US Equity markets likely could be peaking out and Thursday might have officially served as the technical catalyst for confirmation. US and European sovereign yields along with US Dollar index and Yen look to strengthen short-term before turning back lower in August 4350-4400 looks possible for SPX on weakness into mid-August before rally continues

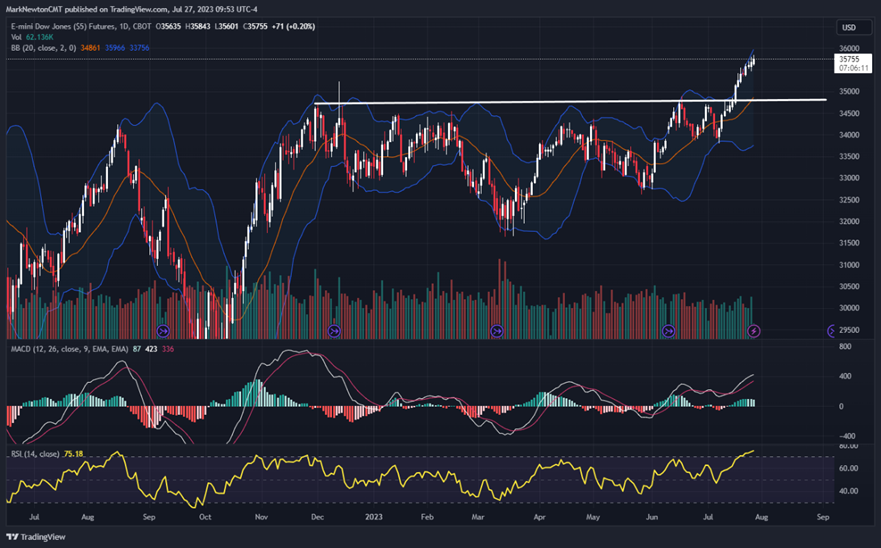

Don’t look now, but Thursday’s rapid trend reversal looks to potentially be the technical catalyst for the warning signs I have discussed over the last week. S&P, DJIA and NASDAQ all pulled back sharply from early day highs and SPX, DJIA, Russell 2000 all made bearish engulfing patterns in sweeping under lows of the last few days in Thursday’s trading.

DJIA came very close to achieving the unthinkable in recording the longest consecutive rally on record, spanning 14 straight days. Despite Thursday’s reversal, DJIA has still achieved an impressive ~2000 point rally, just since mid-July, which was specifically driven by the breakout of $34588, an important technical catalyst. Even at current levels, DJIA is only roughly 2% from all-time weekly closing highs.

As mentioned earlier this week, the chief warning signs of a potential pullback were based on the following :

- Counter-trend exhaustion based on DeMark indicators on numerous timeframes

- Daily breadth and momentum divergence (Only daily charts, not weekly)

- Sentiment has ratcheted up in short-term (NAAIM readings came in bullish today)

- Defensive trading saw a notable uptick over the last month (Note, Utilities and REITS are giving back a bit on yields spiking )

- Bearish seasonality -August has been bearish for US Stocks during pre-election years

- Cycles turn lower into late August before turning higher

Overall, I’ll monitor whether this was indeed a meaningful short-term peak and can discuss more in tomorrow’s note. This happened to occur directly in line with cycle composites just as DeMark exhaustion had reached fruition. Breaking SPX 4500 would serve to give more conviction in this regard, but it looks like 10-yr yields jumping up above 4.00% served to spook markets, and this rally in Yields does not yet look complete.

In the days/weeks ahead, adopting a “Buy the Laggards” approach looks prudent technically. Owning Chinese Equities, areas like Pharmaceuticals and Biotechnology within Healthcare, along with scouring the various DJIA laggards for signs of bottoming might make sense (MMM 1.72% yesterday made a breakout from a two-year downtrend after having been cut in half) Financials, Technology, and Consumer Discretionary (particularly Large-cap) look vulnerable in August.

DJIA chart below showing “why” this trended higher so sharply over the last three weeks. Much of this was due to the larger trend breakout. A pullback to near $34,588 looks possible in August.

S&P bearish engulfing pattern looks like a negative technical catalyst for selling pressure

A big bearish reversal happening right as cycles were due to turn down makes Thursday’s reversal particularly important as a negative development which could coincide with markets finally showing some weakness.

As detailed, the entire bear market of 2022 lasted 40 weeks and now has risen 40 weeks. This area has importance time-wise and directly coincides with a minor cyclical top.

While trends technically still haven’t been broken on SPX, nor NASDAQ, the bearish engulfing pattern given yields spiking looks important, as yields and US Dollar’s reversals today look to continue a bit higher.

Bottom line, under SPX 4500 likely leads to 4350-4400 into late August and I view Thursday’s reversal as being important and a short-term negative.

Steel stocks are on the verge of breaking out to the highest levels in over a decade

Weekly charts of SLX 0.50% , the VanEck Steel ETF, is getting set to make a larger breakout of the consolidation which has been intact since 2021.

While a US Dollar Rally on BOJ yield curve control timing changes along with yield spike could result in short-term pullbacks in SLX, this should set up for an excellent risk/reward opportunity on weakness down near $66-67.

Stocks like RS -1.19% , STLD 0.32% , MT 0.94% , ASTL -1.55% could all prove to benefit on SLX pushing up to new multi-month highs.

Gold stocks likely weaken a bit short-term given Yields and Dollar spiking; I feel this provides buying opportunity into August

Gold stocks likely will face some near-term downward pressure as real rates move higher in the short run. While I don’t anticipate this proves long-lasting, ETF”s for Gold stocks like GDX 4.73% , the VanEck Gold Miners ETF, could weaken down to test strong support near $29-$29.50 into early August before an important bottom and reversal back higher.

This selling pressure appears short-term only and does not take away from the bullish intermediate-term call on precious metals. Individual names like NEM 5.80% which I just added to UPTICKS this week, should present attractive buying opportunities on weakness over the next week.

US Treasury yields could strengthen on a 3-5 day basis; However, I don’t expect movement over TNX-4.20%

This rapid about-face for Yields looks to extend a bit more in the near-term and TNX could reach 4.10% before stalling out with a likely maximum lift to 4.20%.

Overall, my cycle composite along with wave structure both suggest that any near-term backing up in rates should prove short-lived at the present time.

Thus, TLT -0.09% or IEF -0.13% likely could be considered attractive risk/rewards for buying dips into early August as I do not anticipate that yields push up to new highs for 2023 on this recent spike.

However, the act of both TYX and TNX having eclipsed 4.00% is certainly a short-term negative for stocks psychologically, given that stocks reversed sharply just as the acceleration in both yields and US Dollar got underway Thursday afternoon. It should be important to pay close attention to the Bank of Japan’s Friday announcement for additional clues, as their yield curve control program might also affect US Treasuries.