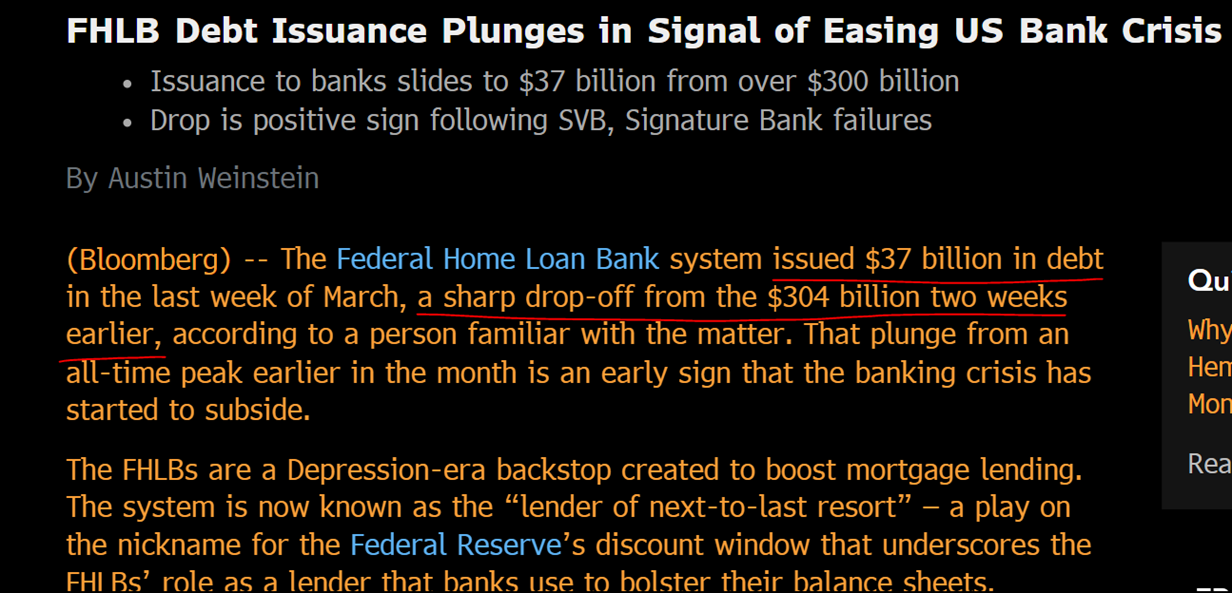

- Fed officials are splintering in their views on whether further rate hikes are necessary. The latest to weigh in is Chicago Fed President Austan Goolsbee, who urged “we need to be cautious.” The bank crisis continues to fester, which is a new uncertainty for Fed officials and economists. The most visible remains First Republic (FRC) but others as well. The good news FHLB debt issuance (which corresponds to borrowings by regional banks) was $37 billion in the past week, compared to $304 billion the week prior. So there are some signs part of the crisis is ebbing.

- This is what the bond market has been communicating as well. The US 2-yr yield is 4.02%, which is 83bp lower than the current Fed Funds midpoint. The bond market is saying the Fed is done raising rates. And we think this is where consensus views ultimately converge.

- If the Fed is done raising rates sooner (our view), we think this also means the Fed will tolerate further easing of financial conditions. This will be particularly likely if markets worry about credit tightening as CRE and CMBS and other commercial lending markets show stress. And thus, those “higher for longer”-ites will be capitulating. And those generally in the “higher for longer” are also in the bearish camp for equities.

Bottom line. We believe bears remain trapped and April is going to be a generally strong month (based upon “rule of 1st 5 days”). Month to date, April is flat, but March was similarly back-ended. We would use any weakness from a post-March CPI sell-off to add to equity exposure. And we continue to favor Technology, Energy and Industrials (XLK -0.25% , QQQ -0.07% , XLE 1.37% , OIH 0.67% and XLI 0.11% ).

MARCH CPI: +0.40% is the “uncertain” consensus

March CPI consensus forecasts are shown below.

- Street consensus (per Bloomberg, 64 estimates) is +0.39% Mar Core MoM (+0.5% Feb) and Mar YoY of +5.6% (+5.5% Feb).

- The YoY is accelerating, but part of this is due to prior revisions. The higher months in 2022 were April, May and June and those get dropped beginning next month.

- There are 10 of 64 with an estimate between +0.25% and +0.35%, so there are a fair number expecting a downside read.

- The widely followed UBS economist, Samuel Coffin, expects +0.4%, or consensus.

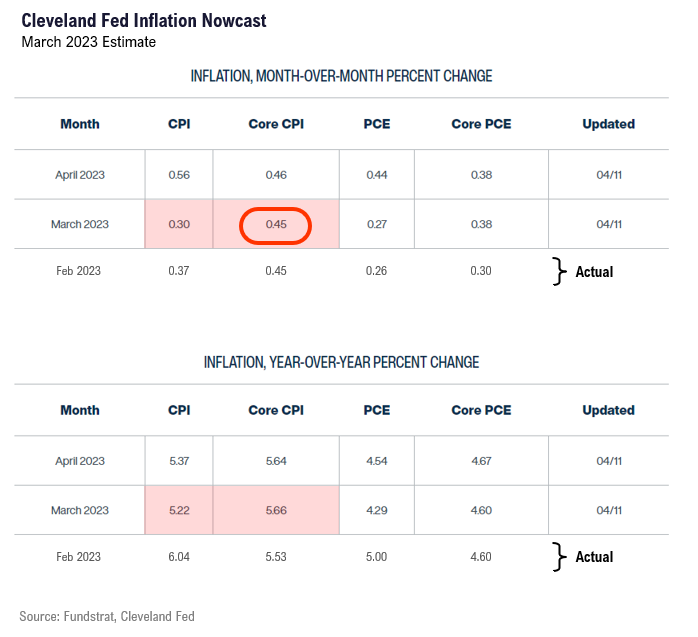

The less reliable Cleveland Fed InflationNOW forecast is +0.45% for core

FED PAUSE: The case for continuing to raise rates is not clear cut

As we noted above, Fed officials are splintering in their views on whether further rate hikes are necessary. As the WSJ article below notes, the latest to weigh in is Chicago Fed President Austan Goolsbee, who urged “we need to be cautious.”

