-

Research

-

Latest Research

-

Latest VideosFSI Pro FSI Macro FSI Crypto

- Tom Lee, CFA AC

-

First WordFSI Pro FSI Macro

-

Intraday WordFSI Pro FSI Macro

-

Macro Minute VideoFSI Pro FSI Macro

-

OutlooksFSI Pro FSI Macro

- Mark L. Newton, CMT AC

-

Daily Technical StrategyFSI Pro FSI Macro

-

Live Technical Stock AnalysisFSI Pro FSI Macro

-

OutlooksFSI Pro FSI Macro

- L . Thomas Block

-

US PolicyFSI Pro FSI Macro

- Market Intelligence

-

Your Weekly RoadmapFSI Pro FSI Macro FSI Weekly

-

First to MarketFSI Pro FSI Macro

-

Signal From Noise

-

Earnings DailyFSI Pro FSI Macro FSI Weekly

-

Fed WatchFSI Pro FSI Macro

- Crypto Research

-

StrategyFSI Pro FSI Crypto

-

CommentsFSI Pro FSI Crypto

-

Funding FridaysFSI Pro FSI Crypto

-

Liquid VenturesFSI Pro FSI Crypto

-

Deep ResearchFSI Pro FSI Crypto

-

-

Webinars & More

- Webinars

-

Latest WebinarsFSI Pro FSI Macro FSI Crypto

-

Market OutlookFSI Pro FSI Macro FSI Crypto

-

Granny ShotsFSI Pro FSI Macro FSI Crypto

-

Technical StrategyFSI Pro FSI Macro FSI Crypto

-

CryptoFSI Pro FSI Macro FSI Crypto

-

Special GuestFSI Pro FSI Macro FSI Crypto

- Media Appearances

-

Latest Appearances

-

Tom Lee, CFA AC

-

Mark L. Newton, CMT AC

-

Sean Farrell AC

-

L . Thomas Block

-

⚡FlashInsights

-

Stock Lists

-

Latest Stock Lists

- Super and Sleeper Grannies

-

Stock ListFSI Pro FSI Macro

-

CommentaryFSI Pro FSI Macro

-

HistoricalFSI Pro FSI Macro

- SMID Granny Shots

-

Stock ListFSI Pro FSI Macro

-

PerformanceFSI Pro FSI Macro

-

CommentaryFSI Pro FSI Macro

-

HistoricalFSI Pro FSI Macro

- Upticks

-

IntroFSI Pro FSI Macro

-

Stock ListFSI Pro FSI Macro

-

PerformanceFSI Pro FSI Macro

-

CommentaryFSI Pro FSI Macro

-

FAQFSI Pro FSI Macro

- Sector Allocation

-

IntroFSI Pro FSI Macro

-

Current OutlookFSI Pro FSI Macro

-

Prior OutlooksFSI Pro FSI Macro

-

PerformanceFSI Pro FSI Macro

-

SectorFSI Pro FSI Macro

-

ToolsFSI Pro FSI Macro

-

FAQFSI Pro FSI Macro

-

-

Crypto Picks

-

Latest Crypto Picks

- Crypto Core Strategy

-

IntroFSI Pro FSI Crypto

-

StrategyFSI Pro FSI Crypto

-

PerformanceFSI Pro FSI Crypto

-

ReportsFSI Pro FSI Crypto

-

Historical ChangesFSI Pro FSI Crypto

-

ToolsFSI Pro FSI Crypto

- Crypto Liquid Ventures

-

IntroFSI Pro FSI Crypto

-

StrategyFSI Pro FSI Crypto

-

PerformanceFSI Pro FSI Crypto

-

ReportsFSI Pro FSI Crypto

-

-

Tools

-

FSI Community

-

FSI Snapshot

-

Market Insights

-

FSI Academy

-

Book Recommedations

- Community Activities

-

Intro

-

Community Questions

-

Community Contests

-

Part 2

Understanding Human Behavior and Biases

One of the most interesting components of investor psychology lies in its counterintuitive nature. Investing after a significant drawdown has the potential to pay off handsomely. There’s a consistent pattern of quality returns if you invest in the strategy of a decline of 15% of more. Investors in the strategy roughly double the market’s long-term average returns. “It’s waiting that helps you as an investor, and a lot of people just can’t stand to wait,” Charlie Munger has said.

Author, philosopher, and investor Naval Ravikant has said, “Don’t take yourself so seriously. You’re just a monkey with a plan.” What he means is that we humans are not as rational as we think. We say we’re going to buy low and sell high, but that simple concept is much harder to put to practice when there’s panic on the street. An investment advisor won’t necessarily get flooded with calls from his or her client when they’ve reported a sizeable gain. But big losses? The phone will be running off the hook. A loss appears larger than a gain of equal size. The value of money changes in our mind.

