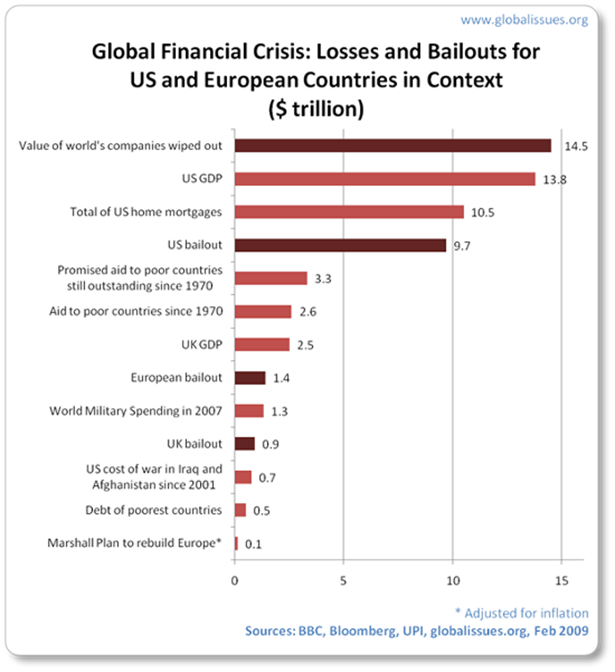

For much of human history, lending has been a highly regulated business. The Depression and the associated bank runs led to the creation of FDIC insurance and other guard rails for the banking system that consumers embraced. In some ways, the lending business has always been subject to the same risks, and effective due diligence has always been a key component of success. Innovation in lending was always somewhat curtailed, in the West, at least, by significant regulatory oversight. Another great wave of regulation came after the Great Financial Crisis in 2008.

This watershed event also accompanied an influx of innovators who preferred to reform the financial system with innovation rather than by government mandate. The VC community embraced a new wave of companies dedicated to empowering consumers, increasing efficiency, and expanding access to credit and financial services. Still, as 2022 unfolded, valuations plummeted far more than the broader market. We want to dive into the newer area of FinTech and determine which public companies are the best to invest in.

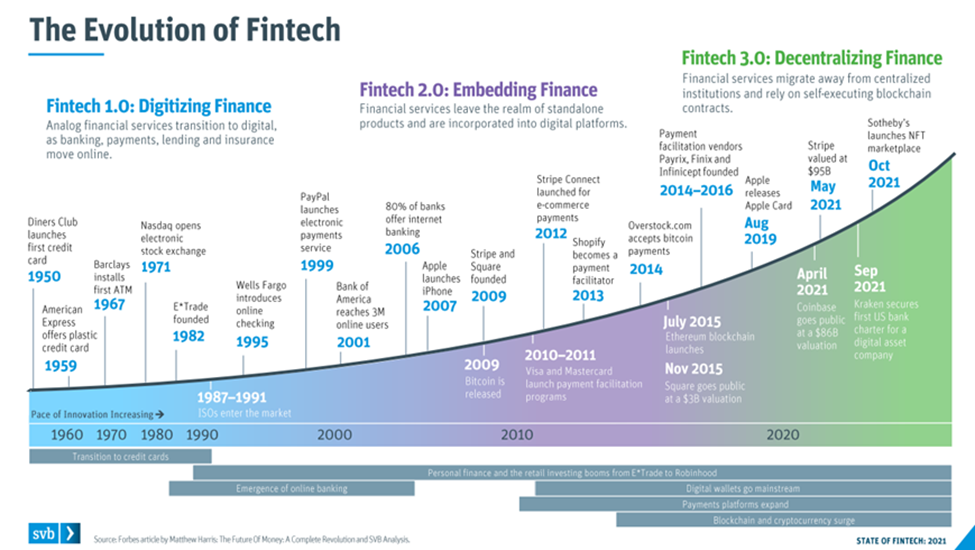

FinTech has become a broad umbrella term describing companies at the intersection of the ongoing digital revolution and finance. The burgeoning area has become a venture capital term as money flowed into a cornucopia of different companies, not just in the United States but worldwide. The firms promised to revolutionize the financial experience and rectify many of the perceived abuses of the banking system that were particularly acute in the public consciousness during and after the Global Financial Crisis. There are definitely inefficiencies and rent-seeking in both the banking and credit card industries, so there is a use-case, but overall obstacles and incumbents catching up has made growth projections seem untenable for many leading publicly traded FinTech firms done during the frothy 2021 markets.

