“The close relationship between railroad expansion and the general development and prosperity of the country is nowhere brought more distinctly into relief than in connection with the construction of the Pacific railroads.” ~ John Moody

Union Pacific Railroad (UNP 0.68% ) rose sharply recently after it announced a new CEO – Jim Vena, who formerly served as UNP’s chief operating officer. The market apparently welcomed Vena’s ascendancy due to his reputation for improving efficiency, which will come in handy when he takes the helm on August 15, 2023. UNP, like the rest of the railroad industry, faces increasing challenges.

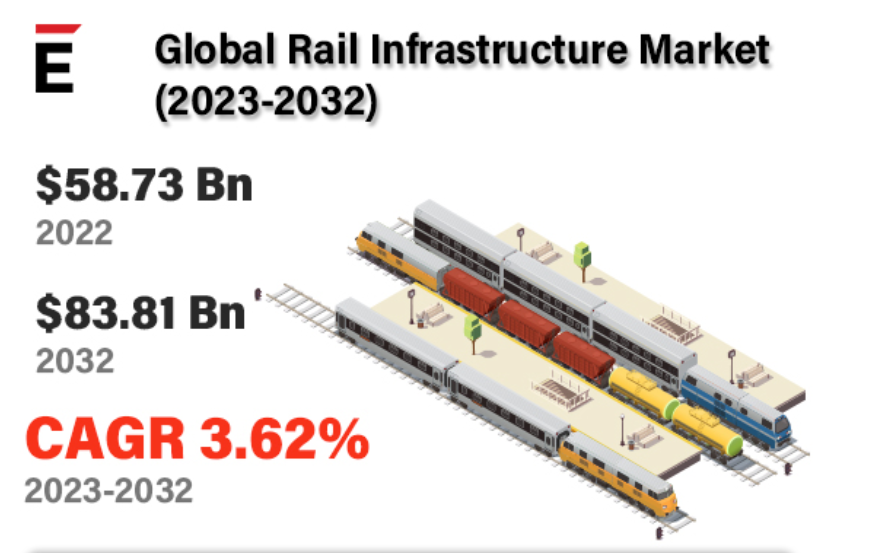

Yet in both the U.S. and on a global scale, public initiatives present potential longer-term opportunities for railroad operators, infrastructure companies, and manufacturers of rolling stock and associated products and services. An April 2023 report by Extrapolate Statistics valued the global rail infrastructure market at $58.7 billion and estimated that the market would grow to about $83.8 billion by 2032. Extrapolate also forecast that passenger and freight activity would double by 2050.

In Asia, much of this growth will likely be driven by increased urbanization, development, and trade. In India, for example, passenger traffic has almost tripled since 2000. Freight traffic has grown by 150% over the same period. And China is rapidly building freight and high-speed passenger railroads both domestically and abroad as part of its Belt and Road Initiative.

Economic factors are also a big reason for the interest in expanding rail capacity in the West. But environmental concerns play a role as well. On a per-passenger basis, trains are as much as 12 times more energy efficient than air travel. Along similar lines, the Federal Railroad Administration estimates that freight locomotives are two to seven times more fuel-efficient as trucks, as measured by gallons per ton-mile. And it goes beyond that: one diesel-powered locomotive can haul as much as 800 trucks, so replacing truck hauling with rail shipping whenever feasible also reduces emissions by improving traffic for other vehicles. (As a side benefit, this significantly reduces roadway wear-and-tear.)

