The S&P 500 slipped 1.39% this week, and the Nasdaq Composite fell still further, ending the week down 2.10%. Software stocks helped lead the indexes lower, as worries over whether AI would render many forms of software redundant maintained their presence on investors’ wall of worry.

As Fundstrat Head of Research Tom Lee put it, the story of “software eating the world,” which we read repeatedly from 1980-2025, is now becoming one of “AI eating software.” Yet this shift, to Lee, signals that AI is productive and has a payoff. “To us, [the carnage in software] argues that AI’s biggest impact in the U.S. is ultimately less inflation. Because if there are fewer workers, less software and services spend, but the same output, this is both productivity-enhancing and disinflationary.”

From a technical analysis perspective, Head of Technical Strategy Mark Newton acknowledged that “software has struggled to stabilize and find a bottom, [and] they look like they’re going straight down in the short run.” Going forward, Newton told us that “I don’t sense it’s going to be an area to overweight within technology.”

As he told us during our weekly huddle, however, the situation does not necessarily look so dire for those with more of an intermediate-term timeframe. “The intermediate-term charts help to put this deterioration into perspective,” he suggested, and “I do sense that this group can bounce.”

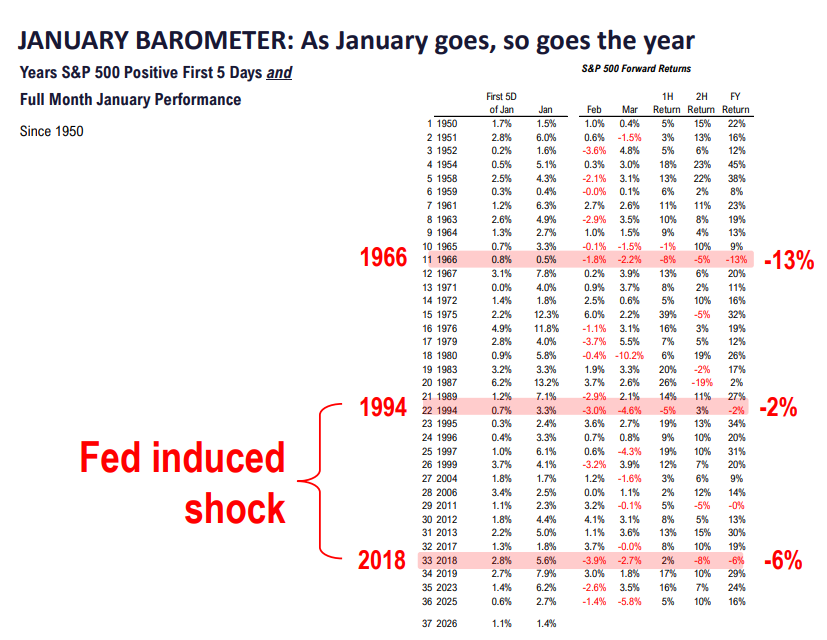

Regardless of one’s views on Kevin Warsh, President Trump’s choice to succeed Jerome Powell as chair of the Federal Reserve, Newton noted this that the changeover to a new Fed chair has historically tended to be followed by market uncertainty and short-term drawdowns. Newton also sees a seasonality challenge. “The second year of a second term of a president has tended to coincide with challenging years for stock investors,” he pointed out, a pattern that has largely held true going as far back as Harry S. Truman’s second term.

For the most part, this independently coincides with Lee’s view. As he reiterated this week, Lee said, “We still think markets have enough tailwinds to get to 7,300, and then we do think there’s likely to be a drawdown that feels like a bear market this year. And then year-end we do finish stronger, in my view.”

