The third quarter ended last Tuesday with the S&P 500 having hit 23 records as it climbed 7.8%. The broad-based index then proceeded to set fresh records on Thursday and brush up against yet another record on Friday before settling slightly to close the week in the green, at 6,715.79.

Head of Technical Strategy Mark Newton said that the S&P 500’s new records have positive technical implications for stocks. “This sets up for a push up to 6,749 in the short run, and potentially near 6,800 in mid-October before some consolidation starts to get underway.” He reiterated, “It looks technically right to trust that this rally has more to go.”

Yet perhaps the biggest headline this week was the federal government shutdown, which began at 12:01 a.m. right as Wednesday began. As Fundstrat’s Washington Policy Strategist Tom Block and Head of Data Science Ken Xuan noted, history suggests that government shutdowns do not tend to have lasting negative effects on the financial markets, even though some limited, short-term panic selling can take place at first.

That does not mean there’s no impact for investors, however. Friday was supposed to be the day the Bureau of Labor Statistics released the Nonfarm Payrolls numbers (aka the jobs report) for September. Thanks to the shutdown, this didn’t happen.

Fundstrat Head of Research Tom Lee suggested that if the shutdown continues past the next Federal Open Market Committee meeting on Oct.29 (the last shutdown in 2018 went on for 35 days), the lack of BLS jobs data could end up pushing the Fed in a dovish direction, which arguably would be good for stocks. Without any new jobs data, “the Fed most likely would have to rely on the August jobs report (weak),” and this would arguably require them to act with caution, he suggested. Another dovish consideration is that “the economy suffers from a shutdown, from lost activity,” Lee wrote, and the Fed is likely to take this into account as well.

In summation, Lee wrote: “I would not lean ‘bearish’ because of shutdowns. […] Shutdowns have rarely created lasting impacts on equities. There is a strong seasonal tailwind underway, and the upside is higher given the Fed is dovish.”

Chart of the Week

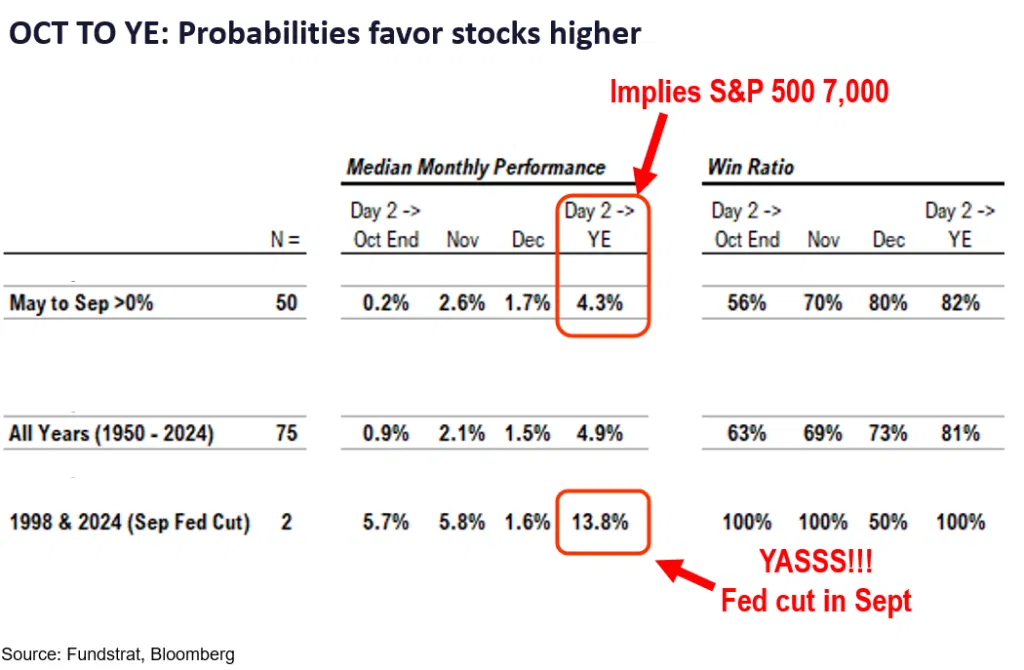

Amidst a rousing start to the fourth quarter, Fundstrat Head of Research Tom Lee noted that Q4 has historically been a strong period for stocks. Since 1950, stocks have notched a median gain of 4.9% in the period from October through December, with a win ratio of 81%.Two historical instances are particularly noteworthy: In both 1998 and 2024, the Federal Reserve cut rates in September after having been on pause since the beginning of the year – just as we’ve seen this year. The average Q4 gains in those precedent years is 13.8%. Details can be found in our Chart of the Weekabove.

Don’t look now but the formerly lagging Dow Jones Transportation Avg has made a bullish short-term triangle breakout today that likely can help to jump-start its performance at a time when the market is sorely seeking leadership from areas outside of Technology. I’ll discuss some of my favorites from this sector in tonight’s piece, but stocks like JBHT 2.79% LUV 0.65% ODFL 0.52% R 1.44% and CHRW are all up more than 2% today. It’s typically important to see the Transports confirm the bullish movement in the broader averages like SPX and DJIA from a Dow Theory standpoint, and while this will take some time, today’s constructive gains should lead this higher over the next few weeks. (TRAN)

While it might seem odd that the Equity market might rally as economic data gets weaker and a govt. shutdown gets underway, that’s exactly what technicals suggest at the moment. Recent Equity strength in the wake of Govt. Shutdown possibilities looks set to gain ground as the decline in Treasury yields on weaker data starts to reinforce the strong likelihood (based on Fed Funds futures pricing) of a near 100% certainty of a late October rate cut. (Keep in mind that Jobless Claims data might not be released this week given the Govt Shutdown) Early S&P Futures weakness of -0.50% overnight has improved to just -0.35% into today’s Market open, and yesterday’s strong close likely will push even further to the upside to test and exceed 6700 en route to near 6749. This level would allow the minor hourly swing of the last 24 hours to be equal in price terms to the one that began on 9/25 as an initial target to this rally. Cyclically, the next 1-2 weeks look likely to be bullish for US Equities and it will be important to keep a close eye on market breadth between now and mid-October.

