-

Research

-

Latest Research

-

Latest VideosFSI Pro FSI Macro FSI Crypto

- Tom Lee, CFA AC

-

First WordFSI Pro FSI Macro

-

Intraday WordFSI Pro FSI Macro

-

Macro Minute VideoFSI Pro FSI Macro

-

OutlooksFSI Pro FSI Macro

- Mark L. Newton, CMT AC

-

Daily Technical StrategyFSI Pro FSI Macro

-

Live Technical Stock AnalysisFSI Pro FSI Macro

-

OutlooksFSI Pro FSI Macro

- L . Thomas Block

-

US PolicyFSI Pro FSI Macro

- Market Intelligence

-

Your Weekly RoadmapFSI Pro FSI Macro FSI Weekly

-

First to MarketFSI Pro FSI Macro

-

Signal From Noise

-

Earnings DailyFSI Pro FSI Macro FSI Weekly

-

Fed WatchFSI Pro FSI Macro

- Crypto Research

-

StrategyFSI Pro FSI Crypto

-

CommentsFSI Pro FSI Crypto

-

Funding FridaysFSI Pro FSI Crypto

-

Liquid VenturesFSI Pro FSI Crypto

-

Deep ResearchFSI Pro FSI Crypto

-

-

Webinars & More

- Webinars

-

Latest WebinarsFSI Pro FSI Macro FSI Crypto

-

Market OutlookFSI Pro FSI Macro FSI Crypto

-

Granny ShotsFSI Pro FSI Macro FSI Crypto

-

Technical StrategyFSI Pro FSI Macro FSI Crypto

-

CryptoFSI Pro FSI Macro FSI Crypto

-

Special GuestFSI Pro FSI Macro FSI Crypto

- Media Appearances

-

Latest Appearances

-

Tom Lee, CFA AC

-

Mark L. Newton, CMT AC

-

Sean Farrell AC

-

L . Thomas Block

-

⚡FlashInsights

-

Stock Lists

-

Latest Stock Lists

- Super and Sleeper Grannies

-

Stock ListFSI Pro FSI Macro

-

CommentaryFSI Pro FSI Macro

-

HistoricalFSI Pro FSI Macro

- SMID Granny Shots

-

Stock ListFSI Pro FSI Macro

-

PerformanceFSI Pro FSI Macro

-

CommentaryFSI Pro FSI Macro

-

HistoricalFSI Pro FSI Macro

- Upticks

-

IntroFSI Pro FSI Macro

-

Stock ListFSI Pro FSI Macro

-

PerformanceFSI Pro FSI Macro

-

CommentaryFSI Pro FSI Macro

-

FAQFSI Pro FSI Macro

- Sector Allocation

-

IntroFSI Pro FSI Macro

-

Current OutlookFSI Pro FSI Macro

-

Prior OutlooksFSI Pro FSI Macro

-

PerformanceFSI Pro FSI Macro

-

SectorFSI Pro FSI Macro

-

ToolsFSI Pro FSI Macro

-

FAQFSI Pro FSI Macro

-

-

Crypto Picks

-

Latest Crypto Picks

- Crypto Core Strategy

-

IntroFSI Pro FSI Crypto

-

StrategyFSI Pro FSI Crypto

-

PerformanceFSI Pro FSI Crypto

-

ReportsFSI Pro FSI Crypto

-

Historical ChangesFSI Pro FSI Crypto

-

ToolsFSI Pro FSI Crypto

- Crypto Liquid Ventures

-

IntroFSI Pro FSI Crypto

-

StrategyFSI Pro FSI Crypto

-

PerformanceFSI Pro FSI Crypto

-

ReportsFSI Pro FSI Crypto

-

-

Tools

-

FSI Community

-

FSI Snapshot

-

Market Insights

-

FSI Academy

-

Book Recommedations

- Community Activities

-

Intro

-

Community Questions

-

Community Contests

-

Part 3

Risk Mitigation Enables Greater Risk-Adjusted Return

Risk management has become a ubiquitous sub-field in the financial world, but it wasn’t always the case. If there are dark clouds outside and you never go outside because you’re afraid of getting wet, then you’ve likely already failed in your investment strategy.

