Signal From Noise

Research

Signal From Noise

Research

Morgan Housel and his wife needed a house. It was June 2016, and they had agreed they wouldn’t make an emotional decision on one of life’s most significant commitments. This would be their first home, where they’d celebrate Christmas morning and welcome friends to backyard barbeques. Their son was about six months old. Being patient, they decided, would be critical to their search. No emotional home buying. No impulse moves.

After they saw a house on Zillow that looked nice, they drove up to the driveway to tour the property. “Wow, I love it,” his wife said. “We’re like, oh my God, it’s perfect,” Housel recalls. “We told each other, ‘We have to buy this house right now.’”

“I love this as an example of even when you think you’re an unemotional person and you go out of your way to say you’re not going to be emotional, some things are emotional,” Housel says. “You shouldn’t pretend housing or children, or money isn’t emotional. So much of investing isn’t a spreadsheet, it’s emotion.”

Housel, a partner at The Collaborative Fund and former columnist at The Motley Fool and The Wall Street Journal, published his international bestseller, The Psychology of Money, in 2020. The book is 19 short stories exploring how people think about money and how to make better sense of one of life’s most important topics. In two and a half years, it has sold over 3 million copies. Oaktree’s Howard Marks says Housel’s “observations often hit the daily double; they say things that haven’t been said before, and they make sense.” Author James Clear said, “Everyone should own a copy.”

Early this month, we spoke with Housel out of his Seattle-area home about the timeless lessons from his book, what he’s learned studying the best investors, and some of his favorite mental models to better orient yourself around markets. Spoiler: He has a new book coming out this fall. This special edition interview of Signal From Noise is edited lightly for clarity.

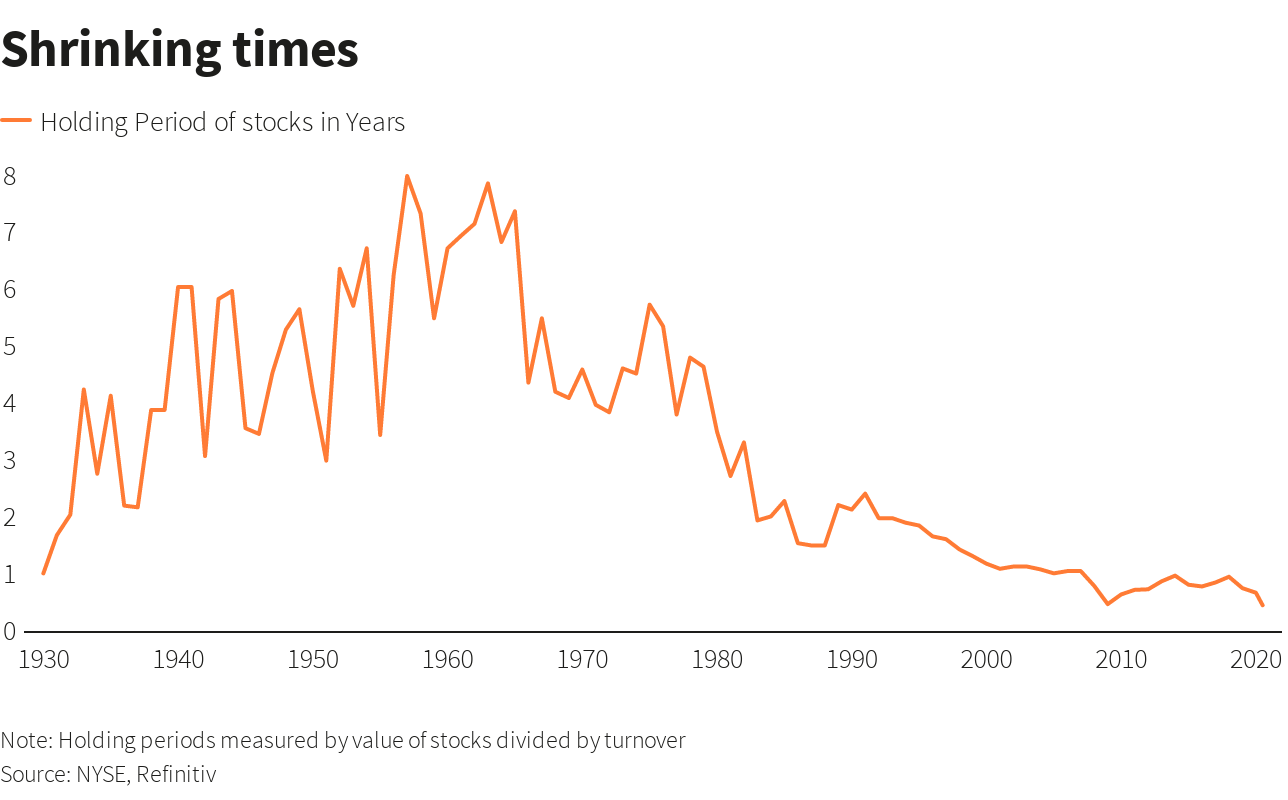

Let’s start with time horizons. The average holding period for U.S. stocks was about 10 months in 2022, down from more than five years in the mid-1970s. Why is it hard to be patient with our investments?

