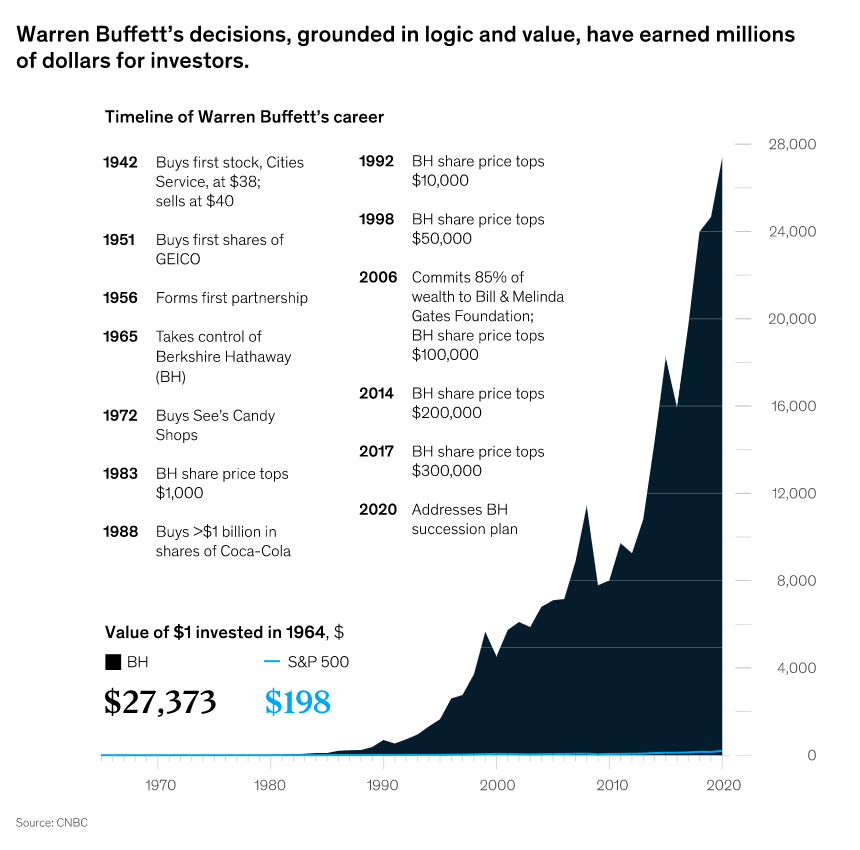

In mid-October 2008, with blood all over the streets, Warren Buffett penned a New York Times column: ‘Buy America. I am.’ Amid mass hysteria, the Oracle of Omaha made another contrarian move in a career defined by them. He predicted some of the U.S.’s most outstanding companies would set profit records in five, 10, and 20 years. It proved to be a dead-on forecast, as the March 2009 low marked the beginning of a long-standing bull market. A simple rule dictated his buying then, as it always has: Be fearful when others are greedy, and be greedy when others are fearful. Over the past 80 years, the mantra has helped make him the richest investor.

By age 30, Buffett had amassed a net worth of $1 million, or $9.3 million adjusted for inflation. He’s invested through wars, bubbles, panics, recessions, and political environments. He’s made nearly all of his wealth (roughly $113 billion) after his 65th birthday, a masterclass in the power of compound interest. In an era of constant notifications, price reminders, and trading apps, Buffett’s approach continues to stand out. His company, Berkshire Hathaway, has delivered a compounded annual gain of 19.8% since 1965.

“If you aren’t willing to own a stock for 10 years, don’t even think about owning it for 10 minutes,” Buffett has said.

On May 6, thousands of investors will flock to Omaha for Berkshire Hathaway’s Annual Shareholder Meeting to see Warren Buffett, 92, and his partner, Charlie Munger, 99, discuss markets, investing, and life. Ahead of the meeting, we spoke with bestselling author Robert Hagstrom, whose superb book, The Warren Buffett Way, has sold more than 1 million copies. It explores Buffett’s process, and how he became a billionaire and investment sage by looking at companies as businesses rather than prices on a stock screen. How to hold through turbulence? How to identify excellent businesses worth holding for a decade or more? Behaving rationally in the face of the ups and downs of the market has been central to Buffett’s success.

