Electric vehicles (EVs) are the future – or at least zero-emissions vehicles are, and that’s close enough to being the same thing, since hydrogen fuel-cell vehicles, the only other option currently available, are not nearly as widely accepted. Even Lamborghini apparently agrees: Earlier this month, the iconic Italian sports-car manufacturer announced that it had taken the order for the last all-gas/internal combustion engine (ICE) vehicle it will ever make. Going forward, a gearhead seeking to buy a blisteringly fast Lambo will only have hybrids and electrics as options.

That’s not surprising: Norway is well on the way to the EV future – in 2022, 80% of all new car sales were of electric vehicles, and by 2025, sales of new internal combustion vehicles will be banned there. There will be a similar ban on new-car sales of ICE vehicles by 2035 in both the European Union and Japan – as well as the state of California. The South Korean government has a raft of policies and incentives in place to encourage the EV transition. Meanwhile, China, the largest market for cars, is incentivizing domestic purchases of electric vehicles through tax breaks, registration-fee discounts, and subsidies for charging-station construction.

In the United States, the Biden administration in April 2023 proposed strict new emissions rules for automakers that essentially require them to shift 67% of their production to electric vehicles by 2032. This was the latest in a series of efforts by the White House to facilitate and speed the U.S. transition from fossil fuel-burning vehicles to electric vehicles. The U.S. has also implemented tax incentives for vehicle producers and purchasers, manufacturing incentives for producers of EV components and batteries, subsidies to speed the building out of the U.S. public EV charging network, incentives to electrify heavier vehicles such as school buses.

The thinking behind these policies is a combination of concerns. Climate change is a primary motivation. But so too are the perceived economic benefits. With consumers increasingly willing to consider buying an EV over an ICE vehicle, countries understandably want to position themselves to get ahead of what is widely seen to be a growth industry.