I think a big part of this is that so many people say they’re in for the long term, but the long term is just a series of short terms you must experience and endure. It’s like standing at the base of Mount Everest and saying, that’s where I’m going, to the top. That’s great, but now you must hike up the mountain daily, dealing with market volatility. Some investors do themselves a disservice when they say, “I’m in it for the long run. I don’t have to think about the short run.” No, you must think about the short run, you still have to experience it.

You’ve written about how it’s hard to do nothing, which is often the best move to make as a long-term investor. Why is that?

When markets are down 10%, it’s like, “What are you doing with your money?” It might be better to ask, “What are you not doing?” Simplify it. I wrote about this in my book: I think it’s hard to be inactive as an investor because, in almost every other endeavor in life, there’s a correlation between activity and results.

Physical fitness is the best example. If you want to be in great shape, work out every day. If you want to be a great runner, go out and run, act. If you want to learn physics, go read 100 books about it. But investing is different. Often, if you want to perform better, go do something different. Stop thinking about investing, stop trading all the time, and you’ll probably be better off. It’s so counterintuitive that there is no relationship between activity and results in investing.

Look at (Warren) Buffett and (Charlie) Munger. They read all day and only make a few calculated investments here and there. It’s fascinating.

Why does it feel, as Tom Lee has pointed out, that markets seem to get spooked easily nowadays, and investors are so short-term oriented?

Convenience plays a role. You could check your phone, check the news on a stock, then make a few clicks and move your money. Not long ago, you had to pick up the phone, call your broker, and you got his assistant. And the assistant would say, “Oh, he has an appointment now, he’ll call you back.” When he calls you back, he says, OK, it’s $200 to place a buy order. This is not long ago. That’s how it worked forever. And 40 years ago, it was not $200. It was more like

$1,000 to buy and sell a stock. That made investors think long and hard about making a trade.

There used to be a speed bump, and that was great. Now the convenience has made investors worse. There was much less emotional trading when you had to call your broker and pay him to make a trade. Now, it’s boom, boom, boom, done.

In some cases, especially in 2020 and 2021, it was like a casino.

Well, maybe not a casino, but it turned stocks into a drug. Stocks became an addictive drug. It’s very powerful and critical to be in tune with your emotions.

Let’s discuss dopamine’s role in investing. You recently wrote about how we don’t necessarily want the nice this or that, but rather we crave the feeling associated with acquiring new things. Was that a new insight, or was it always percolating in your head?

I got that idea the last year from interesting places. One was Will Smith from his biography.

He says becoming famous is the most amazing feeling in the world, being famous is a mixed bag, and losing fame is some of the worst pain you can ever experience. And I was like, wow, that’s it. It’s not about being famous, it’s becoming famous. It’s the same thing with money: It’s not being wealth. While that’s great, the real pleasure comes in gaining wealth.

There’s a Nas (rapper) quote I love, it’s like, “People don’t admire you when you have something, they admire you when you’re in pursuit of something.”

Those two insights explain dopamine. You don’t get dopamine from having something or a lot of wealth. You get dopamine when you gain something new. It’s why living in a mansion might feel great, but it’s probably not as great as buying a mansion.

A key idea in stoic philosophy is reducing our desires and expectations. Thousands of years ago, the stoics had to remind themselves to desire less, not to let their emotions manipulate them.

Absolutely. It can be a superpower. You might not get the 40% annual return all the time, but you can do well if you’re buying quality index funds or stocks and taking a decades-long approach. In investing, it’s ironic that if you’re accepting of lower returns, those people tend to be the people who become the wealthiest.

The right question to me, if you understand compounding, is from the exponent. It’s returns to the power of time. The exponent is time. That’s where all the power is. If you can earn average returns for an above-average period, that’s great. If you could earn 8% returns for 50 or 60 years, you’re an elite investor. But nobody wants that. Everyone’s like, how can I earn 15% right now?

I’ve always viewed it this way: Do nothing and you get 8% a year. Or, if you can jump over this pit of lava filled with crocodiles, with people shooting at you, you can get 8.5% per year. If you can have less focus on your returns and more focus on endurance, you might be better off.

The asterisk is that that only works for younger people. If you’re 75, you can’t say, oh, I’m investing for the next 50 years. But particularly for young people, your efforts should be on endurance.

You could rationalize that a 75-year-old can still invest for the long haul, with their heirs in mind. You can be 90 and invest for the next five decades seeking to build generational wealth.

For sure. Absolutely.