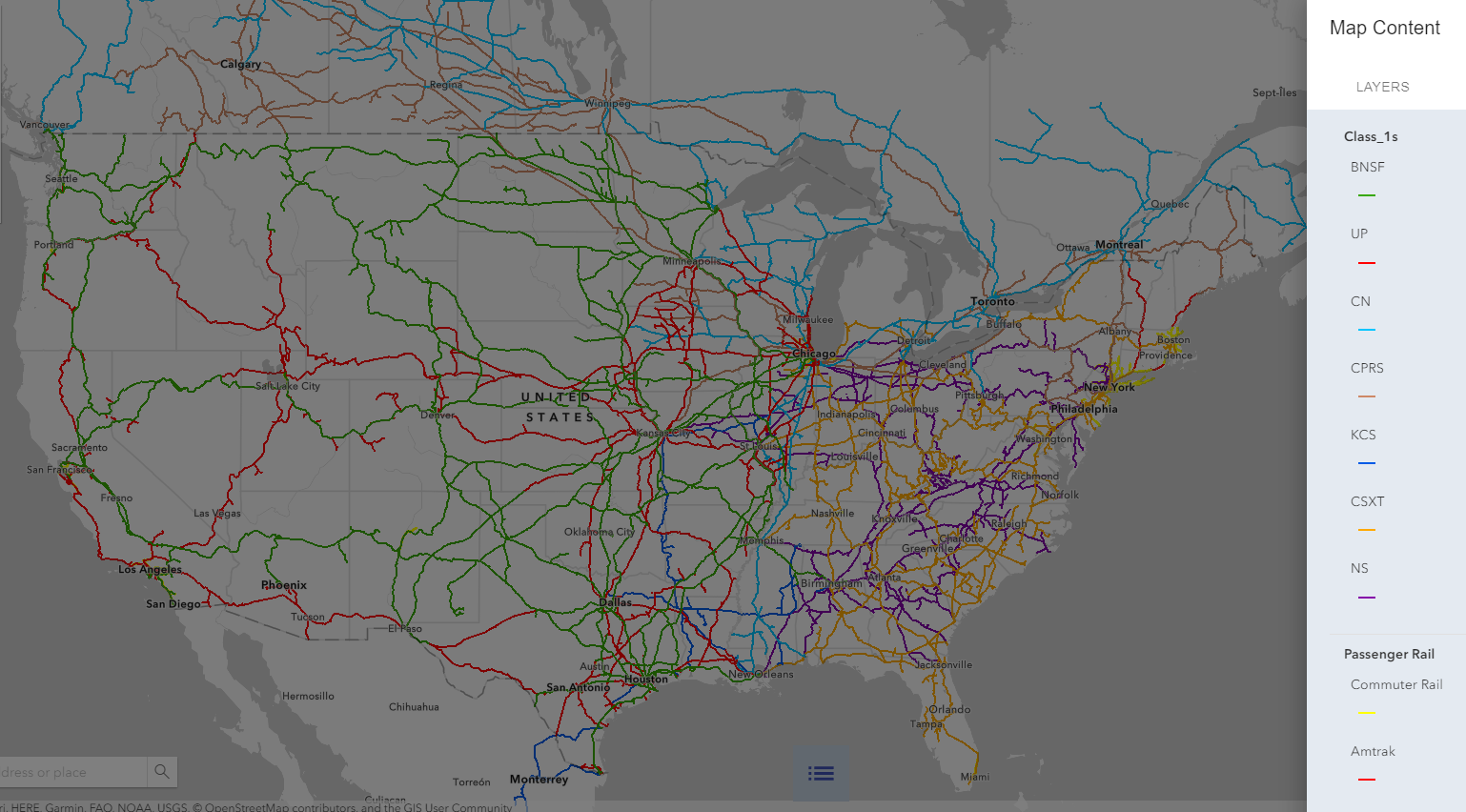

In the U.S. the railroad system is comprised of roughly 150,000 miles of rail lines in total. The majority of those are owned and operated by six large Class 1 freight railroad companies (as of this writing, defined as a rail company with annual operating revenues of at least $490 million.) Amtrak (which also counts as a Class 1 railroad company) runs U.S. intercity passenger rail service. It owns about 600 miles of track in the northeastern states, and operates on leased tracks owned by freight rail companies elsewhere. The rest of the system is made up of a number of small freight and passenger rail companies that operate in a very limited capacity. (The latter includes commuter rails that run between large cities and the surrounding suburbs, but it does not include urban public transit systems like subways.)

Both freight and passenger rail in the U.S. have declined in importance since their heydays in the last century. Amtrak’s passenger tally (22.9 million passengers in the 2022 fiscal year) is dwarfed by any of the major airlines – United Airlines, for example, had 58.8 million domestic passengers last year. And domestically, trucks have become increasingly more important for the transportation of freight and cargo.

