Markets Troubled by Inflation Data, End Weekly Win Streak

Our Views

- Tuesday’s selloff in equities is the largest decline of 2024 so far, after Jan CPI came in “hot” vs consensus with Core CPI +0.39% (vs consensus +0.30%). While Tuesday’s decline was indeed large, this simply takes us to prices 4 trading days ago — in other words, this is a mild retracement of recent gains:

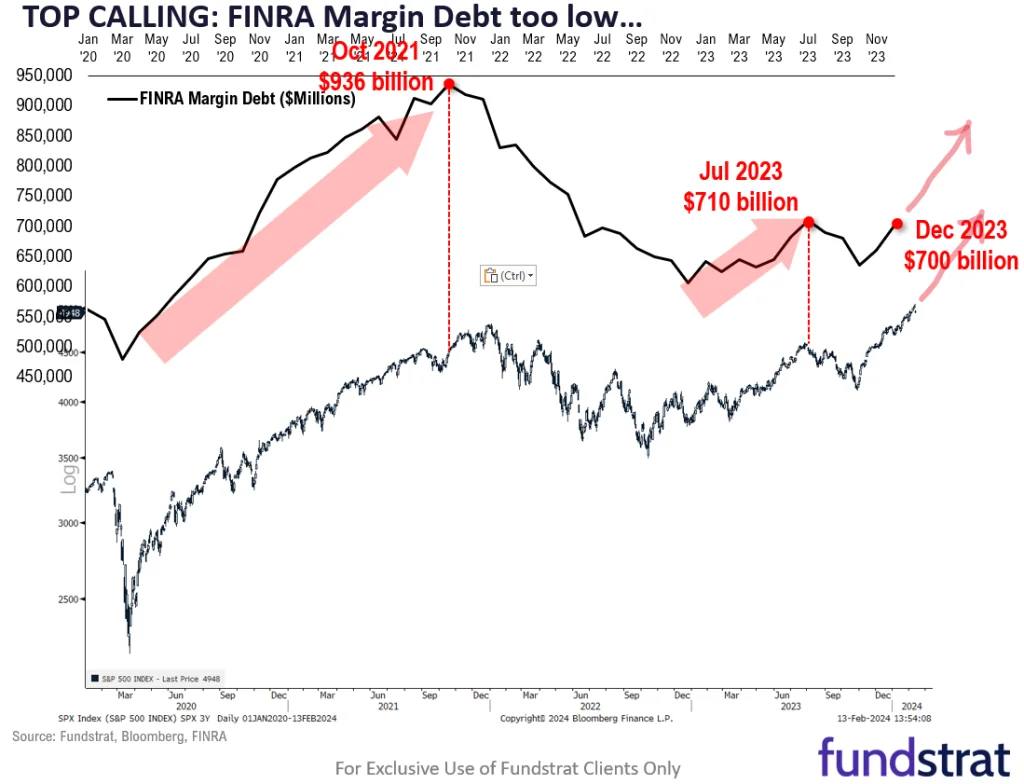

- Is this the peak for equities in the first half of 2024? In our view, this is not likely. There is still too much dry powder, with margin debt still below July 2023 levels. In addition, sentiment is still skeptical, in my view.

- We think the trend in inflation is still lower. Yes, even after Tuesday’s CPI report. Core CPI is still tracking lower and there is noise in Tuesday’s report.

- Consider this: Core CPI MoM Jan came in at +0.39%. Shelter CTG (contribution to growth) was +0.26%, while Auto insurance CTG was +0.05%. So just excluding those two items, Core CPI was at +0.08%, or +0.96% annualized. It is still falling like a rock.

- Bitcoin’s performance relative to other risk assets following a hot CPI print was a great example of how passive ETF flows can affect the way that BTC trades in a post-ETF world.

- Altcoins have seen gains from recent capital inflows, resulting in expanded market breadth. However, when market breadth is measured in BTC, it continues to decline, signaling a market led by Bitcoin. This is typically characteristic of the earlier phases of a market cycle and bodes well for continuation higher in alts.

- Older wallets, who presumably purchased at a lower cost basis, have begun selling their BTC. While this might appear bearish on the surface, it signifies strength and is a characteristic feature of every previous bull market cycle.