Here’s our interview with Hagstrom, the Chief Investment Officer of EquityCompass and Senior Portfolio Manager of the Global Leaders Portfolio. It’s edited lightly for clarity.

Warren has always been known as a stock guy, but he’s really a business buyer. How can we think about that?

Warren says, “I’m a better investor because I’m a business person, I’m a better business person because I’m an investor.” They work together. When you’re a business-driven investor, a lot of stuff falls away. It just doesn’t matter what someone says will happen with the economy. People ask for speculative comments or answers, but you can say, “I have no idea what the market’s going to do next week or month.” That’s not a good answer for many people. They’re unsettled with the idea that the future is unknowable.

We don’t have a perfect system, but democratic capitalism has endured 250-plus years of significant challenges. I’ve got a pretty optimistic long-term outlook. I just don’t know what’s going to happen week to week (neither does Buffett).

Once, Jeff Bezos asked Buffett: “Your investment thesis is so simple. You’re the second-richest guy in the world, and it’s so simple. Why doesn’t everyone just copy you?” Buffett’s reply? “Because nobody wants to get rich slow.” That’s one of Warren’s many admirable traits: He’s earned all this money without having an opinion about where markets are headed in a given year. He just holds great businesses.

As Charlie would say, it’s a recipe for mediocrity when entering and exiting positions. By the time you do expenses, trading costs, and taxes, you wonder why 90% of people can’t beat the S&P 500 index over 10 years.

I’ve never met anyone who disagrees with Buffett’s methodology. Few people have the mental attitude or mental capabilities to apply it when they’re distracted by all the short-term market noise. That’s why I wrote Warren Buffett: Inside the Ultimate Money Mind, not about his mechanics, but the mental side. The goal is to help people recognize there’s a mechanical part and a mental part, and the mental part is the hardest. People can learn discount models and their mechanics. It’s hard to put Buffett’s principles to practice when markets are falling sharply, and there’s a lot of noise.

Buffett and others have said that by reading annual reports and digging beyond the surface, you’ll be ahead of 90% of investors. He has said, “I insist on a lot of time being spent, almost every day, just to sit and think. That is very uncommon in American business. I read and think. So I do more reading and thinking, and make less impulse decisions than most people in business. I do it because I like this kind of life.” Is reading a big part of your process?

Let’s distinguish between being a business owner vs. a trader or speculator. If you’re into microeconomics, macroeconomics, or market analysis, you’re reading something different. But if you’re a business owner, you must read the financials of the companies you own and their competitors. We do that a lot.

You don’t have to read about markets. You don’t have to read about the economy because it’s all noise to being a business investor. I’ve been through a couple of recessions, and I’ve been through a lot of geopolitics and COVID. I stay updated on the daily news, but I don’t spend a lot of time on the economy. I don’t spend a lot of time on markets. I don’t spend a lot of time on geopolitics.

That sounds like the opposite of what many of us do in the modern news cycle.

You’re focusing on what Warren says is really the only thing you can somewhat control. It’s just an entirely different game. You have to figure out what game you want to play. The reason I gravitated to the Buffet game was that I was a lousy trader. I’m not wired in that way. There are rare people who are good at that, but they’re rare because trading is a very hard business. As a trader, you have to know when to buy to get ahead of the market, and when to sell because you think it’ll go down, and it’s just really hard.

I’ve got my model, and I’m trying to figure out businesses, not tickers. I’m trying to determine who has a competitive advantage and how long it will last. That’s about all I have to do.

Buffett and Charlie (Munger) read all day.

It’s enjoyable. After you really get a lot of reading done over the years, you realize so much stuff is noise, it’s not adding value, so you can skim over a lot. A somewhat underrated trait of Buffet and investors like that is cutting through the noise and deciphering what is an actual signal. We’re not taught that in school. You only have a certain number of hours per day, so you can ask: Is this serviceable to me or can I discard it? There are only so many quality businesses worth holding for long periods.