Nevertheless, railroads remain essential to the U.S. economy – so important that in December 2022, when railroad unions were threatening to strike, some economists estimated that such an action could cost the U.S. economy as much as $2 billion a day, and cause the loss of hundreds of thousands of jobs. The American Trucking Associations ruled out any possibility of truckers taking up the slack, estimating that it would require 460,000 additional trucks and 80,000 additional drivers to make up for the suspension of freight-rail service. This is why, when it comes to railroads, both the President and Congress each have the authority to intervene in labor disputes and, under certain circumstances, block or end strikes.

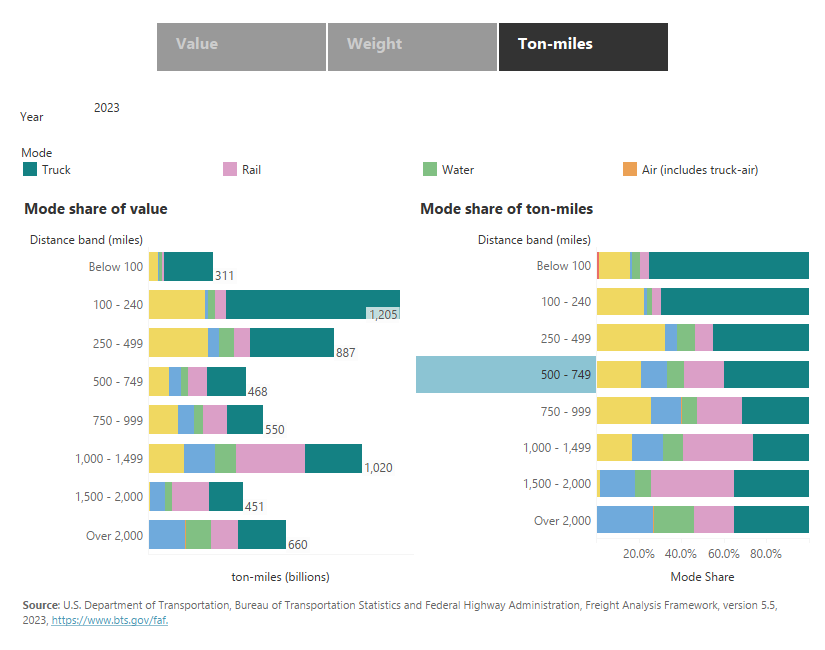

The U.S. freight rail system is the largest in the world. Measured by ton-miles, it handles 40% of long-distance freight shipments. The rail companies collectively transport about a third of the country’s grain production and play a major role in the shipment of coal, crude oil, construction materials, and paper products. And thanks to the widespread adoption of standardized shipping containers, railroads are expected to remain essential to an increasingly multimodal global freight system that relies on water transportation for international shipments, railroads for the middle of the journey, and trucks for transporting goods through the last segment to their final destinations.