Given the volume of noise coming at people, a simplified approach stands out. Spend less than you make, save, and invest the rest in excellent places, right? (One such place is Tom Lee’s Granny Shots, which has beaten the S&P 500 by a mile over the last four years.)

It’s so simple that it’s almost stupid, and I think people don’t want to believe how simple it is. It’s also important to know that, if you or your spouse reach 75, the odds that one of you will reach 90 is pretty good. There are a lot of people in the 60s and 70s who think they don’t have 30 years ahead of them. No, you probably do. People are living longer, which helps compound money over more extended periods.

With a 30-year horizon, you don’t have to worry about perfectly timing a trade or getting the bottom. All that takes so much emotional bandwidth. It’s time you could spend with your family or doing something you love.

Some people genuinely enjoy the process of investing. That’s great. But most people don’t. They’d rather spend time with their spouse, hike, improve their health, read a book, take a nap, whatever it might be. We must recognize how lucky we are to live in an era where there are investment products that allow you to buy stocks with minimal fees and leave them alone for 50 years. That is such a gift.

I buy low-cost index funds with a 50-year horizon, but I don’t recommend others do that. I don’t judge people who invest differently from me. It’s just an amazing gift that you can buy and not do anything and have very good odds (not 100%) that in 50 years these will compound into a fortune.

You’ve talked about it with Buffett. If he had retired in his 60s, he probably wouldn’t be a household name. But he’s been investing for over 80 years, and that’s his superpower: time.

He has a great annual return, it’s 20% for decades, but he’s also been invested for many years. It’s not 10 years, it’s not 30 years, it’s 80 years. That doesn’t mean you have to do the same because everyone is different. We all have different goals, savings rates, and spending habits. It’s like music: Some people like rap, country, or rock. There’s no right or wrong. Different approaches can work.

You advocate having cash, even if the market is running hot. Buffett would agree that there are no called strikes in investing, so you can afford to sit and wait for the right pitch. Why do you believe holding a healthy amount of cash is so critical?

Two things. I graduated college in 2008 ahead of the Great Financial Crisis. People thought the world was melting down. I was very young and didn’t have a lot of cash, but it was this oh-shit moment where I was like, well, my job prospects are slim. I’ve got enough cash in the bank to make my rent for the next two months or something. The rest was in stocks. I had 100% of my net worth in stocks, which during the bull market, was great.

But it was in 2008 when I realized cash is the oxygen of independence. You need a lot of cash for financial independence. You don’t have to get caught up on the opportunity cost of cash losing to inflation or quality stocks. Every five or 10 years, there’s an emergency where you need cash. It’s healthy to have an amount of cash that feels a little bit excessive because if it feels a little excessive, that’s when you know you’re prepared for the risk you can’t envision. Because there are so many risks nobody can predict.

For years, people question, why would a CEO keep all that cash on the balance sheet? Then Covid-19 happened. And it was like, oh, that’s why.

How do you reduce noise in the investing world to think clearly, and not be distracted by news or stock price fluctuations?

How do I reduce noise? I don’t. I read financial news all day. I’m on Twitter all day. I read The Wall Street Journal every day. So, I don’t reduce noise. But what’s important is that the noise doesn’t cause me to act. I read the noise because I think markets are fascinating. I think the economy is fascinating. I don’t read the noise and say I need to sell this or buy that. Never, never, never.

It’s critical to pay attention to your media diet. If your media diet leads you to act, you might want to look harder at what you’re doing.

Why is FOMO, or the fear of missing out, pervasive in markets?

Not feeling FOMO is a key trait. If you can do that, you’re ahead of 90% of people. In 2020, people were doubling their money even if they had no idea what they’re doing. To just sort of sit on the sideline when stocks with no profits are flying, that’s hard.

It takes discipline not to act. Some people are more susceptible to FOMO than others. Some people are very concerned with an external benchmark. How do other people view them? They might be doing it for applause or attention. But people who aren’t susceptible to FOMO are usually more concerned with how they feel on the inside.

When and where do you come up with your best ideas for writing and investing?

I go on a lot of walks in the neighborhood. I read all day. If there’s a meeting on my calendar I don’t want to do, I’ll just cancel it.

Look at the U.S. President, he’s the most powerful man in the world, with the least control over his schedule. A lot of billionaires and CEOs fit that too. But there’s value in slowing down and having leisure time. That’s when big ideas happen.

As Fed Chairman Alan Greenspan said, his day was very scheduled with meetings. Once, he was asked how he got his ideas. He said every great idea came in the bathtub. Buffett gets his best investing ideas there too. For all these people whose days are very scheduled, as soon as they have a moment of unscheduled time, the brain starts clicking in the way that they wished it did during the scheduled time.

Morgan, an absolute pleasure. Thank you.

Thank you so much.

Your feedback is welcome and appreciated. What do you want to see more of in this column? Let us know. We read everything our members send and make every effort to write back.

Thank you. Access our full Signal From Noise library here.