If you look far enough, there will always be ominous clouds on the horizon, so you have to bring an umbrella with you if you wish to operate effectively and stay dry in the world. The umbrella is a metaphor for the utility of a hedge. If you’re wearing an expensive suit, then an umbrella is definitely worth the investment, isn’t it? This everyday logic is at the root of risk management and mitigating your risk despite the field’s prohibitive jargon.

If you have better peace of mind and you’re less worried about career-ending catastrophic losses, then you’ll probably be a better investor. There will be many people trying to sell you different hedges, and you need to be able to determine whether or not that hedge is effective? How do we do this?

Well, one key thing to pay attention is the correlation of the asset you are trying to hedge with the instrument you’re trying to hedge with. There can be direct instruments, like inverse ETFs, that will try to have a precise -1 correlation with the asset you’re trying to hedge. There are also leveraged ETFs with a -2 or -3 correlation to the investment you’re trying to hedge. While this may be what the vendor is selling, always be sure to check the correlations and historical data yourself, mainly if you’re using cross-asset hedging.

An example of cross-asset hedging would be the way many “Gold Bugs” have used their favored asset over the years. Those who lack faith in government, particularly those who lived through the Depression, always had a great affinity for gold because they saw it as separate from the machinations of what some would describe as the unstoppable fiscal expansion of the US government. In other words, Gold is not directly correlated to US currency.

Still, as a commodity that is bought to hedge against inflation, the correlation itself to events that weaken the dollar almost becomes a self-fulfilling prophecy. Using gold to hedge against a constellation of tail risks is an example of cross-asset hedging. Using an inverse SPY ETF to hedge a position on the

long side of the index would be an example of direct hedging. In other words, the ETF is specifically designed to be a precise instrument specifically designed to mitigate risk in a particular asset.

We’re much bigger fans of crypto these days. While the crypto doesn’t have definitive correlations, the fact that it is uncorrelated to significant risk assets is in itself a helpful characteristic for an investment. Why? Because when there is market panic and sell-offs, the old saying is, all correlations go to 1. So, sometimes in market panics, assets that typically move in opposite directions may actually sync up. This is often why downside panics exaggerate economic losses and often bring assets below their inherent values.

Some folks may think hedging is too expensive, and sometimes it is. Don’t hedge just to hedge. Just as you seek out investments that appear cheaply priced, the same is true of your hedges. Too great an emphasis on perfect hedging and ensuring every situation is fully covered may begin to diminish the returns of the assets you’re hedging. How do you determine which contracts are better priced than others? Well, the Black-Scholes Model, of course. This will be the subject of our next educational guide, and we recommend reading it next month to build on the lessons from the guide.

Related Guides

-

Series of 3~15 minutesLast updated1 year ago

Series of 3~15 minutesLast updated1 year agoInflation – What’s All the Fuss About?

A multi-part series about inflation and its impact on stock investors.

-

Series of 3~11 minutesLast updated3 years ago

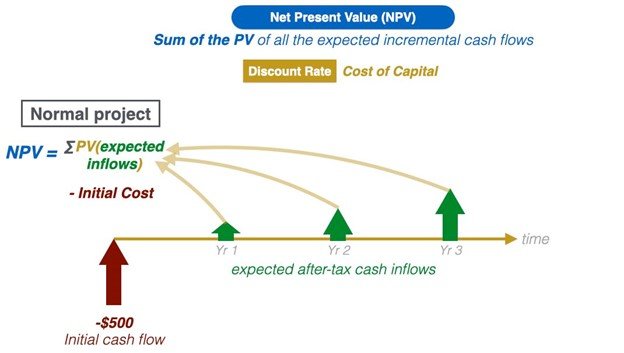

Series of 3~11 minutesLast updated3 years agoUnderstanding Net Present Value and The Basics of Discounted Cash Flow Models (DCF)

Acquaint yourself with the basics of net present value and discounted cash flow (DCF) models.

-

Series of 8~27 minutesLast updated2 years ago

Series of 8~27 minutesLast updated2 years agoBitcoin Guide

Is it a good time to get in? How much should I invest?

-

Series of 5~21 minutesLast updated3 years ago

Series of 5~21 minutesLast updated3 years agoThe VIX Series

What is the VIX? What does it indicate? How can I use it to improve my strategies?