A daily market update from FS Insight — what you need to know ahead of opening bell

“There is no quality in this world that is not what it is merely by contrast. Nothing exists in itself.” — Herman Melville

Overnight

Fed officials remain worried that inflation could stop cooling, minutes show

English video to investors shows Japan banks waking to change

China slowdown deals $3 billion blow to HSBC

Iran sends Russia hundreds of ballistic missiles

Biden administration cancels another $1.2 billion in student debt covering 153,000 borrowers

Guyana won’t approve drilling by Exxon near Venezuela until ICJ issues a ruling

Seizing frozen Russian assets over Ukraine war wins endorsement of legal experts

Amazon plans to sunset Freevee, its free ad-supported video streaming service

Rivian is laying off 10% of its salaried workforce amid challenges

Chord Energy, Enerplus to combine in $11 billion deal

First news

- Ford is careful to forge a deal with a UAW local, protecting continued production at one of its most profitable plants

- China’s ‘Broker Butcher’ regulator comes after short sellers, quant trading funds

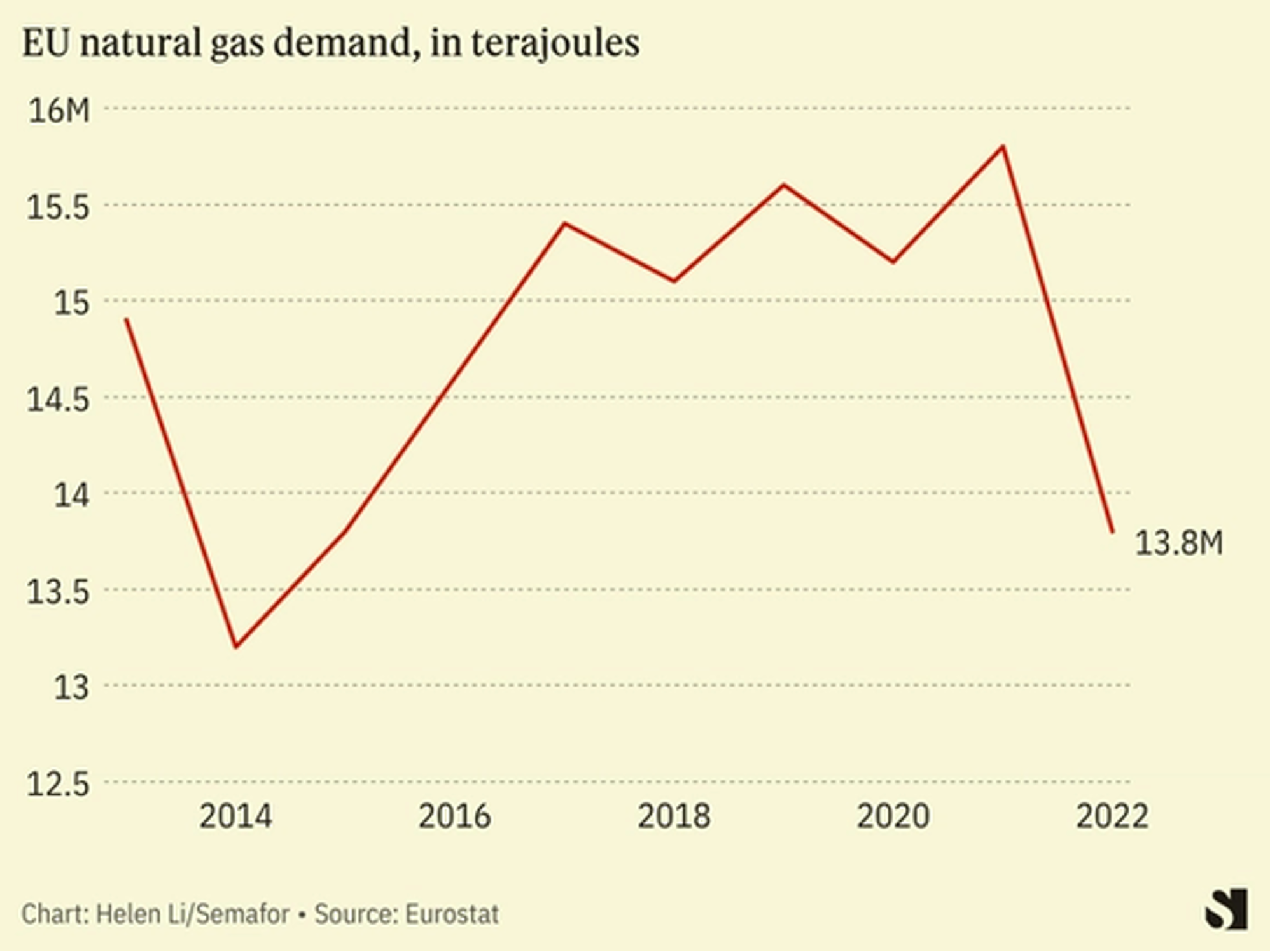

- Europe is high on natural gas infrastructure, lower on gas demand

- True to its maverick spirit, Reddit will offer 75,000 of its most ardent participants access to upcoming IPO.

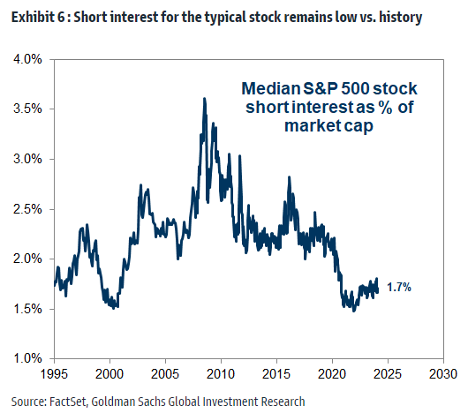

