Investors have been nervous and uncertain in the past two weeks. At our weekly research huddle, Fundstrat Head of Data Science Ken Xuan suggested that this was an indirect result of the federal government shutdown, which has largely cut off the flow of macroeconomic data. “As time goes by, the more time we go, the more uncertainty we feel. That’s because we just don’t have data to know where we are,” he said.

It could be argued that Friday morning’s release of September CPI data removed much of that uncertainty, though it must have helped that the numbers came in dovish – lower than consensus expectations. That bolstered expectations of another rate cut when the Federal Open Market Committee meets next Wednesday, and the results could be seen in a range of indices – the S&P 500, the Nasdaq Composite, and the DJIA, as well as the small-cap Russell 2000. All four posted positive weeks, with the Russell 2000 leading the way with a 2.5% weekly gain.

Yet not all of the choppiness from the past two weeks has been due to the lack of fresh data. Fundstrat’s Head of Research Tom Lee attributes much of the rangebound action to a sort of PTSD (post-traumatic stress disorder). U.S.-China trade tensions remained elevated this week as the U.S. threatened to ban exports to China of any products that contain or were made with U.S. software. As Lee suggested, this gave investors “PTSD from earlier this year” when the trade war began.

Head of Technical Strategy Mark Newton remains constructive. Asked to comment on the press speculation that we are currently in a market or AI bubble, he said, “I’ve heard the term ‘bubble’ so much in the last couple weeks, and it’s a very action-oriented word that makes us all pay attention. But honestly, technical trends haven’t really given us any reason to be concerned.”

The same goes for recent choppiness in markets. “I don’t care if the market’s been sort of choppy and range-bound. In my view, despite the choppy short-term trends, longer-term trends are intact. And with sentiment remaining subdued, it seems to me that the path of least resistance remains to the upside over the next couple weeks.”

What about valuations, Newton was asked during our weekly research huddle. “Yes, everybody’s saying things are expensive. Well, compared to what? How do we know how to value AI?” he asked rhetorically. For him, metrics like the number of stocks near 12-month highs matters more. It could be bearish, he suggested, “if that percentage starts to roll over sharply,” but as of right now, it isn’t.

Lee concurs. The case for a rate cut from the FOMC arguably strengthened this week, and the confirmation that President Trump and China’s Xi Jinping will meet next week on Thursday alleviates yet another concern that has been bothering markets. Thus, Lee continues to view any dips that might emerge as buyable.