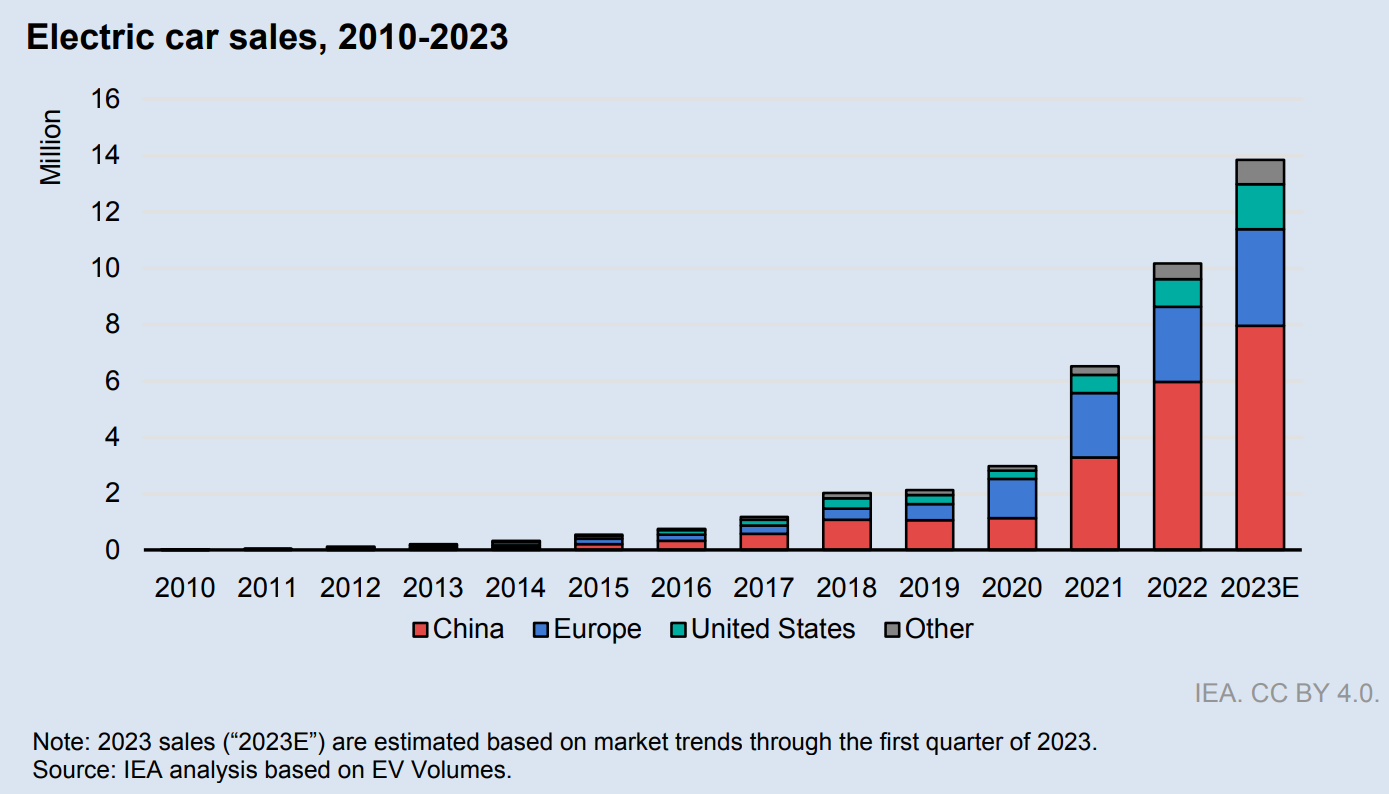

The various governments are not trying to create a trend out of thin air. According to the International Energy Agency (IEA), electric cars accounted for less than 5% of new car sales in 2020, rose to 9% the next year, and hit 14%, or 10 million, in 2022. In the U.S market, EV sales rose 55% in 2022, though still accounting for only 8% of new-car sales.

The odds seem good that over the next decade, electric vehicles will account for an increasingly large percentage of new car sales – and eventually car ownership. That suggests potential opportunities for companies in several key industries – and for their investors.

The obvious players: EV manufacturers

Right now, Tesla (TSLA 0.20% ) is by far the largest manufacturer of electric vehicles around the world. But in its Q2 2023 results, the company acknowledged that it was facing increased competition.

This is good for the EV revolution, which needs more than one company to perform well in order to take hold. One of Tesla’s advantages over traditional or legacy automakers has been its relatively small product line, which has helped the company lower manufacturing costs and thus improve margins.

But consumers like having options – not just because it gives them a feeling of control, and not just because that’s how the automobile market has always worked. It is unlikely that any single manufacturer could ever hope to effectively provide the breadth of choices that customers demand.

Currently, the largest manufacturers of EVs (not including hybrid vehicles) are:

BYD Co. Ltd. (BYDDY)

The Chinese manufacturer has reached the No. 2 spot despite eschewing the large and lucrative U.S. market – and repeatedly noting that it has no plans to enter. While Tesla autos started out targeting higher-income buyers before diversifying its offerings somewhat, BYD got where it is by looking to lower-income Chinese buyers.

Volkswagen Group (VWAGY)

In addition to its namesake brand, Volkswagen also owns brands including Audi, Bentley, Cupra, Porsche and the aforementioned Lamborghini. Volkswagen, Audi, Cupra (a Spanish brand), and Porsche already have electric models on the market. The company has also funded research into EV batteries (see below), expanded its battery-production capabilities, and taken part or led several initiatives to expand charging networks in Europe and the United States.

General Motors (GM 2.87% )

General Motors is no newcomer to the electric vehicle market – at least not technically. The company claims to have made the first mass-produced electric vehicle of the modern era with the 1996 EV1, which was leased to about 1,100 customers to test the waters for a new product. GM at the time decided that electric vehicles could not be made profitably, so it had almost all the EV1s destroyed. It clearly feels differently now, aggressively expanding into this segment – the company has plans to introduce dozens of new EV models by 2025, for both consumer and commercial markets. Like Volkswagen, GM has also made significant investments of EV-related research and development.

Also critical: public charging stations

One of the biggest sources of reluctance for consumers considering a switch from ICE vehicles to EVs has to do with the inability of EVs to offer the same kind of convenience as ICE vehicles, whose drivers are almost always just a few miles away from a gas station where they can fill up their gas tank in a few minutes.

At first glance, it would seem that this should not be a major impediment for electrics. EV owners typically charge their vehicles at home overnight. With the slowest Level 1 charging (using an adapter to plug the vehicle into the ubiquitous 120V AC plug that powers most consumer devices), eight hours of overnight charging can add about 40-50 miles of range. Owners who opt to pay about $1,500 to install a 240V connection (the kind that powers devices like electric clothes dryers and cooking ranges), can generally get a full charge overnight, equivalent to between 59 to 426 miles, depending on model, speeds being driven, and outside temperature (range decreases when the weather gets colder.)

Level 2 chargers are also useful for charging stations at public venues where people tend to spend hours on end – the parking lots of office buildings, shopping malls, or movie theaters, for example, as they can add about 25 miles of range per hour of charging.

With the average U.S. driver putting about 37 miles a day on their vehicles, this should be perfectly sufficient most of the time. But during unexpectedly busy days or road trips, and for peace of mind, customers want the same kind of convenience offered by gas stations and gas-powered automobiles. In addition, owners and operators of commercial vehicles – including delivery trucks, buses, and taxi/ride-share vehicles – often do not have the luxury of waiting hours for a full recharge.