People start with good intentions of wanting to be investors and wanting to buy good companies, but they acquire bad habits and begin speculative behavior. The art of speculation then filters into their investment approach. That’s the problem.

Warren, luckily, found Ben Graham, who gave him an investment model, a mental model to think about things, before modern portfolio theory. He didn’t have to unlearn bad habits. And then the secret sauce was that he was buying businesses; he was investing in both the stock market and he was buying companies. Few ever did that in the 1950s and 1960s. It’s the difference between slugging percentage in baseball and hitting for base hits; frequency vs. magnitude. Warren’s slugging percentage would be pretty high.

Another baseball analogy he uses is that there are no “called strikes” in investing. You can afford to be patient and miss a quality stock opportunity because there’s always another chance.

Exactly. He waited and waited before buying Apple at an extreme discount in 2016. I bought it in 2014, and it’s been a monster. I think it was the only time I ever bought something before Warren. It will be the only time that happens.

But you know, I can’t tell you how many smart analysts had “sell” ratings on Apple, maybe half a million times over the last eight years. I’ve just held it. All you had to do is understand the business, let it compound, and you’d make a ton of money. If you’re looking at energy stocks because someone said they’re in vogue, or you’re looking at high-flying tech stocks because they’re doing well, that’s a totally different world than what I do, what Warren does. It’s a harder way to make money.

Warren also says: “The difference between successful people and really successful people is that really successful people say no to almost everything.”

Basically, he knows what his perfect pitch is, and he says he waits until the market gives him the perfect pitch with the perfect company in his strike zone, instead of swinging high and outside or far inside. He just knows the one swing he’s really good at.

I’ve heard you say you hold stocks for a while, and you stay out of the way of really extraordinary companies, like Apple, and Amazon; no need to be too cute and try to pick bottoms and tops. What is your thought process there?

We don’t do a lot of buying and selling. I try to take advantage of stocks when they get a little ahead of themselves, I’ll sell some of them and put them in things that are lagging. For example, we had a stock up 41% in two months, so we pulled a little bit off that. We’re constantly optimizing our portfolio.

What are your thoughts on cash? Investors can earn more on their cash now, and Buffett is a big fan of holding plenty of cash.

Warren feels like he has people’s savings and this goes back to the Buffett Partnership when he had life savings from doctors and business people in Omaha. He was so, so stressed about the idea of losing money for them. His first rule for investing is not to lose money.

That has probably prevented him from buying things like Google and Amazon, which he said he missed. He didn’t know if they were going to make it over the long run, and he just couldn’t stomach the idea of having a permanent capital loss. Our portfolio is fully invested, but the advisors we subcontract make individual asset allocation decisions based on their clients’ situations.

It wasn’t an overall market prediction, but last fall, at the bottom, you said areas in growth (Amazon, Apple, Microsoft) were mispriced. You were spot on, as technology has made a strong move since. Tech is up about 20% since. What did you see at the time?

I only make those calls when the odds are in your favor so much that if you’re wrong, you won’t be wrong for long. To back up to that, we had five years of growth in one year during the pandemic. The numbers were parabolic, and tech stocks took off as the interest rates cut to zero. I didn’t say one word about our portfolio, that you had to buy it. We were up 30% or so. Then I said dividend stocks are probably the most mispriced part of the market. They were down 20%, and 30% in 2020. So in late 2020, I said to look for high-quality dividend stocks, and they offered nice returns for a while, into this year.

But by late last year, it was clear investors were indiscriminately selling everything growth. Not just venture-capital growth-like companies that should have stayed private, but Google, Amazon, Microsoft, and Nvidia were all ridiculously cheap. The relative outperformance of value vs. growth was the second highest it had been since 2000. So, I did bang the table and say this is the cheapest I’ve ever seen growth in over 20 years. I said I don’t know when it’s going to reprice, but it’s the most mispriced part of the market. And sure enough, what happened on Jan. 1? Growth has led the way since.