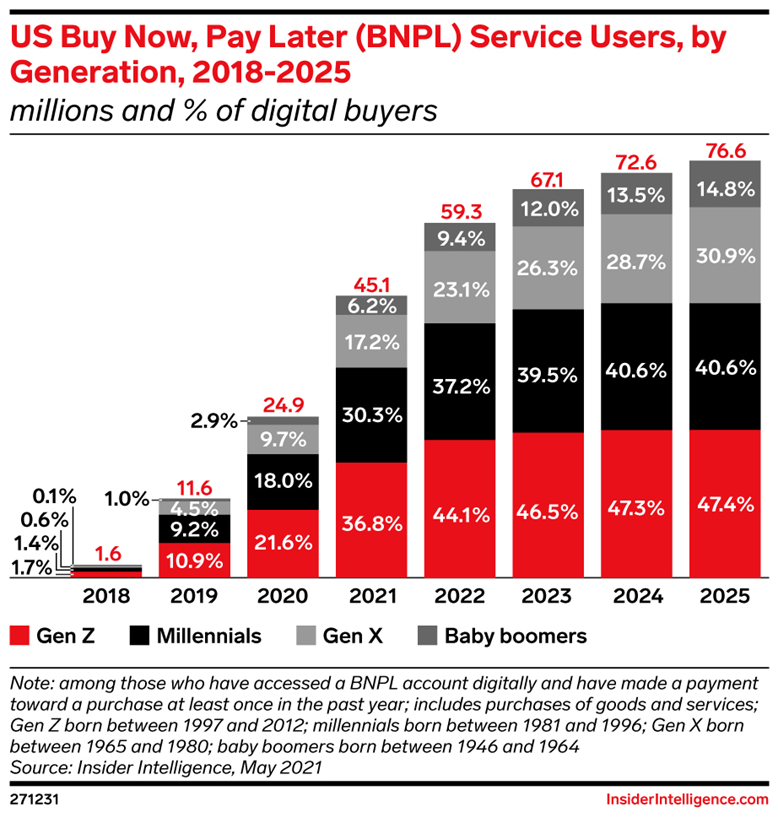

While early promises of rectifying and disrupting the financial system may have been enticing (and perhaps too well funded by VCs) after this event, the track record of many of these companies has fallen short of the initial grand ambitions. FinTech has become fiercely competitive and customer acquisition costs on the scale needed to revolutionize the financial system are high and likely only going to increase over time. There are several different areas of FinTech: Digital Lending, Payments, Challenger Banks, Insurtech, Wealth Tech, and Capital Markets Tech. There are also differing business models, as well as newer trends like Buy Now Pay Later (BNPL) that flourished in the pandemic but have since retreated.