That requires high-speed charging, the kind that can deliver 100 miles of range in about 10 minutes or a full charge in 30 minutes. Right now, that primarily means Level 3, direct-current (DC) charging stations. The problem? There aren’t very many of them, probably because installation requires a construction crew, heavy equipment, and $80,000 or more. What’s more, localized power-grid inadequacies mean that they cannot be installed at all in some places.

The expansion of publicly available high-speed charging stations plays a key role in every country that wants to encourage a shift to EVs. Currently, Tesla is the largest operator of public charging stations in the world, including 17,000 superchargers in the U.S. alone. Those chargers were originally exclusive to Tesla vehicles, but the company is, as of this writing, in the process of opening up access to at least 7,500 of its U.S. chargers (3,500 high-speed chargers and 4,000 L2 chargers) up to non-Tesla EVs. (In addition to the added revenue stream, this would qualify Tesla to receive some of the aforementioned federal funding.)

On July 26, 2023, a consortium of seven automakers – BMW, GM, Honda, Hyundai, Kia, Mercedes Benz Group, and Stellantis announced the formation of a consortium aiming to install at least 30,000 high-speed charging stations in North America starting in 2024.

The U.S. government has proposed federal funding for up to 80% of capital and installation costs in some situations, including $5 billion in subsidies to state governments, which will hopefully accelerate efforts. The catch is that the federal incentives require that the new stations “can be utilized by all EVs regardless of vehicle brand.”

This has required adjustments on the part of some companies, because there is no universal charging standard. The three most popular are:

- North American Charging Standard (NACS) – Created by Tesla, the specs for this standard are publicly available. Both Ford and GM recently announced their intention to start switching to this standard by 2025, mostly so customers will have instant access to thousands of charging stations owned and operated by Tesla. Rivian is also set to adopt the standard in its vehicles.

- Combined Charging System (CCS) – This standard was jointly introduced by Audi, BMW, Daimler, Ford, GM, Porsche, and Volkswagen. The EU requires that all EVs sold there, including Teslas, must be compatible with CCS stations.

- CHAdeMO – Created by Japanese carmakers in conjunction with the Tokyo Electric Power company, this standard is widely used in Japan, but less popular in other countries. (The CHAdeMO name derives from a Japanese offer of tea, meant to imply that the standard is fast enough to charge a vehicle in the time it takes to have some tea.)

Some other companies that are positioning themselves in an attempt to capitalize on this growing need for high-speed charging stations include:

ChargePoint (CHPT 11.84% )

Chargepoint manufactures both commercial and home-based charging-station hardware. It also owns and operates a network of public charging stations in North America and Europe, with around 240,000 locations in more than a dozen countries. It provides charging solutions to commercial fleets as well.

ADS-TEC Energy (ADSE -11.76% )

AD-TEC offers an intriguing high-speed charging alternative to DC-based L3 stations: battery-buffered charging stations. These offer similar charging speeds to an L3 station, but without the need for a DC connection. Instead, the company uses its lithium ion battery packs to supplement the charge delivered by an L2 hookup. These battery packs get recharged when nobody is using the station, particularly late at night when power-grid demands are lower and electricity tends to be less expensive.

Battery manufacturing

The transition to EVs will also require a dramatic expansion in the production of batteries. Right now, lithium-ion batteries are the preference for EV manufacturers. These typically include a cathode made of some combination of lithium, nickel, cobalt, and manganese; and anodes made of some combination of graphite and silicon, with electrolytes made of a lithium salt dissolved in either liquid or gel.

In early July 2023, the IEA found that in just the last five years (2017-2022), there was a drastic increase in demand for many of those raw materials. This includes a “tripling in overall demand for lithium, a 70% jump in demand for cobalt, and a 40% rise in demand for nickel.” Unsurprisingly, prices have soared as well: the price of lithium rose sixfold over the same period, the price of cobalt nearly doubled, and the price of nickel more than tripled.

Increased EV demand accounts for some of this higher demand, but so does the push for other types of green energy like solar and wind – forms that depend on batteries to store excess generated power to be used when the sun isn’t shining or the wind isn’t blowing.

It is worth mentioning that some of these materials are most abundant in countries that are either diplomatically precarious or morally problematic. For example, China is the source of much of the world’s lithium supply (and lithium refining facilities), while the Democratic Republic of the Congo controls 60% of the world’s cobalt deposits.