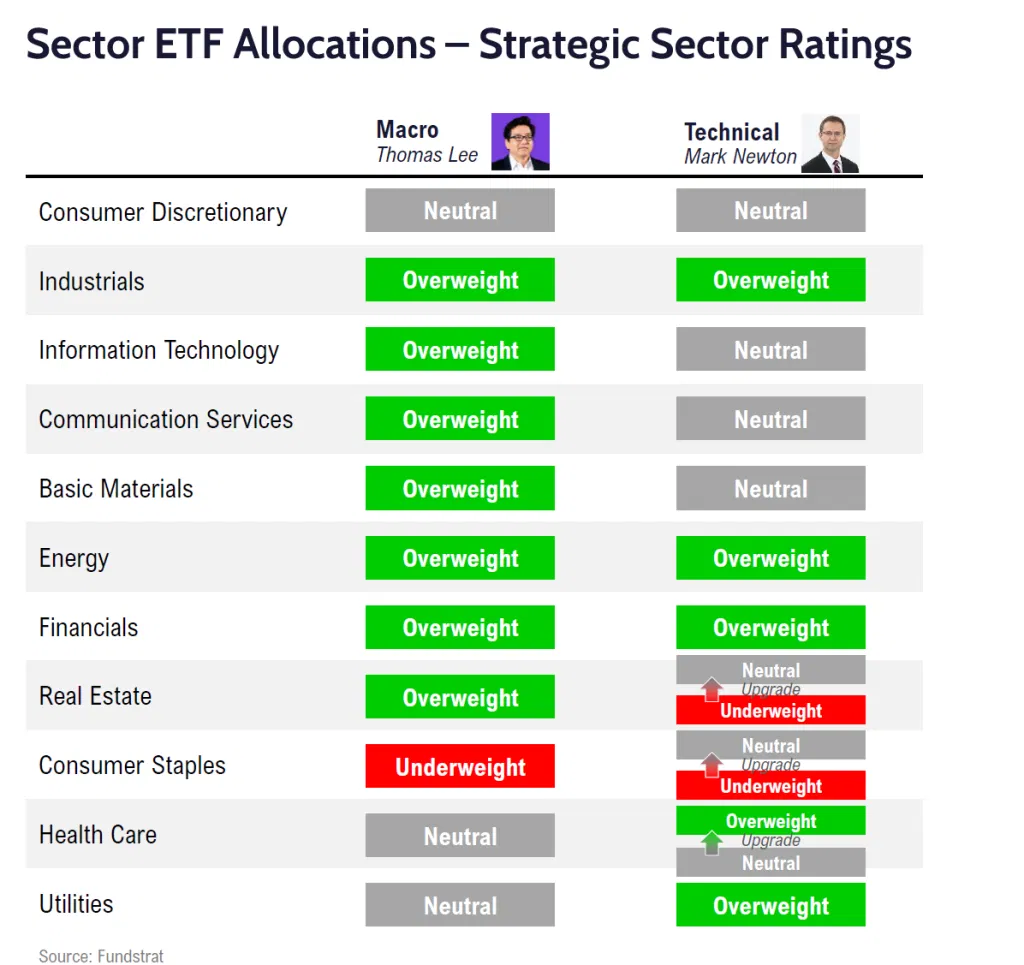

Sector Allocation Strategy

These are the latest strategic sector ratings from Head of Research Tom Lee and Head of Technical Strategy Mark Newton – part of the February 2026 update to the FSI Sector Allocation Strategy. FS Insight Macro and Pro subscribers can click here for ETF recommendations, precise guidance on strategic and tactical weightings, detailed commentary, and methodology.

