A daily market update from FS Insight — what you need to know ahead of opening bell

“You have to stay alert. You’ve got to keep raising your game.” ~ Larry Wilmore

Overnight

The International Monetary Fund projects that U.S. economic growth of 2.7% for 2024, more than double the growth rate of any other G-7 country. (FT)

UK headline inflation fell to 3.2% in March, higher than the 3.1% economists expected but still the lowest it’s been since September 2021. (AP)

Hedge funds pile into Mexican peso, fueling a rally that has made it one of the best-performing currencies in the world (BBG)

The House has delivered two articles of impeachment against Homeland Security Secretary Alejandro Mayorkas to the Senate. (CNN)

President Biden reportedly plans to call for tariffs on Chinese steel to triple, in part to garner support in the swing state of Pennsylvania. (FT)

VC firm Andreessen Horowitz has raised raises $7.2 billion to identify and invest in generative AI start-ups, sparking hopes that the tech-startup environment might begin recovering. (FT)

An EU court has ruled that the name of the late Colombian drug lord Pablo Escobar cannot be trademarked because it goes against “accepted principles of morality.” (Politico)

A second House Republican, Thomas Massie (Kentucky), has joined Marjorie Taylor Greene (Georgia) in supporting a motion to oust House Speaker Mike Johnson, after Johnson announced plans to separate foreign aid proposals into separate bills. (Guardian)

Treasury Secretary Janet Yellen says new sanctions against Iran to be unveiled in “coming days” (BBC)

Some experts see signs of disunity and disagreement among the three most senior Israeli wartime decision makers, Prime Minister Benjamin Netanyahu, Defense Minister Yoav Gallant and the former head of the Israeli military, Benny Gantz. (WSJ)

Dubai saw its heaviest rainfall in recorded history, getting six inches of rain in a 24 hour period – about 1.5 times what it usually gets in an entire year, enough to shut the city down. (AP)

A brawl broke out in Georgia’s parliament during a debate over a proposed ‘foreign influence’ or ‘Russian law that critics said would suppress free speech and dissent. (BBC)

Microsoft announced a $1.5 minority-stake investment in G42, an AI firm based in the United Arab Emirates, a deal facilitated by the Biden administration in an effort to counter Chinese diplomacy in the Middle East. (NYT)

United Airlines incurred a $200 million in losses due to the scandal surrounding the Boeing 73, slashed its expectations for aircraft deliveries from Boeing over the next few years, and will seek to fill the gap by leasing Airbus planes. (CNBC)

UnitedHealth beat 1Q expectations on top and bottom lines, despite taking a $1.6 billion charge after a massive February 21 ransomware attack at its Change Healthcare subsidiary. (RT)

AMD unveiled new processors specifically designed to power AI capabilities in PCs, and are expected to begin appearing in PC models in 2Q 2024. (CNBC)

The International Monetary Fund expects global economic growth to remain tepid, with world GDP remaining steady at 3.2% in 2024 and 2025, just as it was in 2023. (Axios)

Morgan Stanley saw 1Q earrings rise 14%, with investment-banking fees helping the firm to beat Street expectations. (FT)

First news

- The authors of Stanford University’s annual AI Index suggest large AI models are running out of material to use for training purposes, but not everyone agrees.

- Federal Reserve Chair Jerome Powell sent a strong signal that there would not be a rate cut at the next FOMC meeting on May 1.

- A survey of Chinese electric-vehicle owners shows a worryingly high level of buyer’s remorse.

Chart of the Day

MARKET LEVELS

| Overnight |

| S&P Futures +14

point(s) (+0.3%

) overnight range: -17 to +19 point(s) |

| APAC |

| Nikkei -1.32%

Topix -1.26% China SHCOMP +2.14% Hang Seng +0.02% Korea -0.98% Singapore +0.32% Australia -0.09% India flat Taiwan +1.56% |

| Europe |

| Stoxx 50 +0.63%

Stoxx 600 +0.49% FTSE 100 +0.47% DAX +0.56% CAC 40 +1.07% Italy +1.08% IBEX +1.14% |

| FX |

| Dollar Index (DXY) -0.12%

to 106.13 EUR/USD +0.23% to 1.0643 GBP/USD +0.36% to 1.2471 USD/JPY -0.1% to 154.57 USD/CNY -0.01% to 7.2368 USD/CNH -0.18% to 7.2515 USD/CHF -0.2% to 0.9112 USD/CAD -0.17% to 1.3805 AUD/USD +0.36% to 0.6425 |