Companies that can develop and operate mines for these materials, especially in countries that are friendlier or less controversial if possible (and it often is not), should have little trouble finding customers in the years to come. Some prominent names include:

Albemarle Corp (ALB 3.49% )

Albemarle is one of the largest and most well-known integrated lithium producers in the world, extracting the metal through lithium salts extracted from sites in Chile, lithium brine in Nevada (the only lithium production site in the U.S.), and stakes in lithium mines in Australia. It is also a major lithium refiner, with operations in Nevada and Chile, and processing plants in North and South Carolina

Lithium Americas Corp (LAC -0.01% )

Although much smaller than Albemarle, Lithium Americas enjoys good trading-volume liquidity as of this writing, and GM recently agreed to take a $650 million equity stake in LAC to help secure the automaker’s supply of lithium.

Piedmont Lithium (PLL 3.33% )

Piedmont has a contract to supply Tesla with high-purity lithium. It produces lithium through its in Gaston County, North Carolina, and through its minority stake in Sayona Mining, which has a mine near Quebec, Canada. Piedmont is also developing production sites in Ghana and a lithium hydroxide processing facility in Tennessee.

Glencore (GLEN)

Glencore accounts for 16% of global output, most of which is produced as a byproduct of its copper-mining efforts in the DRC. The Swiss mining conglomerate is well known for its extensive suite of operations in various commodities: it produces coal, copper, gold , aluminum, zinc, and oil.

Jervois Global (JRVMF)

Jervois is one of the largest producers of refined cobalt outside of China. Among its cobalt-related holdings are the only cobalt mine in the U.S. (located in Idaho), a nickel-and-cobalt mine in New South Wales, Australia, and a major cobalt refinery in Finland. It is also a significant supplier of nickel, operating a nickel and cobalt refinery in São Paulo, Brazil.

Alternative battery technologies – potential gamechangers?

On July 4, 2023, Toyota (TM 1.19% ) announced that it had made a significant breakthrough that would allow for EVs powered by solid-state lithium ion batteries. The Japanese carmaker claimed that its solid state batteries would allow for a full recharge in just 10 minutes, enough power for a range of 745 miles or more, and it would introduce the technology into the market as soon as 2027.

Many viewed Toyota’s announcement, if true, as a “game changer.” Scientists had long known that solid-state batteries could dramatically increase range and improve charging times, and that solid-state batteries could deliver such benefits in a smaller, lighter, and safer form factor – all with a more environmentally friendly manufacturing process. Solid-state batteries are already in use in small devices such as pacemakers and active RFID tags.

But manufacturing batteries large enough to power an automobile had always been too complex and difficult to achieve at scale, subject to faster deterioration of capacity, and vulnerable to performance issues in colder temperatures. Toyota’s breakthrough – the details of which have not been disclosed – purportedly addresses these issues. Other companies have been searching for a solution as well, and one new company claims to also be close to a commercially viable solid-state battery for EVs:

QuantumScape (QS 3.82% )

A spinoff from a project at Stanford University, QuantumScape has been working with Volkswagen on the development of mass-producible solid-state EV batteries for more than a decade. It went public in 2020, and despite not having a viable product – or any revenues, QS has generated buzz for its progress reports on a smaller, durable, solid-state battery that could recharge from 10% to 80% capacity in less than 15 minutes and deliver up to 400 miles of range at full charge. As with Toyota, QS’s claims have not been independently verified, and it is unclear when QuantumScape might have a product ready for commercial production – if ever.

Another alternative to the current dependence on liquid lithium ion batteries are sodium-ion batteries. Sodium is chemically similar to lithium – readers who remember their high-school chemistry will note that sodium sits directly below lithium on the periodic table.

As with solid-state batteries, there are benefits and tradeoffs. Sodium is far more readily available – the primary source for pure sodium is soda ash, and 90% of the world’s known supply of the raw material. Sodium-ion batteries theoretically also have a longer useful life and superior low-temperature performance. Unfortunately, they are also less energy dense, which means significantly heavier and bulkier battery packs are required to deliver the same power.

Another issue has to do with the research into this technology – industry sources suggest that the Chinese are the only ones who have devoted significant effort to researching this potential alternative.

Nevertheless, some have suggested that even if sodium-ion batteries prove too bulky for use in EVs, they could still be used in other renewable energy projects and thus, ease the demand for lithium.

As usual, Signal From Noise should serve as a starting point for further research before making an investment, rather than as a source of stock recommendations. Although the names mentioned above each have the potential to benefit from the world’s likely transition to electric automobiles, this alone should not be the basis of a decision to invest.

We encourage you to explore our full Signal From Noise library, which includes interviews with respected investors and bestselling authors like Morgan Housel and Robert Hagstrom. You’ll also find recent deep dives on the path to automation and opportunities arising from the ever-increasing global water crisis.

Your feedback is welcome and appreciated. What do you want to see more of in this column? Let us know. We read everything our members send and make every effort to write back. Thank you.