Chart of the Week

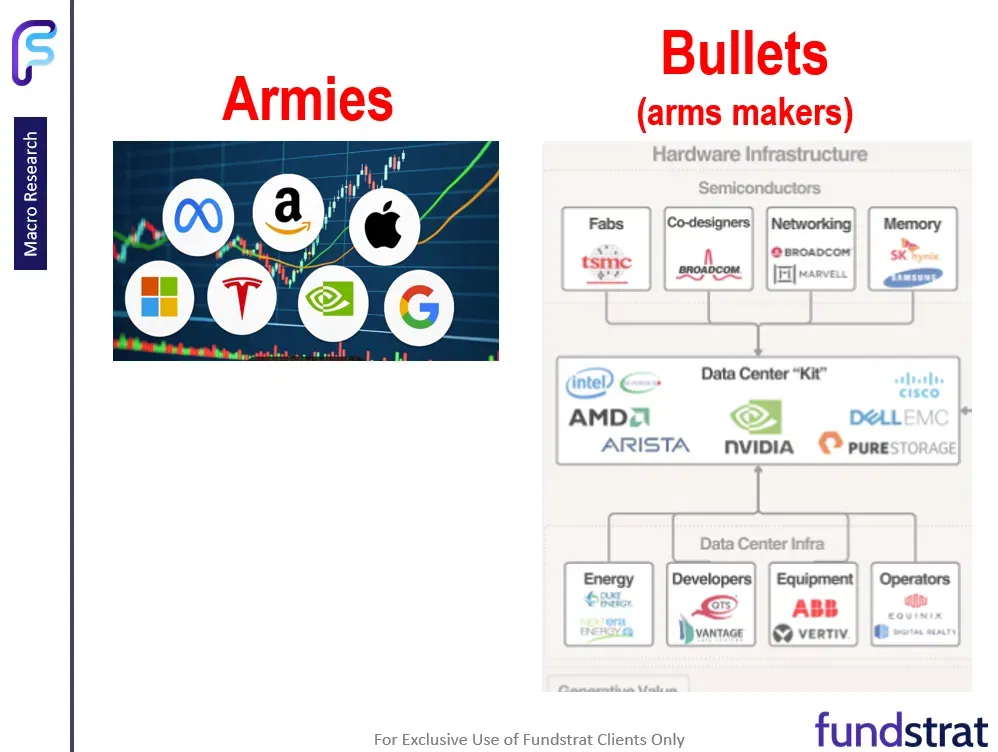

Fundstrat’s Tom Lee views current mood of the market as also related to the current rotation within the AI trade, away from the Magnificent Seven and toward companies in processors, chips, energy, and infrastructure. Taking a look at market history, Lee sees a similarity between the current scenario and the situation with the initial building of nationwide wireless networks in the late 1990s. In those days, investor appetite shifted back and forth between buying carriers and buying infrastructure and handset makers. “Back then, we’d call this ‘buying the armies or buying the bullets,'” he told us. In a modern context and as illustrated in our Chart of the Week, the current AI activity can be seen similarly, shifting between the Magnificent Seven as the “armies” and those companies that make “bullets” – processor and memory-chip makers and those in the business of building out data centers, such as energy companies. To Lee, this current shift does not necessarily mean underweighting or divesting from the “armies” of the Magnificent Seven. “At some point, this rotation will arguably shift again to Mag7,” he told us.