| Crypto |

| BTC +0.51%

to 63364.51 ETH +0.3% to 3080.25 XRP +0.28% to 0.4968 Cardano +0.73% to 0.457 Solana +1.69% to 138.58 Avalanche +0.06% to 34.79 Dogecoin +2.08% to 0.1574 Chainlink +1.07% to 13.51 |

| Commodities and Others |

| VIX -2.23%

to 17.99 WTI Crude -0.7% to 84.76 Brent Crude -0.64% to 89.44 Nat Gas -2.54% to 1.69 RBOB Gas -0.81% to 2.799 Heating Oil -0.59% to 2.636 Gold +0.38% to 2392.06 Silver +1.55% to 28.54 Copper +0.36% to 4.319 |

| US Treasuries |

| 1M -7.0bps

to 5.3168% 3M -1.1bps to 5.3493% 6M -0.5bps to 5.3584% 12M -0.5bps to 5.1661% 2Y -4.0bps to 4.9471% 5Y -4.1bps to 4.6601% 7Y -3.5bps to 4.6561% 10Y -3.1bps to 4.6366% 20Y -1.7bps to 4.8696% 30Y -1.4bps to 4.749% |

| UST Term Structure |

| 2Y-3

M Spread narrowed 4.7bps to -44.9

bps 10Y-2 Y Spread widened 0.7bps to -31.5 bps 30Y-10 Y Spread widened 1.8bps to 11.0 bps |

| Yesterday's Recap |

| SPX -0.21%

SPX Eq Wt -0.55% NASDAQ 100 +0.04% NASDAQ Comp -0.12% Russell Midcap -0.54% R2k -0.42% R1k Value -0.54% R1k Growth +0.03% R2k Value -0.85% R2k Growth +0.02% FANG+ -0.12% Semis +0.83% Software +0.27% Biotech -0.86% Regional Banks -1.27% SPX GICS1 Sorted: Tech +0.23% Cons Staples +0.07% Healthcare +0.02% Comm Srvcs -0.12% Indu -0.2% SPX -0.21% Cons Disc -0.52% Fin -0.62% Materials -0.74% Energy -0.87% Utes -1.35% REITs -1.53% |

| USD HY OaS |

| All Sectors +2.1bp

to 367bp All Sectors ex-Energy +1.0bp to 351bp Cons Disc +1.9bp to 301bp Indu -2.9bp to 256bp Tech -1.3bp to 459bp Comm Srvcs +6.6bp to 637bp Materials +1.0bp to 316bp Energy +0.3bp to 281bp Fin Snr +6.0bp to 331bp Fin Sub -0.3bp to 240bp Cons Staples +0.9bp to 320bp Healthcare +0.3bp to 419bp Utes -2.2bp to 226bp * |

| Date | Time | Description | Estimate | Last |

|---|---|---|---|---|

| 4/17 | 4PM | Feb Net TIC Flows | n/a | -8.756 |

| 4/18 | 10AM | Mar Existing Home Sales | 4.2 | 4.38 |

| 4/18 | 10AM | Mar Existing Home Sales m/m | -4.11 | 9.5 |

| 4/23 | 9:45AM | Apr P S&P Manu PMI | n/a | 51.9 |

| 4/23 | 9:45AM | Apr P S&P Srvcs PMI | n/a | 51.7 |

| 4/23 | 10AM | Mar New Home Sales | 672.5 | 662.0 |

| 4/23 | 10AM | Mar New Home Sales m/m | 1.6 | -0.3 |

MORNING INSIGHT

Good morning!

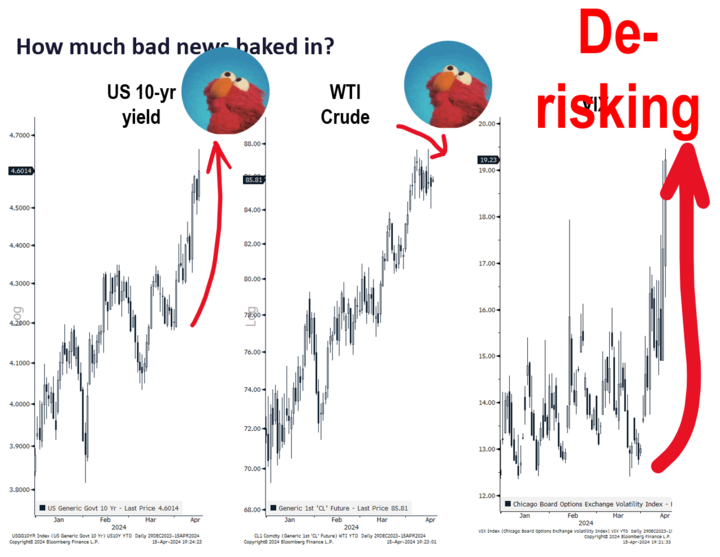

We are in a wartime situation, and markets appear to still be trying to get comfortable in position squaring.