What are you seeing now?

Inflation has probably peaked, it’s coming down hard. Long-term interest rates peaked. The dollar peaked. Those are all headwinds that aren’t there anymore. As we enter a period of slower economic growth, growth outperforms value. But let’s see what happens.

Buffett talks about turning off the stock market, paying little attention to price movement. How do you interpret that?

He has basically said, “Over my career, I’ve had to manage money with six Democratic presidents and six Republican presidents. I’m still buying businesses. I don’t worry about the economy. I manage a portfolio.”

When you buy beautiful ocean property in Florida or a country club on Long Island, you’re not looking at the price all the time. It’s the Buffett way. How do you avoid being distracted by constant prices associated with the market?

That’s a good analogy. I don’t have CNBC on in the office. Warren used to have CNBC on, but then somebody said he muted it, and then he put it far away in the corner. He glances over at it in case there’s a mention of one of his companies.

I just had breakfast with some friends in the private equity business and told them, “You guys have got this so easy. The best part of your business is you don’t have to look at a price every day.” For equity investors, you’ve got constant reminders of the price of stocks and the value of your portfolio. It can play with your emotions. So, basically, you want to run your portfolio like a private equity investor, right? You can think about it as owning private businesses that don’t have prices attached to them all the time.

In your book, you frame the idea of being a “focus investor” so well. Warren told you that, right? He said, “Robert, we’re just focus investors.” He has a lot of concentration, which comes from conviction. Nearly half of Berkshire is Apple, for instance.

It’s a great approach if you can pull it off. The caveat is you have to really know what you’re buying and be a good stock picker. Just really know your businesses. That’s a critical point for people who want to concentrate and reap those benefits.

One thing you wrote years ago: Sometimes Buffett will get cast as a perma-bull, but he’s more bullish on America long-term, right? Is that a fair characterization?

Warren’s bullishness is on America. He’s not always bullish on the stock market.

There were times in 1999 he was telling people the market is way overvalued. He’d made it clear when things were expensive to him. There are also times when he said this looks as easy as I’ve ever seen it, and that’s a bullish statement.

He’s a deep believer in the winning hand of America. That’s not just patriotism; it’s from decades of experience, right? He learned from his father Howard Homan Buffett, who was a congressman, a great man, who told Warren about how terrific the U.S. is in terms of opportunity. His first investment was at 11 years old, in the summer of 1942, when he bought three shares of Cities Service preferred stock the same day The New York Times’s lead article was that the war in the Pacific wasn’t going well. Warren was like, “We’re going to win this war. I have no doubt in my mind.”

Then look at all the decades since. There was always something to worry about, a time when you could have said, “Oh my God, this is the turning point, the good returns are over.” There was the Korean War, the Cuban Missile Crisis, riots, presidential assassinations, double-digit inflation, and so on, and through it all, experience has been his teacher.

No matter how bad those environments were, they didn’t stay bad, they improved, and we continue to heal ourselves. It’s not just patriotism, it’s not just faith, although faith is built upon experience, it’s the facts. The facts are, you know, democratic capitalism heals itself pretty well, not perfectly. Much of this comes from his father’s influence because he was a great believer in the U.S. He’s the one who taught him about character and how it takes a lifetime to build a reputation and 20 seconds to lose it.

The timing of his life is also fascinating: He grows up on the heels of the Great Depression, then we enter World War II during his formative years. He had so many reasons not to trust in America or to be fearful, yet he was the opposite.

When managing the public partnership in the early 1960s, he had the town’s savings, reputation, and trust. People in Omaha were going, “Should we build bomb shelters and get underground?” Cuba was going to launch missiles, they thought. But Warren said no, that they’d be fine. Just keep moving. It was pretty scary. He knew we’d get through that period, just as always. You can get through a lot over time – war, pandemics, and so on. Warren knows that no matter how dire the present is, the future will improve.

Your feedback is welcome and appreciated. What do you want to see more of in this column? Let us know. We read everything our members send and make every effort to write back.

Thank you. Access our full Signal From Noise library here.