Chart of the Week

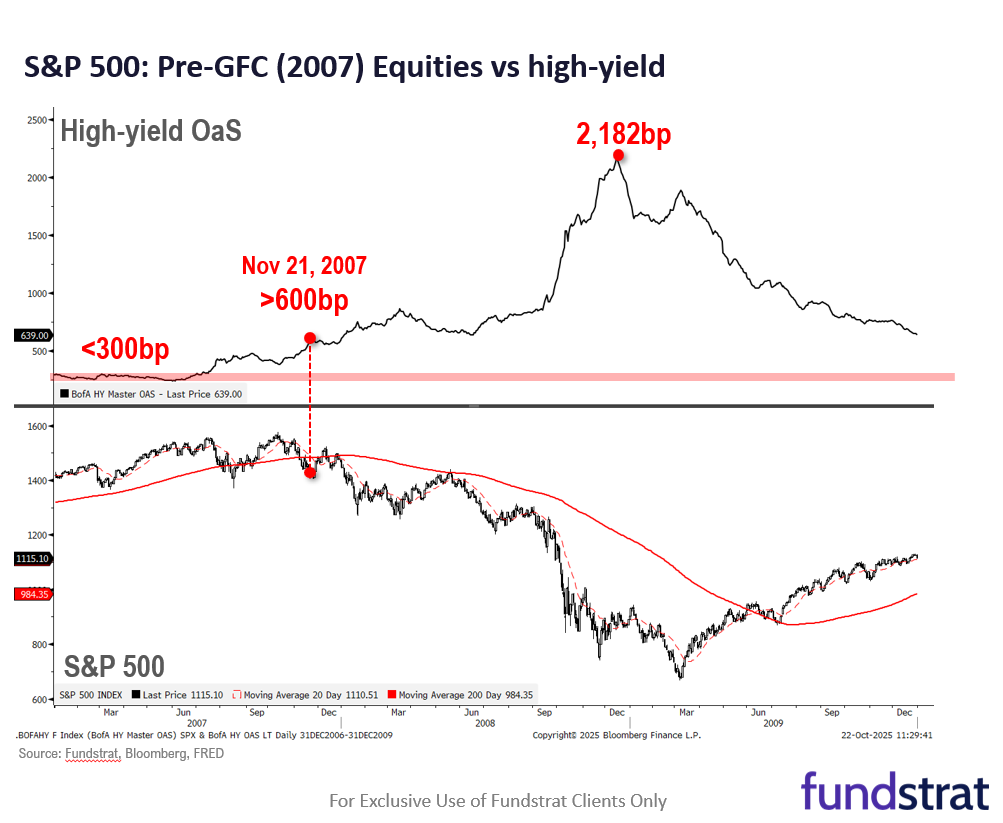

In the wake of the Tricolor and First Brands collapses as well as reports of losses by lenders like Western Alliance and Zions Bank, some market participants have developed flashbacks to the 2008 global financial crisis (GFC). As Bank of England Governor Andrew Bailey told MPs, “If you were involved [as a regulator] before the [GFC] and during it,” recent events had set off “alarm bells.” Fundstrat’sTom Lee remains largely unworried on that front. As he highlighted again this week, “if there are credit problems brewing, we should see it in high-yield spreads, but it’s hardly budged.” As he reminded us and as we see in our Chart of the Week, before the market topped in 2007, high-yield spreads were just under 300 bps, just about where they are today. On Nov. 21, 2007, about a month after the market topped, spreads doubled to 600. To Lee, that rapid doubling in the high-yield spread back in 2007 “was a warning sign,” so those worried about a possible GFC redux might wish to keep an eye out for a similar doubling re-emerging.

