US Equity Markets have stalled out given US Treasury yields having turned back up sharply; Given recent correlation trends, this might persist this week before Stock indices rally back. Energy remains one of the more attractive sectors given recent Crude strength

Minor pullback looks to be underway following the push back higher in yields to kick off this holiday shortened week. While the larger trend in Treasury yields should be close to rolling over, this short-term bounce looks to extend in the days ahead. This might result in short-term selling pressure for US Stocks.

Tuesday’s session proved to be worse “Under the hood” than what indices showed by the End of Day close, as Technology’s strength largely helped US indices from showing much weaker performance. Six sectors finished with performance of -1.0% or worse, with Consumer Staples just barely missing the cut.

Key support lies at SPX-4458, near a 38.2% Fibonacci retracement of the rally from mid-August. Additional support lies at 4439, while a break of 4415 could allow for a more meaningful period of weakness and retest of August lows.

At present, I am not expecting a severe decline in September, and expect that any further dips find support into mid-Month before rallying back. However, Tuesday’s drop to multi-day lows on a closing basis likely does extend a bit lower this week ahead of finding support and turning higher.

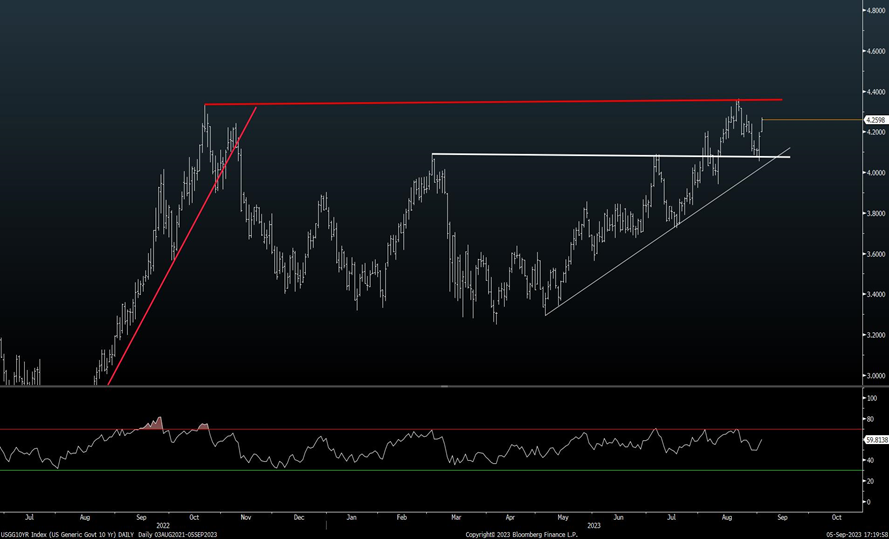

Treasury Yields turning back higher to challenge August peaks

Yields have begun to turn back higher this week, and a retest of August’s peaks in 10 and 30-year yields cannot be ruled out over the next 1-2 weeks.

Overall, given that yields and stocks have moved in opposite directions lately, a sharp rally back in yields could serve to spook stock indices temporarily and allow for a minor pullback in US Equities.

As I’ve discussed in recent reports, sentiment, cycles, DeMark indictors and seasonality all argue for yields to begin pulling back into 2024. Yet, yields require a bit more evidence of technical damage before being able to weigh in that a larger decline is underway.

As daily ^TNX charts show, a break under 4.05% looks to be the more important short-term area of technical support that would have significance.

Energy’s follow-through starts to gain momentum given Saudi Arabia, Russia Output cut extensions

OIH 0.39% (Vaneck Oil Services ETF) looks to be a short-term attractive way to participate in the recent gains in Energy, and in the short run, looks a bit more attractive technically speaking, than either XOP 2.01% (SPDR S&P Oil and Gas Exploration and Production ETF), or XLE 1.37% (Energy Select SPDR ETF)

While XOP has outperformed XLE since April, this looks to have found short-term resistance over the last week and has stalled out relatively speaking. However, Exploration and Production stocks should represent an appealing vehicle for Energy given its correlation to the price of WTI and Brent Crude.

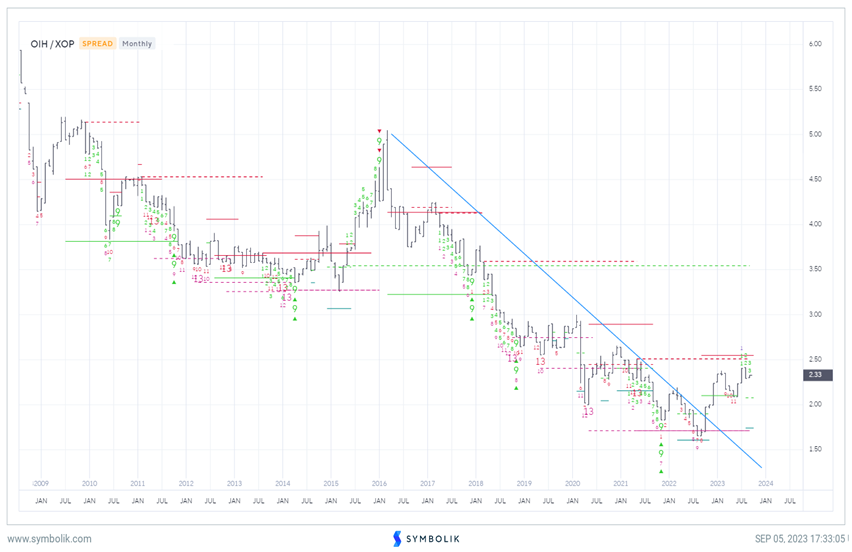

Monthly relative charts of OIH 0.39% vs XOP 2.01% show this ratio to have broken out in the latter part of 2023 after having trended down since 2016.

Thus, the ratio of OIH vs XOP, after having trended down for six years, broke out of a lengthy downtrend last year and continues to trend higher.

While both OIH and XOP look more appealing than XLE (which has larger weightings in XOM 0.60% and CVX 1.19% ) in the short run, many parts of Energy now look to be playing “catchup” following WTI Crude’s breakout to the highest levels of the year.

Energy remains a technical overweight for 2H 2023, and OIH looks likely to be a preferred way of playing energy.

Further short-term consolidation looks likely for Homebuilders as rates climb

The sharp decline to multi-day lows in Homebuilders likely results in a bit more selling pressure in the days/weeks ahead before this group can carve out a technical low.

Homebuilders have proven to be one of the strongest areas within the Consumer Discretionary space this year, and stocks like PHM 0.13% , NVR 0.36% , DHI -0.08% , and LEN -0.59% have all climbed more than 25% Year-to-Date (YTD) representing strong gains within the Discretionary sector.

As weekly charts show the XHB 0.45% (SPDR Homebuilders ETF) maintains an excellent intermediate-term trend from last October’s lows.

Yet, momentum became a bit overbought on the parabolic rise into late July. The subsequent churning followed by August’s selling pressure hasn’t proved too damaging to the longer-term trend.

However, this group does look vulnerable in the near-term as rates push higher. Tuesday’s setback was accompanied by above-average volume on the downside, and likely could lead to a retest and minor break of August’s lows.

My technical target for XHB lies at $75-$76 which would represent an attractive zone of support on further weakness. Bottom line, I suspect that this weakness proves short-lived only and does not do much intermediate-term technical damage. However, in the short run, a bit more weakness looks likely.