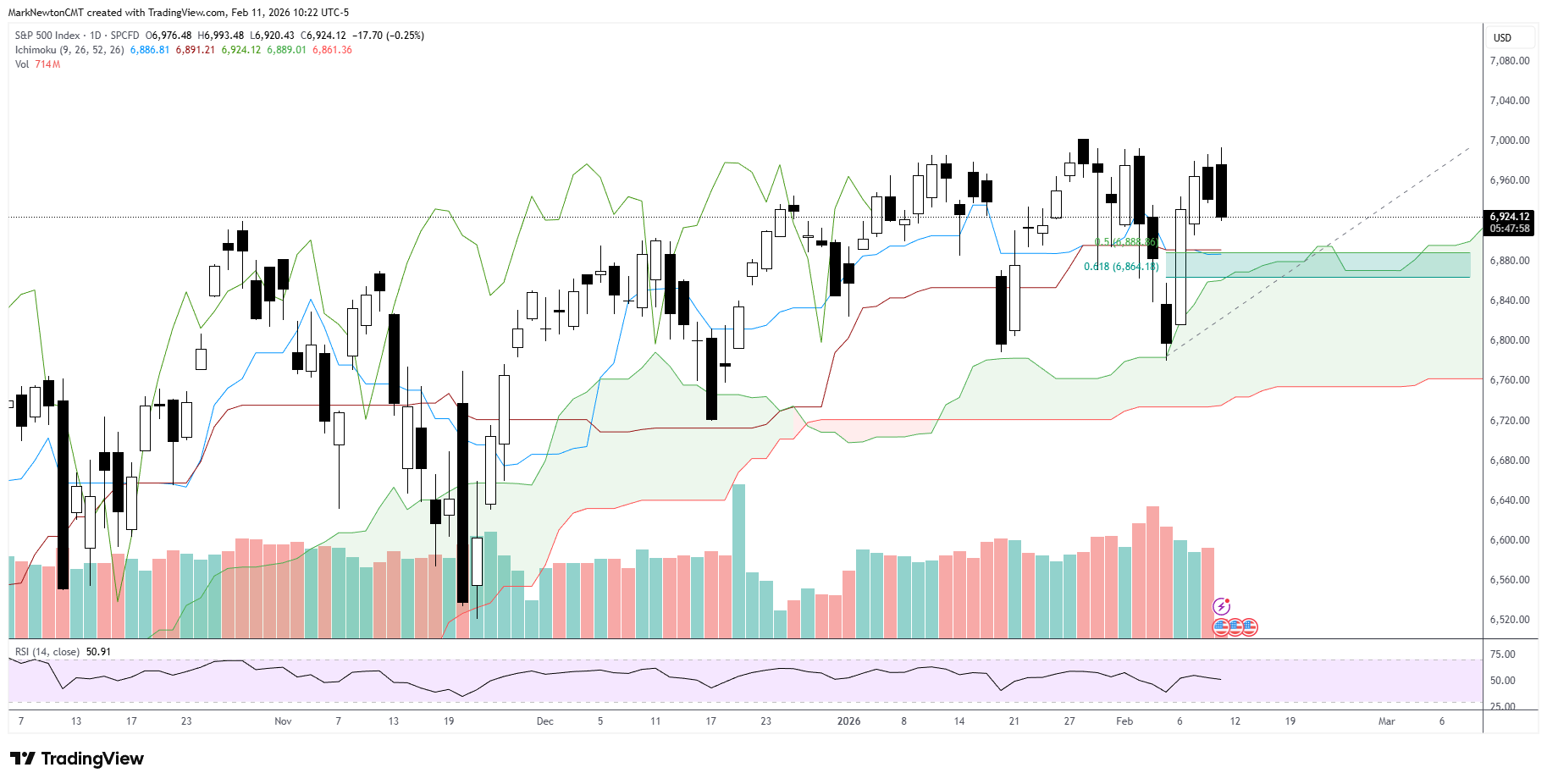

Reposting and updating a chart i shared in last night’s note of IGV 2.33% trying to bottom after its severe decline. As mentioned, following such a steep selloff, bottoming often takes time and is a 2 step forward/1-step backwards type affair. In this case, IGV 2.33% steep 3%+ decline today unless recouped, likely could allow for a pullback to retest lows again, but don’t anticipate that April 2025 lows are taken out at $76.67. Thus, Software stabilization looks to take time, but does appear like we’re getting close to lows, technically. The next 2-3 days might bring about a good risk/reward to attempt to buy into this group on an absolute basis. However, as discussed in notes last week, the breakdown of Software to Technology as a whole is troubling and doesn’t make for an immediate case of favoring this group over other parts of Technology.

Today’s trading is not unlike what’s been happening for most of 2026 thus far. Energy and Materials strengthening while Technology is weak and being weighed down by Software, despite many Semiconductor and memory names still quite positive today (Note: SNDK 0.13% , MU -0.60% , ON 2.35% , WDC -0.78% are all up more than +3.50% today and 4 of the top 10 performers in this morning’s trading are all Tech related, but just not Software based. XLK 0.26% is lower by -0.68% and market breadth is positive despite ^SPX having turned down by 0.34%. This Software move of -3% + likely could lead Tech down a bit further, yet, i don’t expect a larger drawdown than to 6864, or the 61.8% Retracement of the prior rally from last Thursday’s lows. Overall, a choppy market and one which continues to require selectivity. Following some brief consolidation, i expect SPX to push up to 7100-7200 in what could prove to be a peak for February and for 1st Quarter into late February.

GOLD 0.67% meanwhile has pushed back above $5,000/oz as PBOC has extended its gold buying to 15 straight months. Technically given how sharp the recent decline from late January was, this counter-trend rally is not thought to get back to new highs right away technically, but might slow and reverse near 5339. Overall, the next 1-2 weeks could be bullish, but technically i feel this might represent resistance to this bounce and turn lower into Spring.

This research is for the clients of FS Insight only. FSI Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or FS Insight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FS Insight. At the time of publication of this report, FS Insight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FS Insight is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

FS Insight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of FS Insight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by FS Insight clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of FS Insight, which is available to select institutional clients that have engaged FS Insight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

FS Insight does not have the same conflicts that traditional sell-side research organizations have because FS Insight (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by FS Insight and/or affiliates of FS Insight. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of FS Insight.

This research is for the clients of FS Insight only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but FS Insight does not warrant its completeness or accuracy except with respect to any disclosures relative to FS Insight and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where FS Insight expressly agrees otherwise in writing, FS Insight is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fsinsight.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.

{kind=link}