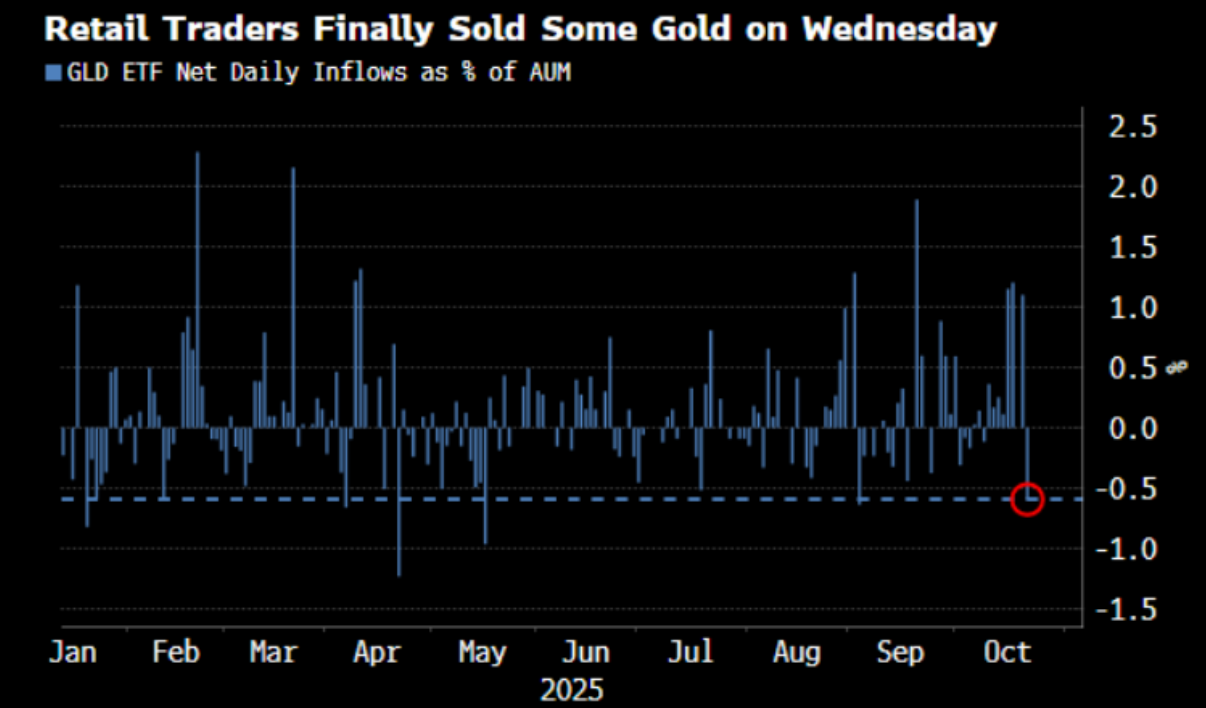

Gold ETF’s showed the largest outflow in Assets Under Management(AUM) since September on this week’s drawdown. Historically this tends to be bullish for a bounce when looking back since 2007 on a three, five, and 10-day horizon. (Bloomberg chart of GLD -0.37% ETF net daily Inflow as a % of AUM)