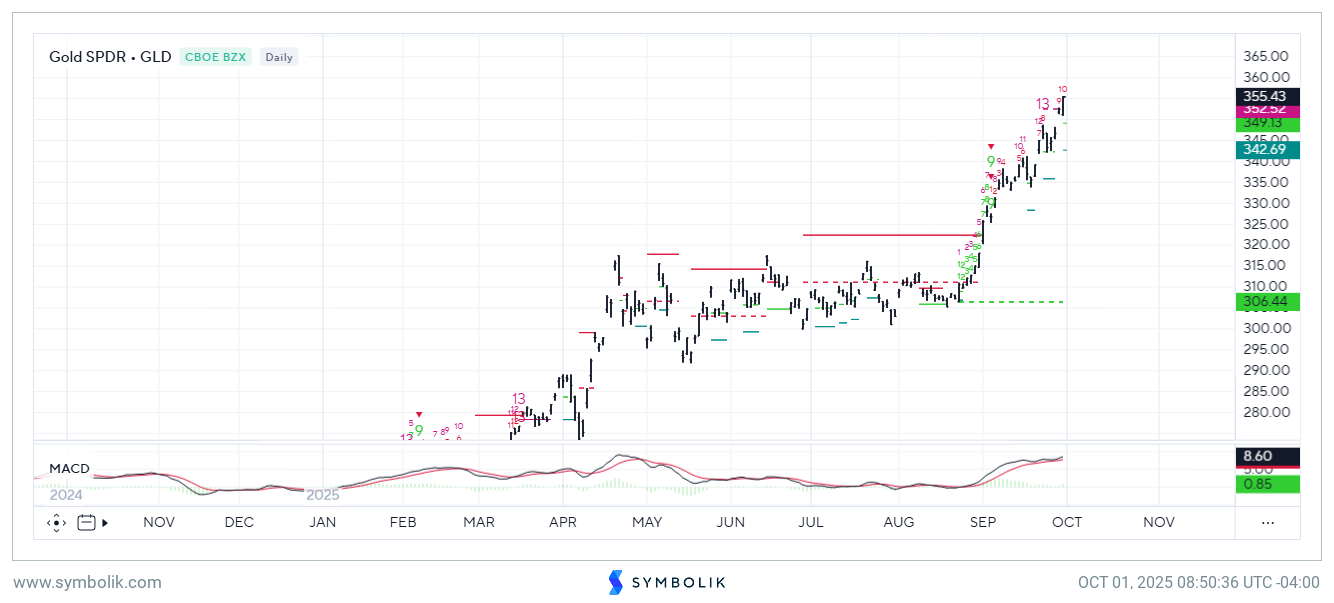

I’ve spent a few days in Dubai at the CMT Global Investment Summit this week and one of the few themes that everyone is talking about is how bullish Gold is from a technical and fundamental perspective. That’s scary to me as noone was discussing this when Gold bottomed three years ago in 2022. Many are mentioning macro themes to back up their bullishness like 1) “Govt Shutdowns being bullish for Gold, 2) Lack of Fed independence 3) Federal Bank buying 4) Declining Real rates and 5) Fiscal uncertainty and concerns. While i agree with all these points, Gold is very very stretched here and i recommend using a 5-day moving average now on all long positions, looking to exit as this moving average is undercut. This year’s 50% rally has barely had a decline of more than 3%, making this very different than 2023, when a number of 5-6% corrections happened as part of this rise. Using DeMark theory, there will be counter-trend Exhaustion “13 countdown signals” (Sells) potentially within 3 trading days, while the Weekly data could come into alignment within 2-3 weeks on both Gold and Silver. I’ve resisted suggesting to trim gains based on Daily DeMark signals in the past, but i suspect we could have a short-term peak by the end of this week given the parabolic move, if/when DeMark daily TD 13 signals appear on TD Sequential. Overall, i expect GLD 0.82% to likely have a target between 360-365, and Spot Gold might hit $4k before showing some backing off. However, normally i have suggested in the past that long-term positions might be better suited to await weekly signals before growing too defensive, and these continue to align towards mid-October.

This research is for the clients of FS Insight only. FSI Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or FS Insight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FS Insight. At the time of publication of this report, FS Insight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FS Insight is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

FS Insight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of FS Insight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by FS Insight clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of FS Insight, which is available to select institutional clients that have engaged FS Insight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

FS Insight does not have the same conflicts that traditional sell-side research organizations have because FS Insight (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by FS Insight and/or affiliates of FS Insight. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of FS Insight.

This research is for the clients of FS Insight only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but FS Insight does not warrant its completeness or accuracy except with respect to any disclosures relative to FS Insight and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where FS Insight expressly agrees otherwise in writing, FS Insight is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fsinsight.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.