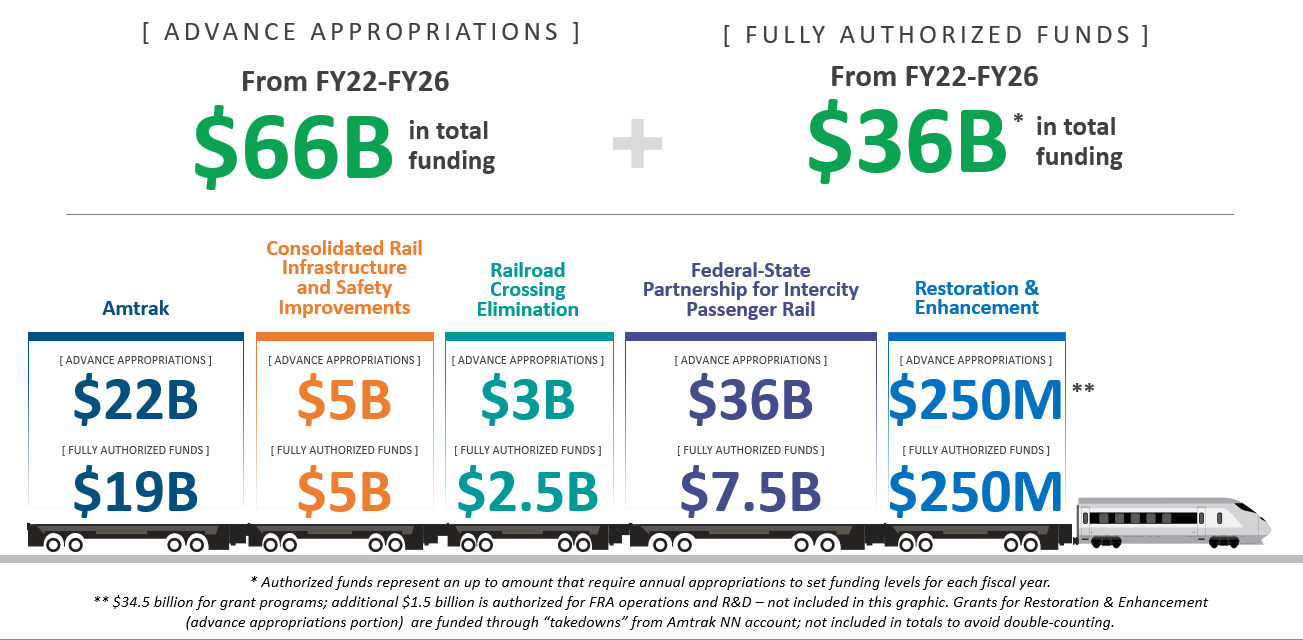

Their ongoing importance to both the domestic economy and global trade helps to explain why railroads were allocated a significant share of funds in President Biden’s Infrastructure Investment and Jobs Act (IIJA), which allocated $102 billion to fund construction of new passenger and freight rail infrastructure. This consists of $36 billion in authorized funds and $66 billion in appropriations.

The IIJA also seeks to encourage the development of U.S. high-speed passenger rail, which currently is limited to Amtrak’s Acela service in the Northeast. The Act would provide funding for smaller independent projects in varying stages of development, in California, Texas, Florida, the Pacific Northwest, and elsewhere. High-speed rail advocates claim that such projects will provide significant economic benefits, including increased productivity, reduced congestion, and job creation.

Meanwhile, in Europe, the EU has set a goal of doubling high-speed passenger rail capacity by 2030 and tripling it by 2050. Concurrently, officials also propose banning shorter flights between major European cities: 17 out of the 20 most popular intra-Europe air routes are less than 450 miles, and in such cases, high-speed rail is not just more fuel efficient, but faster for city center-to-city center travel. (For reference, Boston and Washington, DC are 394 miles apart by plane.)

