Stocks set multiple new all-time highs last week, including on Friday when the S&P 500 closed at 6,388.64. Despite the broader index’s recent advances, sentiment remains restrained. Fundstrat Head of Research Tom Lee noted that anecdotally, “at Fundstrat, the feedback continues to be that many investors are skeptical of gains.”

Head of Technical Strategy Mark Newton concurred. “If you look at the overall levels of sentiment, it’s still pretty subdued,” he noted at our weekly research huddle. “We’re certainly not bearish anymore,” he acknowledged, “but we’re pretty much in neutral. We haven’t really gone to bullish territory yet, and we’re not really all that speculative.”

Even disregarding the new records set by the broader index, “the market continues to trade very well,” in Newton’s view. “In the last week, we’ve seen really good performance out of many of these groups that have not shown performance in quite some time. In general, this is a broadening out of the rally,” he said. Notably, “on an equal-weighted basis, tech actually hasn’t done as well as the others. There are other sectors that have actually started to outperform tech, which I think is a positive.”

We are about a third of the way into earnings season, and perhaps two of the most watched earnings reports last week were Alphabet (GOOG 1.24% ) and Tesla (TSLA -1.50% ). Tesla, of course, had faced some challenges since the beginning of the year, and many investors appeared to interpret Elon Musk’s remarks as subdued. From a technical perspective, however, Newton noted that “despite the gap down the day after its earnings report, I see the stock being a good intermediate-term risk/reward for the second half of this year.” As a caveat, he warned that a break of July lows at $288.77 might temporarily affect his current constructive view of the stock, but “at present, I don’t expect this to happen.”

As for Alphabet, the tech giant surged after reporting a 14% increase in second-quarter revenue. Investors appeared to find much to like in chief executive Sundar Pichai’s remarks, which included upbeat views about AI supporting the company’s cornerstone search-engine revenues and a $10 billion increase in its 2025 capex forecast to $85 billion.

That’s consistent with Lee’s continued view that AI demand remains strong, and AI itself is a multi-decade story. After attending a Hill & Valley Forum co-hosted by the All-In podcast (where President Trump on Wednesday signed three executive orders regarding AI), Lee also noted that, “To me, the key takeaway is that there are many instances of AI helping existing workers multiply their skills, so perhaps AI will not replace as many jobs as feared.” Looking into next week, with the release of June PCE data, a rate decision from the Federal Open Market Committee, and 163 earnings reports on deck, Lee “[expects] equities to end July on a high note. We do not think the final weeks of July are a concern.”

