Our Views

Not only did we get the Fed capitulating, but also a market in which many had to rethink their massively hawkish views. But given the huge drop in the Fed’s expectations for inflation this year and next year, we can see a likely reason for the market’s reaction. We saw some panic buying once the once-rigidly bearish realized that “higher for longer” no longer makes sense.

The SEP suggests the possibility of three rate cuts next year, but it’s important to note that when Chair Powell was asked about real rates during the press conference, he said that “I think the expectation would be that the real rate is declining as we move forward.”

Remember that the real rate is Fed funds minus inflation. So if inflation gets softer without the Fed cutting rates, then the real rate goes up. The Fed actually has to cut rates as inflation softens just to keep the real rates the same.

So to us, Powell suggesting the possibility of declining real rates (as inflation softens) actually means four or more cuts.

As I have said in the past, Chair Powell strives to achieve unanimous votes by the Committee on rate decisions. Despite yesterday’s dovish shift, I suspect that when the minutes from the December meeting are released in several weeks, we will discover some cautionary language in them, but this language will likely be included so that Powell can keep the hawks on board during future meetings.

Capitulation: Dovish Shift for Fed at December FOMC Meeting

The Federal Reserve once again kept rates unchanged at the December 13 FOMC meeting, leaving them at levels set on July 26, 2023 and strengthening our long-held conviction that the Fed might be done with hikes for this cycle. Washington Policy Strategist Tom Block had previously emphasized that “Chair Powell strives to achieve a unanimous vote by the Committee when it reaches rate decisions,” and this month, Powell succeeded again. As it has in previous meetings, the Fed acknowledged the continued easing of inflation while reiterating its commitment to an inflation target of 2%.

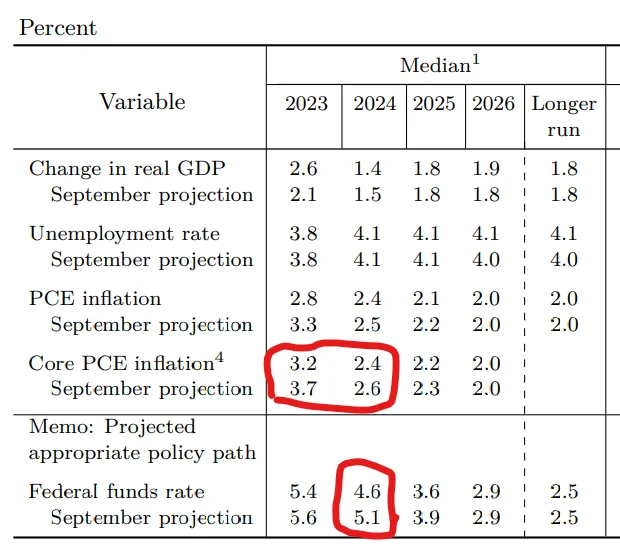

Unlike previous months, the Fed’s projections signaled expectations for as many as three cuts in 2024 (assuming the Fed follows its pattern of changing rates in increments of 0.25%). Given the disparity in the Committee’s previous inflation projections, and how inflation data for the past several months has actually turned out, this was not a surprise for us. In fact, Lee went so far as to suggest that the Fed needed to make a dovish move on Wednesday, arguing that Committee members had been ignoring data that showed inflation falling.

The Fed's September SEP (summary economic projections) showed median expectations for Core PCE YoY of +3.7%. Yet, as Lee pointed out, “Oct Core PCE YoY came in at 3.5%, and Core PCE MoM has come in below +0.20% in 4 of the last 5 months (September was an aberration).” He said, “In my view, at this pace, Core PCE YoY is likely to reach 3.1-3.3% by the end of 2023.”

The September SEP, in which some members raised their dot plots, caused many investors to react bearishly: US 10-yr yields soared above 5% and stocks fell 10% as a result. Because of that prior responsiveness, Lee suggested that on December 13, many investors and markets would react positively if the Fed were to lower its SEP dot plots for 2023 and 2024. That’s precisely what happened once markets realized that, as Lee put it, “The Fed [is] capitulating on inflation and ‘higher for longer.’”

US 10-year rates plummeted more than 10 bp to around 4.08 immediately after the statement was released. Equities surged, with the Russell 2000 shooting up more than 3% after the announcement. Lee suggested that this also shows how most equities investors had been short going into the meeting, expecting Powell to go hawkish. Instead, Powell spoke about “the risk that we would hang on too long,” emphasizing that “we’re very focused on not making that mistake.”

FOMC membership changes

It is worth noting that the roster of FOMC voting members will change in January as part of its regular annual rotation.

Leaving the Committee will be:

- Austan D. Goolsbee (President, Federal Reserve Bank of Chicago)

- Patrick T. Harker (President, Federal Reserve Bank of Philadelphia)

- Neel Kashkari (President, Federal Reserve Bank of Minneapolis)

- Lorie K. Logan (President and CEO, Federal Reserve Bank of Dallas)

They will be replaced by:

- Thomas I. Barkin (President and CEO, Federal Reserve Bank of Richmond)

- Raphael W. Bostic (President, Federal Reserve Bank of Atlanta)

- Mary C. Daly (President, Federal Reserve Bank of San Francisco)

- Loretta J. Mester (President, Federal Reserve Bank of Cleveland)

Articles Read 1/2

🎁 Unlock 1 extra article by joining our Community!

Stay up to date with the latest articles. You’ll even get special recommendations weekly.

Already have an account? Sign In b6c42a-7e4c1a-cfdbe7-c4e79e-fd5afa

Already have an account? Sign In b6c42a-7e4c1a-cfdbe7-c4e79e-fd5afa