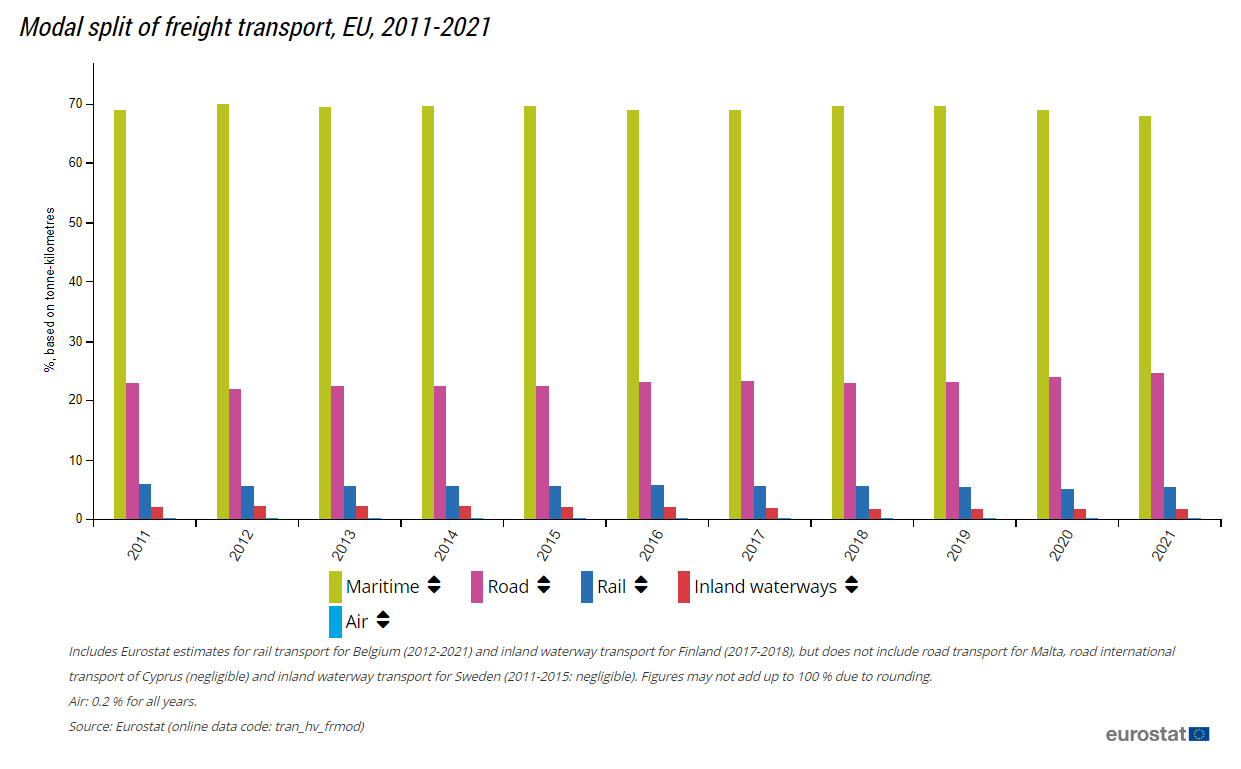

And while passenger rail is far more popular in Europe than it is in the U.S. (EU statistics show that the average European travels about 600 miles a year by rail, compared to 100 miles for the average American), the converse is true for freight rail. European officials have long declared their desire to increase the rail share of freight shipping, but the EU’s infamously labyrinthian bureaucratic procedures have helped to impede that on a transnational level. Recently, the EU disclosed its intention to streamline those processes so that freight rail systems between member states can be more easily connected. The objective is to double the share of freight shipped by rail (currently at around 15%) by 2030.

These initiatives and objectives present potential opportunities for railroads, infrastructure companies, and rolling-stock manufacturers. As previously mentioned, U.S. freight rail shipping consists of private companies operating on their own tracks. These companies benefit from pricing power, costly and difficult barriers to entry for new competitors, and an enduring business model.

Class 1 freight rail operators include:

- Union Pacific (UNP 0.68% ) – Union Pacific is one of two Class 1 companies that form the duopoly dominating rail shipping in the western United States – the other being BNSF (below). It is the second-largest railroad in the U.S.

- Burlington Northern Santa Fe (BRK.A) – Wholly owned by Berkshire Hathaway, BNSF is the largest freight railroad in the United States, with 32,500 miles of track in 28 states (and to a limited extent, in Canada). It is a major hauler of grain and coal, and its lines cover most of the western United States.

- Canadian National Railway (CNR 2.40% ) – The bulk of Canadian National’s routes span Canada from East to West, near the U.S. border. It also operates a north-south freight rail route that runs along the Mississippi River

- Canadian Pacific Kansas City Railway (CP 0.91% ) – CPKC is distinguished by its status as the only operator of a single-line railway that connects Canada, the United States, and Mexico. It operates on approximately 20,000 miles of rail

- Norfolk Southern Railway (NSC -0.25% ) – Headquartered in Atlanta, Norfolk Southern operates 19,420 miles of track. It operates as half of a de facto duopoly that controls freight rail shipping in the Eastern United States. NSC was the operator of a freight train that derailed in East Palestine, Ohio in February 2023, which was followed by at least three class-action lawsuits, widespread criticism, a $416 million charge, and a sharp decline in its stock price.

- CSX Transportation (CSX 0.37% ) – CSX is the other half of the eastern U.S. freight rail duopoly, operating on about 21,000 miles of track

However, U.S. freight operators also face significant challenges. The industry is heavily capital-intensive. Growth opportunities are limited. And revenues are highly sensitive to economic cycles.