Crisis generally means both danger and opportunity, but right now, elevated VIX tells us there’s still more derisking ahead. In our view, it would be good to move slowly right now.

Click HERE for more.

TECHNICAL

Only two out of 11 sectors finished positive on Tuesday – Technology and Consumer Staples. Notably, many of the defensives, such as REITS and Utilities, had outsized losses, which is to be expected when rates are surging higher.

Until we can see some evidence of rates rolling over a little bit and the Treasury market stabilizing, equities are arguably going to have a difficult time moving higher.

Apple had attempted to break out of a multi-month downtrend, but is now giving way on lower volume. This could possibly be good risk-reward, but ideally we would want to see a move back to around 178 or above to have conviction that Apple has bottomed.

Click HERE for more.

CRYPTO

Risk assets remain under pressure weak in the face of rising rates, geopolitical risks, and tax season. However, despite recent price fluctuations, excitement is mounting in the Bitcoin ecosystem. In addition to the upcoming halving and the launch of Runes, Bitcoin’s layer-2 network, Stacks, is set to begin its Nakamoto upgrade next week, aiming to be completed by the end of May.

Drift, a Solana-based decentralized exchange protocol, is gearing up to launch its governance token, DRIFT, with a total supply of 1 billion tokens, 10% of which will be distributed through an airdrop to 180,000 users based on platform activity. While specific dates for the token generation event and airdrop claim are forthcoming, the launch is anticipated in the coming weeks.

Click HERE for more.

FIRST NEWS

Stanford University’s 2024 AI Index was published this week, and the authors warned that large AI models could run out of text that can be used to train such models as early as year-end 2024. Citing Epoch, an AI research consultancy, the authors of the AI Index noted that the amount of high-quality human-generated content increases by around 7% each year, but the data requirements for training AI models grows by 200% a year.

However, Epoch AI has clarified its views, now suggesting that the situation is not quite as dire. Epoch reiterated that the quantity of high-quality, human-edited content (e.g., published news articles) available for training was constrained. However, Epoch argues that while less polished sources might not be as effective, they can still be used, thus extending the deadline by decades.

“We think that broader kinds of data might still be useful, perhaps not to the same degree, but they might still be enough to continue the pace of scaling so we have become a bit more optimistic,” Epoch AI’s Jaime Sevilla said. Meanwhile, AI giants such as Microsoft and Anthropic are doing research into ways of generating synthetic data that is both accurate and usefully diverse, in a training sense.