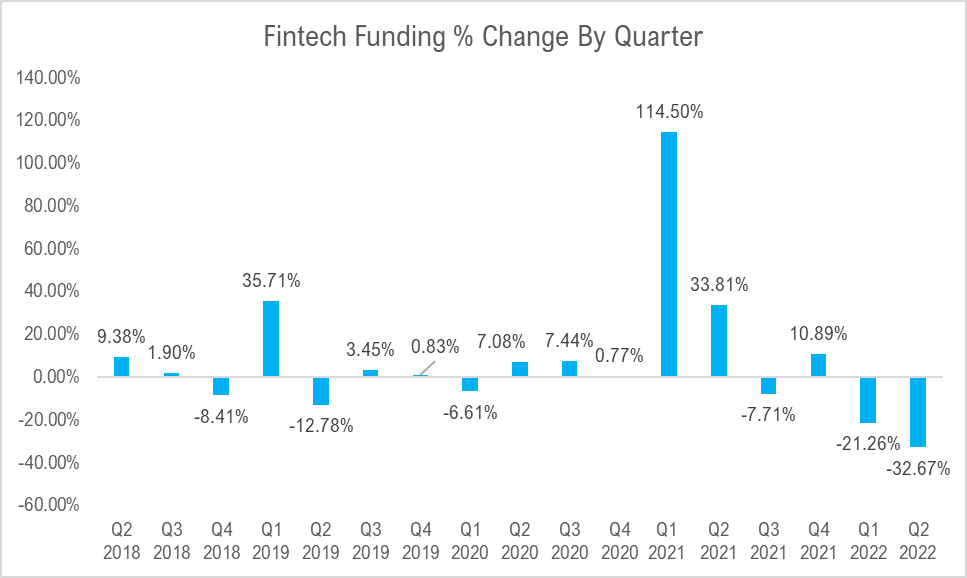

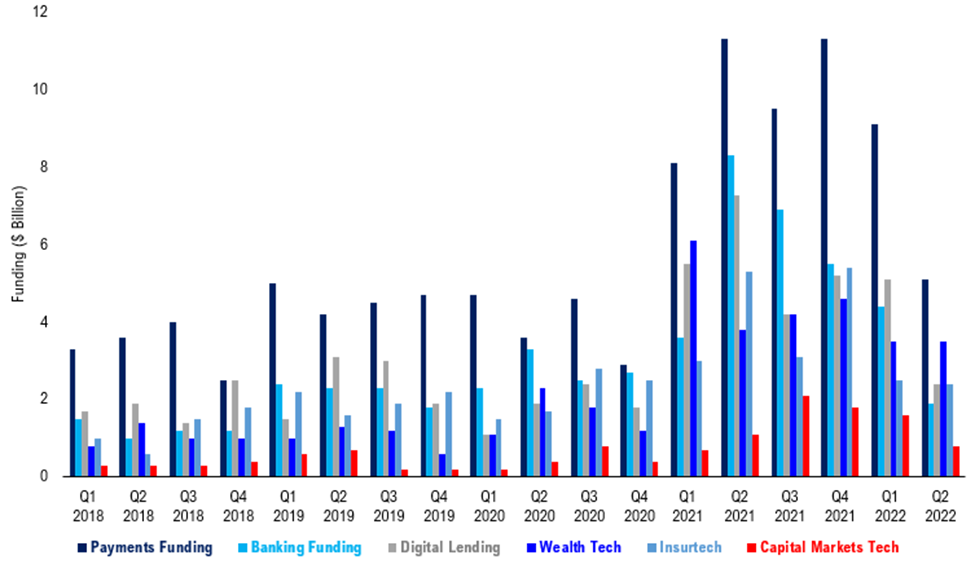

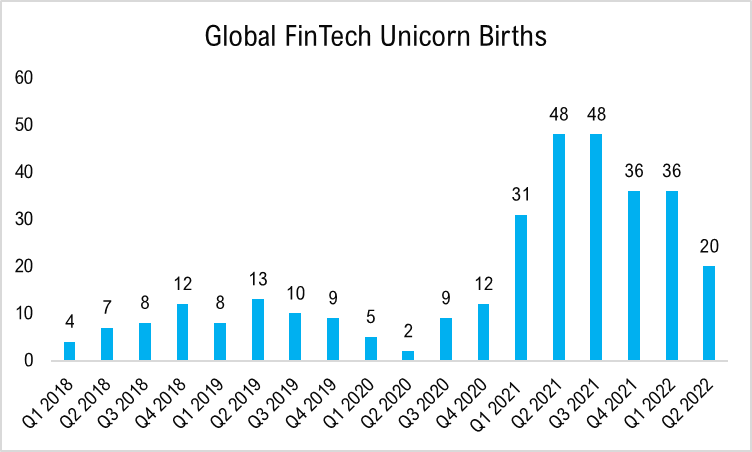

Venture funding has gone to levels not seen in some cases since before the pandemic. All segments contracted except for Wealth Tech. Unicorn births have gone down, and many companies appear to have kicked IPOs down the road, given the adverse environment for valuation. FinTech comprises many technological solutions, but sometimes regulatory solutions are just as important, particularly in the US.

We want to break down some of the core segments of FinTech below. We consider cryptocurrency to be its own area from a venture perspective that could mandate its own article: Nonetheless, crypto and the blockchain are a crucial component of the FinTech puzzle even though we don’t specifically address the segment below.