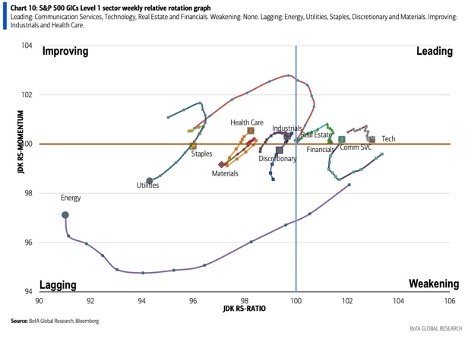

Charts of the Day

MARKET LEVELS

| Overnight |

| S&P Futures +58

point(s) (+1.2%

) overnight range: +19 to +61 point(s) |

| APAC |

| Nikkei +2.19%

Topix +1.27% China SHCOMP +1.27% Hang Seng +1.45% Korea +0.41% Singapore +0.18% Australia +0.04% India +0.74% Taiwan +0.94% |

| Europe |

| Stoxx 50 +1.03%

Stoxx 600 +0.58% FTSE 100 +0.03% DAX +1.12% CAC 40 +0.67% Italy +0.95% IBEX +0.36% |

| FX |

| Dollar Index (DXY) -0.35%

to 103.64 EUR/USD +0.33% to 1.0855 GBP/USD +0.31% to 1.2677 USD/JPY -0.09% to 150.17 USD/CNY -0.01% to 7.1908 USD/CNH -0.03% to 7.1969 USD/CHF -0.23% to 0.8776 USD/CAD -0.36% to 1.3457 AUD/USD +0.52% to 0.6585 |

| Crypto |

| BTC +0.58%

to 51685.62 ETH +2.42% to 2998.46 XRP +0.04% to 0.5465 Cardano +1.32% to 0.6002 Solana +0.82% to 105.92 Avalanche -0.11% to 37.57 Dogecoin +0.83% to 0.0848 Chainlink +1.8% to 18.74 |

| Commodities and Others |

| VIX -7.37%

to 14.21 WTI Crude +0.41% to 78.23 Brent Crude +0.37% to 83.34 Nat Gas -1.86% to 1.74 RBOB Gas -0.1% to 2.284 Heating Oil +0.11% to 2.708 Gold +0.19% to 2029.8 Silver +0.85% to 23.08 Copper +0.04% to 3.876 |

| US Treasuries |

| 1M -1.9bps

to 5.3647% 3M -1.6bps to 5.372% 6M -2.5bps to 5.3188% 12M -2.2bps to 4.9552% 2Y -0.2bps to 4.6644% 5Y -1.2bps to 4.292% 7Y -1.1bps to 4.3153% 10Y -1.6bps to 4.3029% 20Y -2.8bps to 4.5756% 30Y -1.6bps to 4.4619% |