Furthermore, railroad work is difficult and dangerous. In recent years that has made labor both costly, yet scarce, improving the bargaining power of labor unions. In addition, railroads are often entrusted with shipping hazardous cargoes that can amplify the liabilities associated with accidents. For these reasons, many railroads are investing in automation and AI technologies that can help them operate more safely and with less manpower. Some of the options include:

- Automatic Train Operation (ATO).This refers to systems that take over all or part of train operation, with the degree of automation classified from GoA0 (no automation, completely human operated) to GoA4 (complete automation of starting, stopping, doors, with no human action needed except in case of emergencies). Implementation of GoA4-level ATO has been limited to a few subway lines thus far (in cities including Paris, Rome, and Sydney for example.)

- Positive Train Control (PTC). PTC systems are designed to improve safety, helping to prevent accidents such as collisions, speed-related derailments, and unintended train movement into work zones or other inappropriate areas. PTC has already been implemented in much of the U.S. rail system.

- Move Block Signaling. Move block signaling enables greater track capacity without compromising signaling. Older fixed-block signaling works by segmenting tracks into static “blocks,” with sensors indicating when a static block is occupied by a train and preventing any other train from entering the block. Move Block Signaling defines each block as the space around a train (rather than relative to the track), monitoring the position and speed of each train in the system to ensure that no train enters into another train’s block.

- Intelligent Traffic Management. As the name suggests, intelligent traffic management helps manage train traffic on a rail network. This includes planning routes, setting timetables, and scheduling crew shifts.

- Automated Shunting. Shunting refers to the movement of trains between tracks or between a track and a railyard. It also includes hooking train cars to locomotives or to each other. This has traditionally been one of the most dangerous jobs in the industry, and although automated shunting technology is still in its infancy, it should improve worker safety and railroad capacity while reducing labor and energy costs.

The increase in railroad infrastructure investment also presents potential opportunities for manufacturers of rolling stock, a category that includes locomotives, freight cars, and passenger cars (carriages). In particular, manufacturers of rolling stock for high-speed rail should benefit.

There is considerable overlap between these two industries: many leading companies that design and produce automated rail systems are also involved in the design and production of rolling stock. Some of the most prominent include:

Alstom (AOMFF)

Alstom is a leading rollingstock manufacturer. The French company built the first for TGV, France’s high-speed rail service and one of the first in the world. The company recently acquired Canadian-German rolling stock manufacturer Bombardier Transportation, thus uniting two companies involved in Amtrak’s Acela project. Alstom also manufactures a range of automated rail solutions, including systems for automated train operation, move block signaling, and automated shunting.

Siemens Mobility (SIEGY)

Part of the German conglomerate Siemens AG, Siemens Mobility is a multinational company in its own right, with a full range of products and services for just about every aspect of the railroad industry. This includes high-speed locomotives, passenger and freight rolling stock, automation solutions, track and rolling-stock maintenance, and even rail-related cybersecurity, ticketing software, and analytics.

Wabtec (WAB -0.64% )

Wabtec, also known as Westinghouse Air Brake Technologies Corporation, has a product lineup that goes far beyond brakes. The company manufactures components for locomotives, freight cars, and passenger carriages. It recently introduced a completely battery powered freight locomotive. It is also a leading provider of automated rail solutions, including Positive Train Control, Move Block Signaling, and Automatic Shunting.

Hitachi (HTHIY)

Part of the Hitachi conglomerate, Hitachi Rail is perhaps best known as the builder of Japan’s famed Shinkansen bullet train. Hitachi’s high-speed rail technology has since been licensed by rail operators in other countries, including China, the United Kingdom, and Italy

The railroad industry and the businesses that serve it have reason to be optimistic in the face of certain tailwinds, but they are also subject to uncertainty and growth limitations. As usual, Signal From Noise should serve as a starting point for further research before making an investment, rather than as a source of stock recommendations. Although the names mentioned above each have the potential to benefit from increased government investment in railroad infrastructure around the world, this alone should not be the basis of a decision to invest.

We encourage you to explore our full Signal From Noise library, which includes deep dives on the path to automation and opportunities arising from the ever-increasing global water crisis. You’ll also find a recent discussion on the Magnificent Seven and the rise of Generation Z.

Your feedback is welcome and appreciated. What do you want to see more of in this column? Let us know. We read everything our members send and make every effort to write back. Thank you.