Chart of the Week

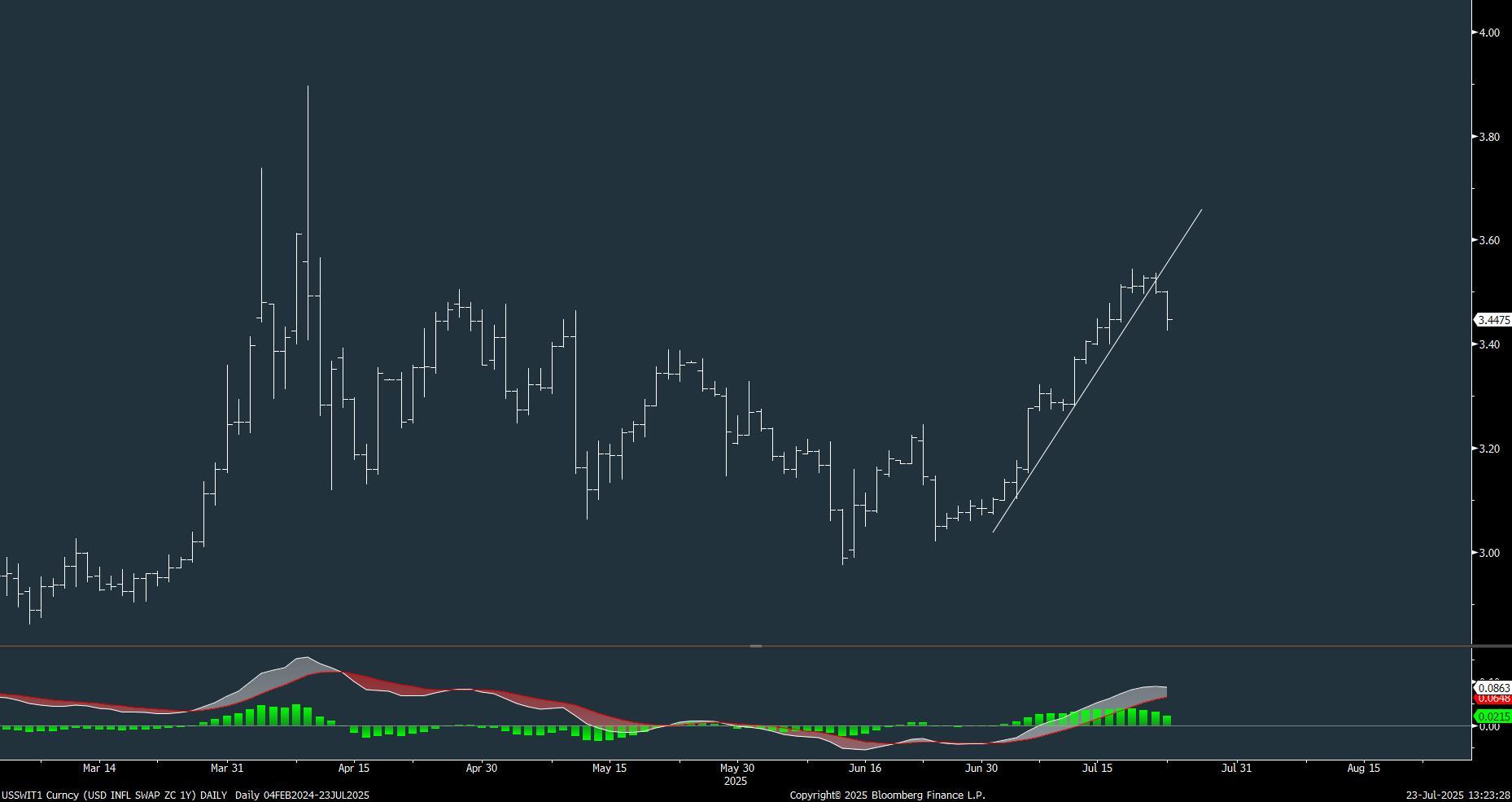

Although it was a relatively light week for fresh macroeconomic data, markets were buoyed by the announcement of three trade deals — Indonesia, the Philippines, and Japan, as seen in our Chart of the Week.

1-year Inflation swaps rolled over sharply today given the news of the US-Japan trade deal and are extending the drop given that US seems to be closing in on a similar deal with Europe. Meanwhile US Treasury yields are rising despite a very good 20-year auction today on very strong demand. The Bid/cover of 2.79 was the highest since last April. Thus inflation expectations are dropping & US Equities have managed to sustain the rally from this morning. This break in the one-month uptrend on Inflation swaps likely can continue to result in Inflation expectations falling given the nature of this technical break.