- With an impending cliff unlock for ARB, nearly equivalent to the current circulating supply, we anticipate strength leading up to the Dencun upgrade. However, our assessment of the risk/reward equation suggests it will be prudent to de-risk on any significant rally prior to the unlock.

- Thus far this week we have seen nearly $2 billion in net inflows across all BTC ETF products, and continued creations within the stablecoin market.

- Core Strategy – Our Q1 outlook anticipated some headwinds, and it seems the initial turbulence has subsided for now. Flows into crypto remain strong and breadth against BTC remains subdued. We maintain that ETH, L2s, and STX offer compelling idiosyncratic upside due to their near-term catalysts. Further, we have no reason to fade the recent strength out of SOL.

- The seat vacated with Republican George Santos’s expulsion from the House of Representatives has returned to the Democrats with this week’s victory of Tom Suozzi.

- Suozzi had previously won the seat in 2020 before losing it to Santos in 2022; the district has a solid Republican machine but has generally gone for Democrats at the national level.

- With the Presidents’ Day recess, both houses of Congress will return just three days before the first of two government shutdown deadlines.

Wall Street Debrief — Weekly Roundup

Key Takeaways

- The S&P 500 slipped 0.42% this week, ending at 5,005.57. The Nasdaq also retreated, down 1.34% to close the week at 15,775.65. Bitcoin reached $51,844 late on Friday afternoon, up 7.29% since Monday.

- Anecdotal evidence suggests continued nervousness in the market.

- Despite hotter-than-expected CPI and PPI, the market still has near-term upside, according to Fundstrat Head of Research Tom Lee.

“I am not ready to back away from my views.” ~ Alexei Navalny (1976 - 2024)

Good evening,

The primary macroeconomic event impacting markets this week was the release of the latest Consumer Price Index (CPI) reading. As we began the week, Fundstrat Head of Research Tom Lee told us that, anecdotally, based on his conversations with clients, RIAs, and investors at various industry events, uncertainty seems to be pervasive.

He highlighted two common perspectives: “nervous bulls” who realized gains during the present 15-week rally, and “angry bears” who are unhappy with the disconnect between the market’s behavior and what they believe it should have been. “Based on our multiple interactions, the predominant view is that of the angry bears” who see the Fed’s stance and the market’s behavior (based on trading activity) as misaligned.

Yields are up – the 10-year has risen to its highest level in months (4.295% as of Friday afternoon) – yet, as Head of Technical Strategy Mark Newton had noted in past weeks, the traditional correlation between stocks and yields has not been in evidence recently, as stocks have risen alongside yields. To Lee, this is a sign of market strength. Yet, Lee continues to urge caution as long as the timeframe for the Federal Reserve’s anticipated rate cuts remains unclear, amplifying nervousness and uncertainty.

They were certainly in evidence on Tuesday, when CPI came in hot vis-à-vis consensus. The latest read showed inflation continuing to decline, but not as quickly as the Street had expected. Many – economists, pundits, and investors – suggested that this could cause the Fed to delay rate cuts, and the day ended with the S&P 500 down about 2%. Lee responded, “In our view, this is an over-reaction to a single CPI print. Markets might panic, the Fed might hesitate, but if you peel the onion, [this CPI print] is not that bad.”

He was not alone. During a speech the next day at the Council on Foreign Relations, Chicago Fed President Austan Goolsbee said, “Let’s not get too flipped out,” later urging observers not to get “amped up when you get one month of CPI that was higher than you expected it to be.”

Consistent with the assessments Lee has been making for months, Goolsbee stressed that “it’s totally clear that inflation is coming down [...] We can still be on the path [to the Fed’s target inflation of 2%] even if we have some increases and some ups and downs.”

What does that mean for equity investors? In his 2024 Outlook Lee had warned that, although the market would likely hit new highs in January, a brief period of consolidation could follow before another rally in the second half of the year. Was the hot CPI print the catalyst to mark a short-term top?