- In his speech to the Economic Club of Chicago, Goolsbee says “At moments like this of financial stress, the right monetary approach calls for prudence and patience,”

- Financial crises create uncertainties, and it is logical for Fed officials to be wary. And in turn, we expect them to be more tolerant of easing financial conditions.

The bank crisis continues to fester, which is a new uncertainty for Fed officials and economists. The most visible remains First Republic (FRC) but others as well. The good news FHLB debt issuance (which corresponds to borrowings by regional banks) was $37 billion in the past week, compared to $304 billion the week prior. So there are some signs part of the crisis is ebbing.

MARCH JOBS (4/7): Moving to neutral rate of growth

We see encouraging details in the March jobs report (last Fri):

- average hourly earnings growing at 4.2%, the lowest since mid-2021 and now sitting at the long-term average since 1965.

- And the 3-month average for NFP (private) is +269k and down from an average >500k last year this time.

- And labor supply is growing at 202k avg (household survey).

- This means the labor market is coming back into alignment, easing the last of the labor market pressures.

The labor supply is still growing at 200k-250k per month and as shown below, seems to be slightly higher recently.

- in the March report, this figure grew +480k

And it is good to see average hourly earnings ease further. The most recent figure is 4.2%, the lowest since mid-2021 and right on top of the average since 1965.

- it is not clear where Fed would target this AHE

- but since 2003, this figure was 3%, so a figure with 3-% in it would likely be where Fed can take a breath.

ECONOMIC CALENDAR: Key is inflation, and April so far is “tame”

And the key data to watch in April is below. But as shown, so far, the cadence of the data has been tame, or dovish.

Key incoming data April

4/3 10am ISM Manufacturing Employment/Prices Paid MarchTame4/4 10am ET JOLTS Job Openings (Feb)Tame4/7 8:30am ET March employment reportTame- 4/12 8:30am ET CPI March

- 4/12 2pm ET March FOMC Minutes

- 4/13 8:30am ET PPI March

- 4/14 7am ET 1Q 2023 Earnings Season Begins

- 4/14 Atlanta Fed Wage Tracker March

- 4/14 10am ET U. Mich. March prelim 1-yr inflation

- 4/19 2:30pm ET Fed releases Beige Book

- 4/28 8:30am ET PCE March

The key data reported in March (Feb data) was overall dovish as it showed softer inflation.

Key incoming data for March 2023

3/7 10 am ET Powell testifies SenateHawkish3/8 10am ET Powell testifies HouseNeutral3/8 10am ET JOLTS Job Openings (Jan)Semi-strong3/8 2pm ET Fed releases Beige BookSoft3/10 8:30am ET Feb employment reportSoft3/13 Feb NY Fed survey inflation exp.Soft3/14 6am ET NFIB Feb small biz surveySoft

3/14 8:30am ET CPI FebTame3/15 8:30am ET PPI FebTame3/17 10am ET U. Mich. March prelim 1-yr inflationBIG DROP3/22 2pm ET March FOMC rate decisionDOVISH3/31 8:30am ET Core PCE deflator FebTame3/31 10am ET U Mich. March final 1-yr inflationTame

BEARS TRAPPED: Speculative futures shorts highest since 2011.

Our Head of Technical Strategy notes that speculative net positioning on S&P 500 futures is the most short since 2011 at 321,000 contracts. This exceeds even the COVID lows.

And BofA Prime Brokerage report shows a similar negative positioning. Investors are betting equities will fall short-term.

- thus, we think if CPI is tame, this would amplify the pain on bears, given the skew in positioning.

STRATEGY: Cyclicals outperforming more than Defensives

We have highlighted the 2-yr relative performance of the major groups below and as shown, the leadership is more cyclical.

- Leading are Tech/FAANG, Energy, some Industrials, Materials and Staples.

- The drags on S&P 500 performance have been Utilities, Financials, Telecoms and Healthcare.

- In other words, the drags have been largely Defensives.

- This is counter to those saying this rally in 2023 is Defensive stocks.

And our base case for April remains a strong >4% rally, following the pattern of “Rule of 1st 5 days.” The Rule of 1st 5 days looks at years when S&P 500 gains >1.4% in 1st 5 days and is negative the prior year.

- This has happened 7 times since 1950: 1958, 1963, 1967, 1975, 2003, 2012 and 2019.

- Based upon those 7 years, April implied gain is +4.2% and was positive 6 of 7 times (only 2012, -0.7%). This implies +175 points, or S&P 500 >4,275 by the end of April.

A gain of 4%, or +172 points would put S&P 500 >4,250 by the end of the month. And we think this would ultimately force a bear capitulation.

We publish on a 3-day a week schedule:

Monday

SKIP TUESDAY

Wednesday

SKIP THURSDAY

Friday

_____________________________

37 Granny Shot Ideas: We performed our quarterly rebalance on 1/30. Full stock list here –> Click here

______________________________

More from the author

Articles Read 1/2

🎁 Unlock 1 extra article by joining our Community!

Stay up to date with the latest articles. You’ll even get special recommendations weekly.

Already have an account? Sign In b27700-4decd1-70545f-2d27c8-f48cd2

Already have an account? Sign In b27700-4decd1-70545f-2d27c8-f48cd2