| UST Term Structure |

| 2Y-3

M Spread narrowed 0.1bps to -74.1

bps 10Y-2 Y Spread narrowed 1.4bps to -36.4 bps 30Y-10 Y Spread widened 0.0bps to 15.7 bps |

| Yesterday's Recap |

| SPX +0.13%

SPX Eq Wt +0.2% NASDAQ 100 -0.38% NASDAQ Comp -0.32% Russell Midcap +0.05% R2k -0.47% R1k Value +0.46% R1k Growth -0.25% R2k Value -0.07% R2k Growth -0.87% FANG+ -0.42% Semis -0.64% Software -2.8% Biotech +0.1% Regional Banks -0.66% SPX GICS1 Sorted: Energy +1.86% Utes +1.36% Cons Disc +0.72% REITs +0.72% Materials +0.57% Indu +0.42% Fin +0.31% Cons Staples +0.29% Healthcare +0.26% Comm Srvcs +0.2% SPX +0.13% Tech -0.76% |

| USD HY OaS |

| All Sectors -2.6bp

to 370bp All Sectors ex-Energy -2.6bp to 354bp Cons Disc -1.0bp to 308bp Indu -1.8bp to 281bp Tech -2.3bp to 452bp Comm Srvcs -4.7bp to 589bp Materials -4.4bp to 325bp Energy -2.9bp to 301bp Fin Snr -5.6bp to 344bp Fin Sub -2.7bp to 249bp Cons Staples -2.4bp to 306bp Healthcare +3.0bp to 459bp Utes -3.6bp to 222bp * |

| Date | Time | Description | Estimate | Last |

|---|---|---|---|---|

| 2/22 | 9:45AM | Feb P S&P Manu PMI | 50.7 | 50.7 |

| 2/22 | 9:45AM | Feb P S&P Srvcs PMI | 52.3 | 52.5 |

| 2/22 | 10AM | Jan Existing Home Sales | 3.97 | 3.78 |

| 2/22 | 10AM | Jan Existing Home Sales m/m | 4.9 | -1.05 |

| 2/26 | 10AM | Jan New Home Sales | 685.0 | 664.0 |

| 2/26 | 10AM | Jan New Home Sales m/m | 3.2 | 8.0 |

| 2/27 | 8:30AM | Jan P Durable Gds Orders | -4.5 | 0.0 |

| 2/27 | 10AM | Feb Conf Board Sentiment | 114.75 | 114.8 |

| 2/28 | 8:30AM | 4Q S GDP QoQ | 3.3 | 3.3 |

MORNING INSIGHT

Good morning!

We think it is too early to declare an AI a bubble, looking back at dot-com and Nikkei surges, in both of which a massive drawdown was seen at the midpoint, with both then seeing a further 10X increase. We see similar developments with AI from here.

Click HERE for more.

TECHNICAL

QQQ 0.36% vs SPY 0.24% While this recent consolidation since 2/12 has proven gradual and not technically damaging to trends in US stock indices, there has been a persistent underperformance in QQQ vs. SPY, which has been ongoing for roughly two weeks. This does not seem complete, and could last another 3-5 trading days before bottoming and turning back higher. The key takeaway here: QQQ has underperformed due to selective Technology weakness, but this has not been damaging to the US stock market as other sectors have shown some ability to play catch-up. QQQ is likely to underperform SPY over the next week, and RSP should outperform SPY.

^TNX 1.12% US 10-Year yields are, we feel, in the process of making a push higher over the next week, which should reach at least 4.41% and potentially 4.51-4.55%, but should prove short-lived in both duration and magnitude. Thereafter, yields are likely to roll over in March, and this should coincide with a broad-based rally in U.S. stocks. Near-term, one should hold off on adding duration for about a week, as yields are likely to move higher.

Click HERE for more.

CRYPTO

- The Hong Kong Monetary Authority (HKMA) released comprehensive regulations surrounding the sale and distribution of tokenized financial products. The standards hope to encourage innovation while protecting consumers who want to invest in tokenized financial products. The release outlines the type of products that fall within the new regulatory umbrella, excluding products that are already covered by the Securities and Futures Ordinance and regulations specified by HKMA and the Securities and Futures Commission (SFC). Requirements include institutions conducting thorough diligence on issuers and third-party service providers and providing necessary disclosures that properly notify consumers of the risks associated with tokenized investments. Additionally, institutions must develop risk management frameworks outlining procedures, systems, compliance controls, and business continuity plans. Honk Kong has been very friendly to the digital asset industry, and the new framework is a response to rapid developments and increased demand for tokenization. The new guidelines should provide clarity to financial institutions and accelerate the adoption of tokenized products.