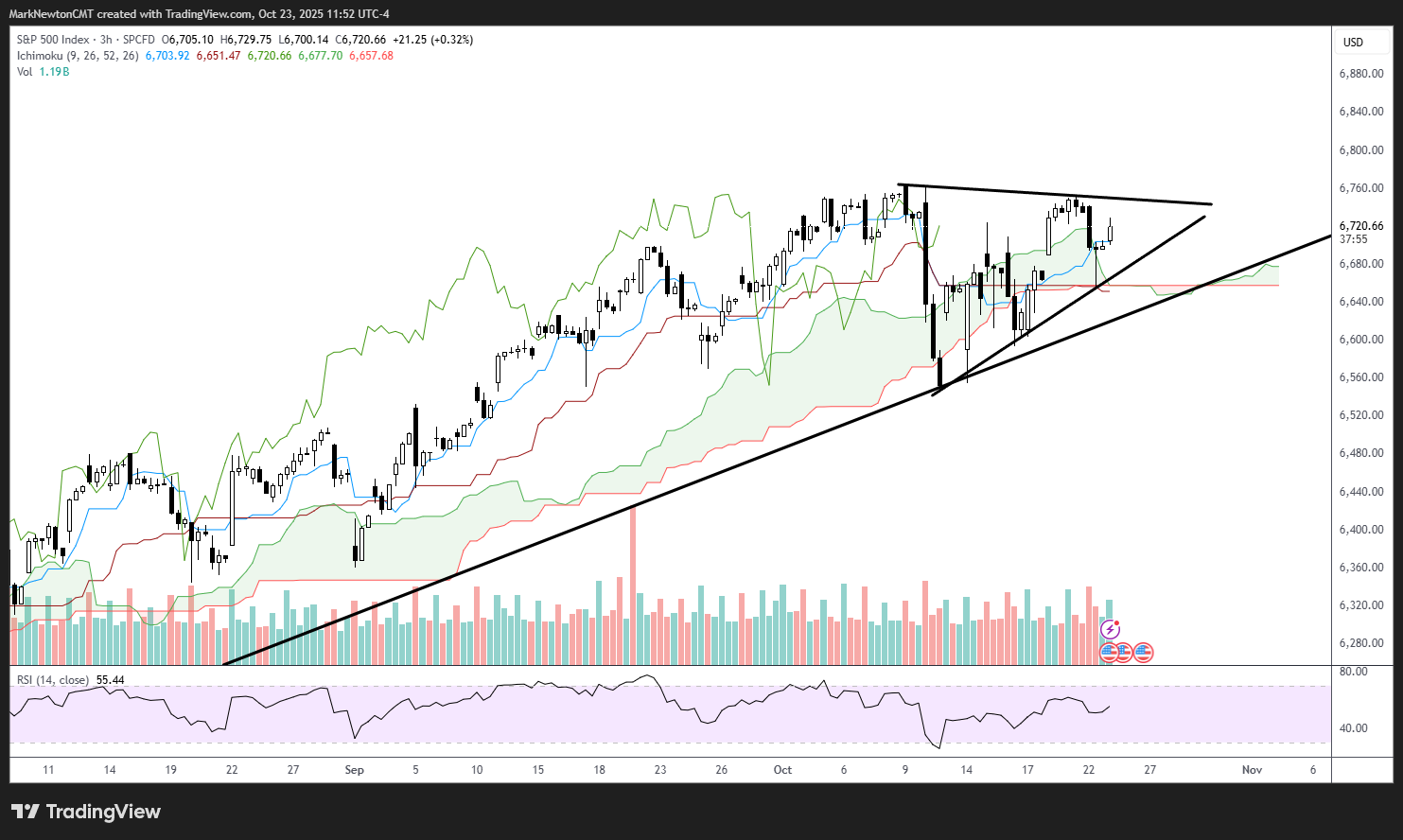

Very good stabilization in ^SPX which bottomed largely where it needed to (I had mentioned yesterday 6654 and SPX got to within 1 point of this, right at the 61.8% Fib levels of the prior low too high swing. This triangle now should allow for a push back to exceed this weeks highs and drive SPX back to new highs into late October. Key will be 6752 on the upside, which i expect to be surpassed, leading up to 6850-6950. For this to work, SPX cannot breach yesterday’s llows, so 6655 is a stop for longs and something which would result in patterns growing weaker short-term. Keep in mind, the larger area at 6550 is the line in the sand, overall and until this is broken, it’s right to simply be bullish and buy dips. However, today’s early push up is largely Technology driven, but also seeing strength from Materials, and Energy and some Industrials strength. REITS and Utilities are the main laggards today. Breadth levels aren’t too bullish just yet, at around 3/2 bullish, but this should change if/when 6752 is exceeded as i expect technically.

TSLA -3.34% hasn’t shown us much progress in the last month following its sharp rally into Oct 10, which proved to be near an exact six-month (180*) rally from our April lows. While the near-term pattern is choppy, one should position long if looking towards year-end, as both technical structure, momentum and cycles have improved since April. It’s extraordinarily difficult to have a timely short-term call on earnings given this choppy pattern, but i feel like a push up to 488 is likely before some consolidation into mid-Month. Thereafter, a move to new all-time highs happens which results in an acceleration which could carry TSLA north of $600. I remain quite bullish on TSLA despite the near-term range-bound activity,, and would use weakness over the next couple days (if this occurs) as a chance to buy dips. $411 is important support and a break of that would warrant patience as TSLA might reach 370-380 briefly before turning up sharply. However, a move back above $450 on a gap likely helps to reach all-time highs from last December at $488.54. In this case, i’m posting this ahead of earnings mainly to share my enthusiastic technical outlook between now and year-end and less about what happens directly after earnings. Given the choppiness of the last month, it’s important to pay more attention to intermediate-term structure.

This research is for the clients of FS Insight only. FSI Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or FS Insight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FS Insight. At the time of publication of this report, FS Insight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FS Insight is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

FS Insight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of FS Insight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by FS Insight clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of FS Insight, which is available to select institutional clients that have engaged FS Insight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

FS Insight does not have the same conflicts that traditional sell-side research organizations have because FS Insight (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by FS Insight and/or affiliates of FS Insight. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of FS Insight.

This research is for the clients of FS Insight only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but FS Insight does not warrant its completeness or accuracy except with respect to any disclosures relative to FS Insight and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where FS Insight expressly agrees otherwise in writing, FS Insight is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fsinsight.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.