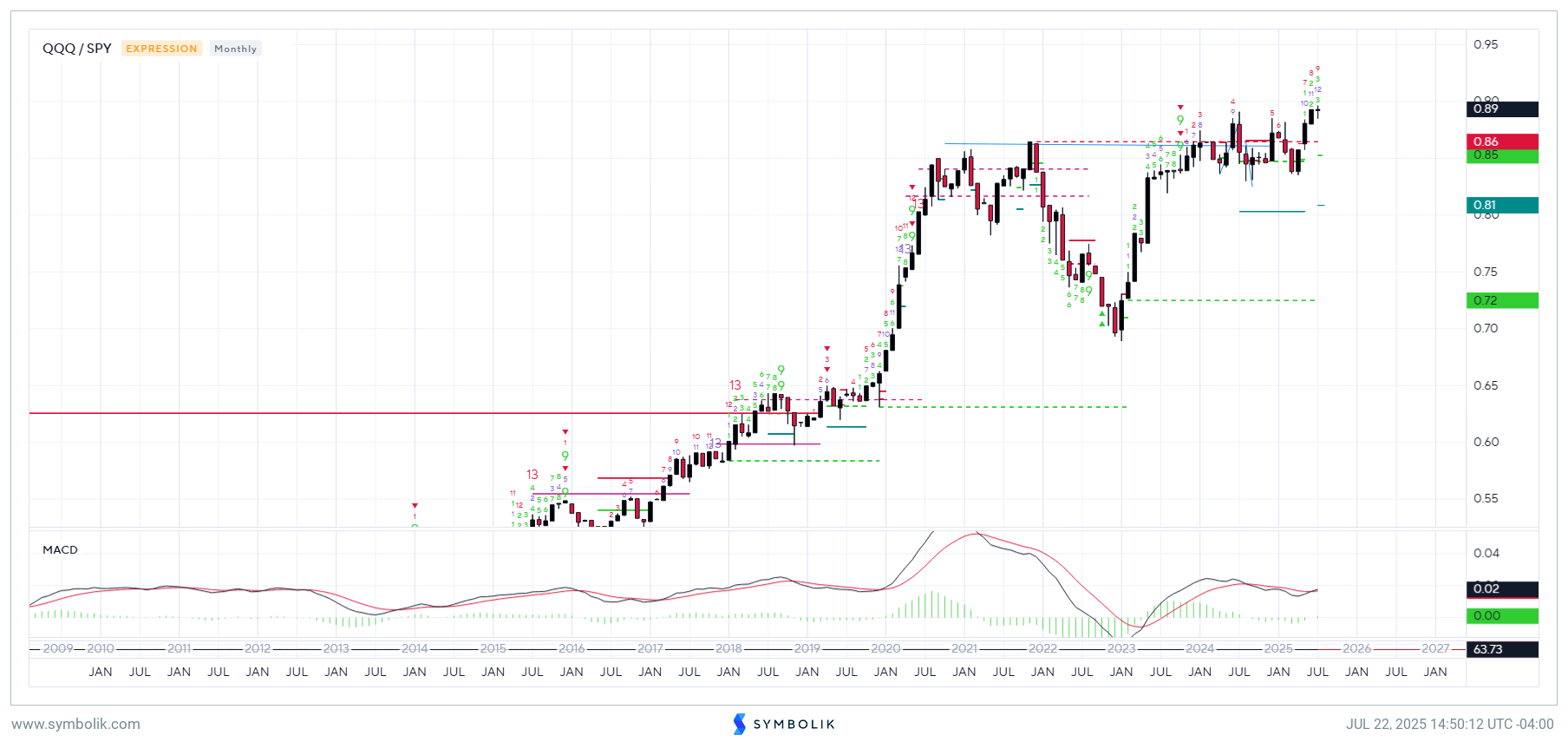

Despite some weakness in many Semiconductor names today, the ratio of QQQ 0.30% vs. SPY 0.42% still looks early to peak out by at least a few weeks. This has been persistently strong off the April lows, breaking out above a meaningful 5-Year cup and Handle pattern, and should be able to trend up for at least another month (and potentially three-months ) before much resistance. Thus QQQ 0.30% might be able to carry higher than many investors expect, and i anticipate a push up to 580-590 before much serious resistance and/or counter-trend exhaustion. Overall, despite a 1-day period of underperformance for Tech vs. the broader market, i don’t think it should prove too serious in July.

Many investors have noted that VIX is at a higher level now than back on 7/10 despite SPX being higher by roughly ~50 points. When looking at intra-day and Daily VIX charts for evidence of exhaustion signals that might point to a possible reversal, we see that this remains premature by at least 3-5 trading days, but could be generated on a pullback in VIX down to challenge VIX lows from 7/10. I am expecting that a “flush” in VIX should be approaching that likely represents a very attractive area for buying implied volatility for the next 2-3 months. I had discussed last month that 16.50 area was certainly an appealing level, but VIX very well might weaken to test and break 15.70 into late July. If this happens, then it would present an even better risk/reward opportunity. My expectations is that VIX likely will bottom out by late July/Early August and begin to trade higher to the mid-20’s at a minimum, but possibly reach the low 30’s into late September. At present though, my analysis suggests a bit lower VIX over next week ahead of a bottom.

This research is for the clients of FS Insight only. FSI Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or FS Insight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FS Insight. At the time of publication of this report, FS Insight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FS Insight is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

FS Insight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of FS Insight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by FS Insight clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of FS Insight, which is available to select institutional clients that have engaged FS Insight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

FS Insight does not have the same conflicts that traditional sell-side research organizations have because FS Insight (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by FS Insight and/or affiliates of FS Insight. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of FS Insight.

This research is for the clients of FS Insight only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but FS Insight does not warrant its completeness or accuracy except with respect to any disclosures relative to FS Insight and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where FS Insight expressly agrees otherwise in writing, FS Insight is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fsinsight.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.