- Circle has announced that customers will no longer be able to mint USDC on Tron, citing their risk management framework. Circle noted that they continually assess the suitability of all blockchains where USDC is supported, and the discontinuation aligns with Circle’s efforts to remain trusted, transparent, and safe. The amount of USDC on Tron is relatively small in comparison to total supply, with approximately 305 million out of 26.8 billion being utilized on Tron (1.12%). Tether is the market leader on Tron, with over 49.6 billion tokens, representing approximately 50% of USDT supply. Circle will continue supporting USDC redemptions on Tron through February 2025. Circle is advising any retail or non-business holders of USDC to send their holdings to centralized exchanges or other networks.

Click HERE for more.

FIRST NEWS

Protecting Revenues at a Cost It Can Bear. Ford and UAW Local 62, a United Auto Workers local, managed to come to a tentative agreement on Wednesday, averting a strike at the automaker’s most profitable manufacturing facility. Before Wednesday, the UAW was menacing Ford with a Friday walkout by ~9,000 workers at its Kentucky truck plant. The deal addresses local issues related to skilled trades, ergonomics, and health & safety.

Given that the plant produces high-margin Ford Super Duty pickups, Ford Expeditions, and Lincoln Navigator SUVs, Ford was smart to avert the strike, which gave it the well-deserved right to be quoted in a statement to the effect that it was “pleased to have reached a tentative agreement” covering the Louisville plant – its largest in terms of employment and revenue. CNBC

Go Long or Get Cut. As economic growth has slowed dramatically and the country’s property market is showing signs of collapse, investors have been selling Chinese equities. Now, in efforts to boost its struggling stock market, China is imposing far-reaching new rules on short sellers. Quant trading funds, which use complex automated trading programs, will now be subject to toughened rules; required to report their investment strategies ahead of time. Major institutional investors are now banned from selling equities at the start and end of each trading day. This is the Chinese government’s most forceful attempt yet to buttress the country’s $8.6 trillion stock market.” These changes were expected by savvy observers. Two weeks ago, China appointed a new security regulator nicknamed the ‘Broker Butcher’ on account of his previous crackdowns on traders. Enforcement will be no joke: the regulator is creating a task force to track short selling. Semafor

High on Power, Low on Will. A new analysis by the Institute for Energy Economics and Financial Analysis shows that natural gas demand on the Continent has dropped by 20% compared to usage at the moment of Russia’s invasion of Ukraine almost two years ago. The trend is thought to be driven by weaker sales in Germany, the U.K., Italy, and other countries. Europe’s liquid natural gas consumption hit a 10-year low in 2023 as, spurred by the war, countries boosted efficiency measures and picked up the pace of the transition to renewable energy. Still, Europe continues to build natural gas infrastructure: eight new terminals have come online since February 2022 and 13 others are scheduled for completion by 2030. Should demand continue to decline, Europe’s import capacity could be three times its demand by that time. Perhaps, in line with the move toward renewable energy, it could convert them to handle naturally occurring hydrogen, of which there are apparently trillions of tons worldwide. Semafor

Public Square Goes Public; ‘Power to the People!’ Reddit, the weird and wonderful home of ‘the internet’s front page’, is planning to do something very grown up next month – go public. In the spirit of its informal, familial DNA, Reddit plans to reward its most loyal users; 75,000 of the platform’s “redditors”; with the chance to buy shares at the IPO price, before the stock starts trading – an opportunity generally reserved for sizable money managers, not people in pajamas serving up snark and spark late into the night via overpowered laptops.

The unusual move could help build even greater loyalty for the soon-to-be-public company, although possibly at the price of volatility in the stock. After all, the meme stock frenzy (think GameStop, AMC, Tesla, et al) began on Reddit and proved the power of the platform to mobilize retail investors. Reddit separately announced yesterday that, over the next decade, it will be setting aside 1% of common stock to fund community-related programs through the Pledge 1% nonprofit. WSJ