“We don’t think so,” Lee said. “Near-term peaks are usually marked by a sell-off on good news,” he said, “and that’s not what happened on Tuesday.” And on Friday, when PPI came in hot, stocks barely slipped. Based on this, “we think stocks have upside in the near-term,” he told us.

Lee also observed that peaks usually happen after buying power is exhausted. The July 2023 top was preceded by a peak in margin debt, and current margin debt is still below those levels. “These levels need to surge to mark a near-term top,” Lee said. This is shown in our Chart of the Week:

Elsewhere

The U.S. Patent and Trademark Office has ruled that inventions created primarily with AI tools such as generative AI cannot be patented. An invention can only be patented if a human made a “significant contribution” to it, and only a human can hold a patent. As an example, “a natural person who only presents a problem to an AI system” such as merely asking a generative AI to create a design “may not be a proper inventor of something,” according to the USPTO. “However, a significant contribution could be shown by the way the person constructs the prompt in view of a specific problem to elicit a particular solution from the AI system.”

UK headline inflation YoY stayed constant in January, matching the 4% seen in December. The Office for National Statistics also reported that YoY core inflation, defined as excluding energy, food, alcohol, and tobacco, remained unchanged, at 5.1%. Core CPI MoM was -0.9%. All three measures came in below consensus expectations.

The University of Pennsylvania announced a new undergraduate degree in artificial intelligence. It will be the first such degree offered by an Ivy League university and will become an option for students this fall. Required coursework will cover Machine Learning, Vision & Language, and Optimization & Control. Other schools offering such a degree include computer-science powerhouse Carnegie Mellon University and Purdue University, an engineering mainstay.

Microsoft and OpenAI said hackers linked to the governments of Russia, China, and Iran have used OpenAI’s ChatGPT to carry out attacks. This includes using the chatbot to generate phishing scripts and realistic human responses, write code, research cybersecurity tools, and identify human targets. In its report, the companies identified cyberwarfare groups linked to Russian intelligence, Iran’s Revolutionary Guard, and the governments of China and North Korea. A Chinese spokesperson described Microsoft’s allegations as “groundless smears and accusations.”

The first-ever private lunar lander was launched this week, and if it lands successfully on February 22, the goal is to put the first human-made artwork on the moon. An unmanned Nova-C lander made by Intuitive Machines, launched aboard a SpaceX Falcon 9 rocket, is expected to deliver not just NASA scientific equipment, but also 125 one-inch-high Jeff Koons sculptures of moon phases representing historic figures such as Mozart, Cleopatra, Gandhi, da Vinci, and the Starman otherwise known as David Bowie.

Japan slipped into recession and fell in the rankings of the world’s economies by size. After recording annualized GDP growth of -0.4% in 4Q2023 and -3.3% in 3Q2023, Japan is no longer the third-largest economy in the world – Germany is.

And finally: Britons are feeling the pain from Houthi attacks in the Red Sea, which have disrupted shipments of tea, causing a tea shortage. “This is a critical period which requires our constant attention,” said Tetley Tea, one of the most popular brands in the United Kingdom. Some observers have suggested that panic-buying by “cuppaholics” had exacerbated the shortage in much the same way panic-buying contributed to toilet-paper shortages during the pandemic.

Notice: U.S. markets and Fundstrat offices will be closed on Monday, February 19, 2024 in observance of Presidents’ Day. There will be no publications that day.

Important Events

The minutes from the January 31, 2024 FOMC meeting.

Prev. -0.15

An assessment of overall economic activity and potential inflation, based on a weighted average of 85 existing monthly indicators of national economic activity.

Est.: 52.1 Prev.: 52.5

A gauge of business activity based on a survey of approximately 400 companies in the service sector.

FS Insight Media

Stock List Performance

| Strategy | YTD | YTD vs S&P 500 | Inception vs S&P 500 | |

|

Granny Shots

|

+8.07%

|

+3.13%

|

+106.94%

|

View

|

Articles Read 1/2

🎁 Unlock 1 extra article by joining our Community!

Stay up to date with the latest articles. You’ll even get special recommendations weekly.

Already have an account? Sign In cf01cf-b95eed-eb9b41-23848a-3ef12e

Already have an account? Sign In cf01cf-b95eed-eb9b41-23848a-3ef12e