To dig deeper, let’s identify five key human behaviors and biases that impact our investments:

Anchoring, which is placing too much importance on recent events while ignoring historical data, is an over- or under-reaction to market events. In the short run, stock prices often over-swing in both directions. In the long run, they revert to the mean. Prices fall too much on bad news and rise too much on good news. Eventually, things stabilize. Investors also make mistakes because they presume that a stock performing well in the past will continue to do so.

Action bias describes our tendency to favor action over inaction. Sometimes, we feel compelled to act, even if there’s no evidence that our action will lead to a better outcome than doing nothing would. Humans tend to act as default. For example, when markets move lower, the human tendency to act – often to sell – settles in.

Choice overload, known as overchoice, choice paralysis, or the paradox of choice, describes how investors get overwhelmed when presented with many options. When a friend recommends that we buy many stocks, it can be difficult to decipher through the noise and make a sound investment decision.

The bandwagon effect, similar to herd mentality, relates to our habit of adopting certain behaviors or beliefs because many other people do the same. Wall Street Bets popularized this concept in early 2021, pushing up the share price of meme stocks such as GameStop and AMC.

Cognitive dissonance describes what happens when we avoid having conflicting beliefs and attitudes because it makes us uncomfortable. Humans often reject, debunk, or even avoid new information. In investing, we can become attached to a belief or approach, which can create blind spots. Having your views confirmed is a powerful drug.

Warren Buffett’s style has succeeded for decades, in part, because he simply buys and holds. His investment time horizon is “forever,” meaning he doesn’t usually plan to sell stocks. There’s minimal trading. He’s never worried about others mimicking his investment style because no other institution or individual has the discipline or patience to wait as long as he can. But there’s no one-size-fits-all investment approach. Some hedge funds and money managers with shorter time horizons outperform the market regularly.

Average investors, meanwhile, consistently fail to achieve returns that beat or even match the broader market indices. Studies have found that in the 17-year period to December 2000, the S&P 500 returned an average of 16.29% per year, while the typical equity investor achieved only 5.32% for the same period—a startling difference. Human behavior is a lead reason why.

The fear of regret concerns the emotional reaction we experience after realizing we’ve made an error in judgment. Faced with the prospect of selling a stock, investors become emotionally affected by the price at which they purchased the stock. This might lead them to avoid selling it to avoid a bad investment.

When 2022 began, many people seemed to believe we lived in especially exhaustive, volatile times. But the rhythms of our moment – pandemic, protest, pandemic, election, insurrection, pandemic, inflation, invasion of Ukraine, market volatility – were nothing new. As Lee, our head of research, often notes: There’s nothing new under the sun. This underscores the importance of looking at cycles and recognizing that what has happened could happen again. The adage applies to markets in profound ways, helping us navigate turbulence and uncertainty. “There’s no excuse for being surprised.”

In the book Of Anger, Seneca draws on Fabius, one of Ancient Rome’s great generals, to teach a lesson from war: “Fabius used to say that the basest excuse for a commanding officer is ‘I didn’t think it would happen,’ but I say it’s the basest for anyone. Thinking everything might happen; anticipate everything.” Anticipate everything is worth keeping at the forefront of your investing approach. In markets, then, we shouldn’t be surprised by the twists and turns, the inevitable ebb and flow. But there is no benefit in panic, even though we endured one of the S&P 500’s worst starts to a year in its history. Sometimes, the stock market is wobbly. Sometimes, prices decline sharply.