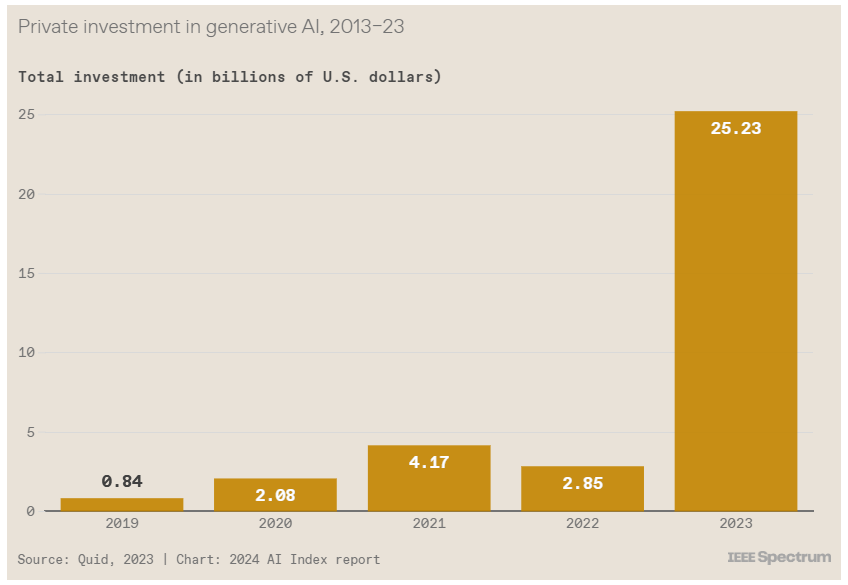

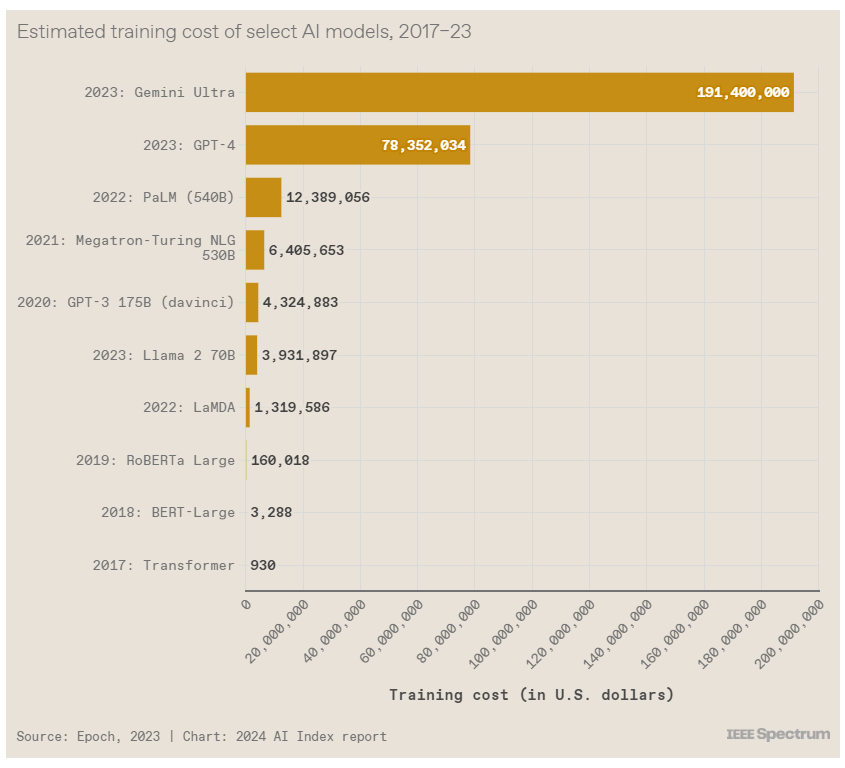

Another takeaway from the AI Index: Generative AI investment skyrocketed in 2023. How much? Quite a lot, as it turns out.

One reason for that is that foundation models have become increasingly and enormously expensive. (Foundation models are AI models that are broadly versatile – OpenAI’s Chat GPT, which can answer questions about monetary policy, plan vacation itineraries, and also compose Shakespearean-style sonnets, is one example.)

(AI Index 2024, Semafor, Spectrum IEEE )

Central banks diverge. Federal Reserve Chair Jerome Powell sent a strong signal that there would not be a rate cut at the next FOMC meeting on May 1. Powell cited a “lack of further progress” on inflation, along with signs of continued strength and resilience in the U.S. economy. Powell made the remarks during a discussion at the Wilson Center, a think tank affiliated with the Smithsonian Institution. Powell’s remarks might not have surprised many, as the CME Fedwatch tool showed investors are almost unanimous in expecting the FOMC to keep rates unchanged on May 1.

If Powell signaled a wait-and-see attitude, his counterpart at the European Central Bank (ECB) expressed comparatively more optimism. Speaking on the sidelines of IMF meetings, ECB head Christine Lagarde said, “We are observing a disinflationary process that is moving according to our expectations,” and “it will be time to moderate the restrictive monetary policy in reasonably short order,” barring any “barring any “major shocks.” (Barron’s, BBG)

Electric regret. A poll of Chinese EV owners by McKinsey showed that roughly one in five want their next car to be a traditional gas or diesel vehicle. The results suggest a surprisingly high degree of buyer’s remorse, particularly worrying for EV makers for several reasons.

One concern is that this dissatisfaction seems to have become significantly more common. In 2022, a similar survey showed that just 3% of Chinese EV owners appeared to regret buying an EV. Perhaps more worrying is that China has already taken steps to tackle a key concern of potential EV owners – the lack of charging infrastructure. In China, there is roughly one charging station for every 2.5 electric vehicles, albeit mostly urban areas and often not offering high-speed charging. Nevertheless, although precise and current figures were not immediately available for the U.S., this ratio is considerably higher than the U.S. statistics from 2022 show: 1 charging station for every 15 vehicles.

China and the U.S. both remain committed to building out charging infrastructure. China has plans to improve its ratio to 1 station for every 2 vehicles by the end of 2025 – a goal that would require more than 20 million new stations. In the U.S., President Biden has invested $5 billion to build out a “national backbone” of high-speed charging stations along major highways and roads. (Semafor)

Articles Read 1/2

🎁 Unlock 1 extra article by joining our Community!

Stay up to date with the latest articles. You’ll even get special recommendations weekly.

Already have an account? Sign In 00816d-83164f-60d5f8-aa54e7-6b0846

Already have an account? Sign In 00816d-83164f-60d5f8-aa54e7-6b0846