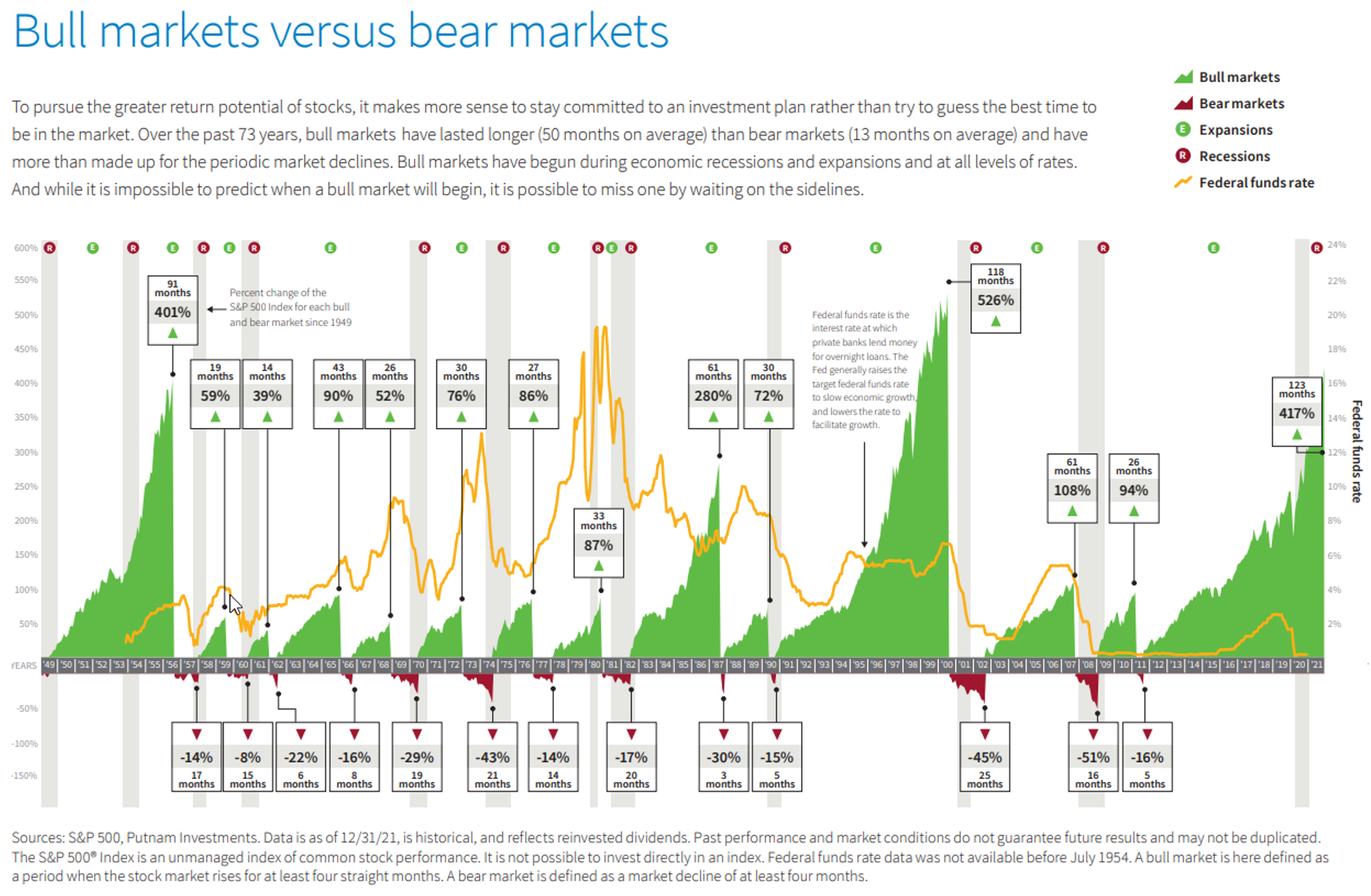

Remember, the market goes down roughly:

- 10% once per year or so

- 20% every 5 years

- 30% every decade

Gut-wrenching stock swings are not for the faint of heart. Just bear in mind, this is a marathon, not a sprint. A reminder: the average year (since 1980) sees a 14% pullback and the average midterm year (since 1950) sees a pullback 17% before climbing higher. “I am still a long-term bull,” Mark Newton, our head of technical strategy, said this year. “It’s all a matter of risk tolerance and time horizon.”

Markets go up a lot, usually slowly but surely, via the staircase. They also go down from time to time, usually via the elevator, in swift, sharp declines without much warning. Since 1928, the S&P 500 has averaged one bear market every four years. We can’t predict the future, but there have been many major market resets over time. Investors with a long view have been rewarded well every time.

Related Guides

-

Series of 3~5 minutesLast updated1 month ago

Series of 3~5 minutesLast updated1 month agoKeep Calm and Carry on Investing

A guide to managing your emotions during market downturns.

-

Series of 2~4 minutesLast updated2 months ago

FS Insight Decoded

An ad-hoc series that explains sayings frequently used by members of the FS Insight research team

-

Series of 3~6 minutesLast updated5 months ago

Your Price Target Is Likely Going to be Wrong. Here’s Why You Should Set One Anyway.

Price Targets

-

Series of 3~9 minutesLast updated11 months ago

Series of 3~9 minutesLast updated11 months agoTechnically Speaking – The FS Insight Primer on Technical Analysis

Three-part series on technical analysis

-

Series of 4~10 minutesLast updated2 years ago

Commodities 100

An introduction to commodities for novice investors.