Payments

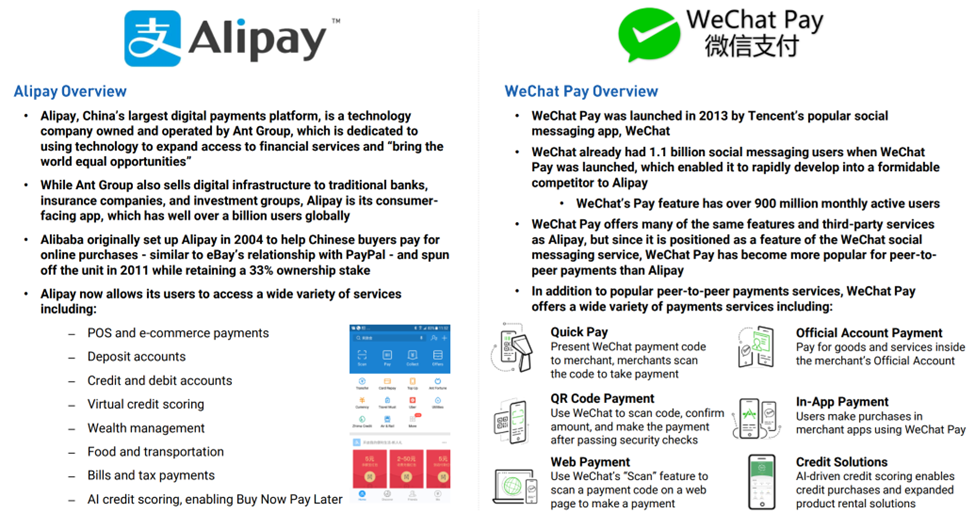

Payments are focused on transferring money either between businesses, from businesses to consumers, or person to person. Banks and Credit Card companies divvy up interchange fees on a per-swipe basis for merchants using their credit or debit cards between each other. Sometimes FinTechs will partner with a bank and split fees. The largest FinTechs on earth usually started their networks by providing accessible and relatively frictionless payments. Square, Paypal, Alipay, and We Chat Pay are all platforms that built extensive functionality on top of their original payments products. Cryptocurrency and removing the need for a trusted third party – which the technology enables – may threaten current payment structures.

Digital Lending

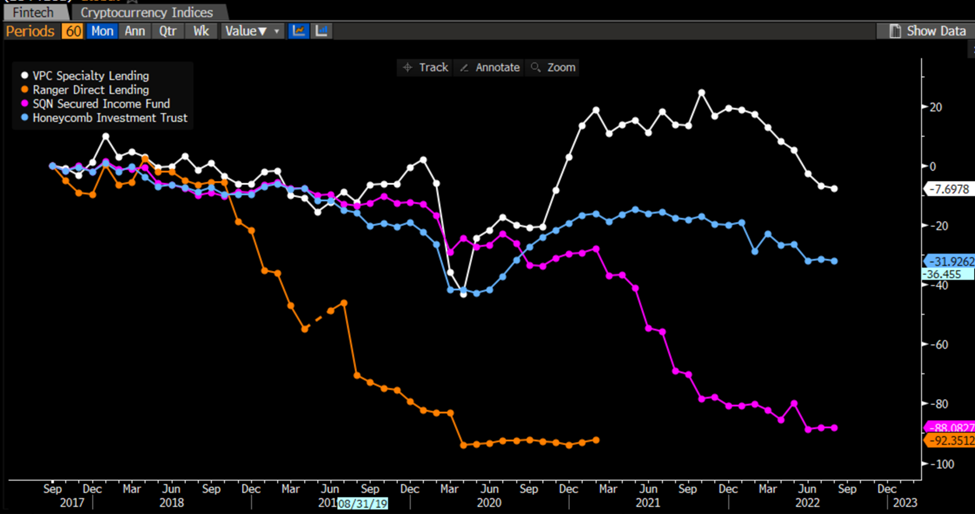

Banks are still dominant in lending. They have the distinct advantage of being able to fund loans from deposits. In countries where deposits are less regulated, FinTechs have been able to penetrate this area better. FinTechs often depend on ABS trust funding for their loans which significantly narrows their spread compared to what banks can get. As you can see below, these funds have performed dismally, and their underperformance started well below the 2022 multiple compression in the equities using them as a funding source.

Some of their funding is variable, so they are more exposed to interest rates. Rising rates won’t necessarily expand their net interest margins. The most recent trend in digital lending was the rise of BNPL (Buy Now, Pay Later). The growth in this product type was rapid during the pandemic when consumers spent an anomalously high proportion of their wallets on goods versus services. Valuations for many BNPL players, such as Affirm, have come down 70% to 90% since the peaks in late 2021.

Insurtech

The insurance industry might even make the banking industry look modern. Insurance giants may often be stuck in their ways, but even more importantly, they might be losing the edge in data. Data was the lifeblood of the insurance business long before the digital age. The plethora of new data sources, some even available in real time, revolutionize how actuaries price risk. New data can lead to more effective risk models, leading to lower consumer premiums. The implications across multiple sectors could be significant. As the tumultuous first half of 2022 has unfolded, losses have mounted for some new underwriting models. On the other hand, auto insurance may be revolutionized by the safety data that semiconductor-rich vehicles provide. Real-time data and automation are key drivers of innovation in Insurtech.

Banking/Challenger Banks

Rather than compete directly with banks, some proactive FinTechs have instead become banks. It was challenging to get a banking charter after the financial crisis, as prudential regulators would have preferred new capital to flow to undercapitalized institutions they supervised rather than new entities at the time, but this has since changed. Many so-called “Challenger Banks” have gotten their charters and even opened physical branches. The banking industry consolidated into a couple of dozen banks with the lion’s share of total banking assets and thousands of smaller banks that split up the rest. The smaller community banks rely on relationships, local connections, and a strong level of trust but often do not have the funds to be technologically dynamic. Many challenger banks aim to fill this void by imparting the precious community bank brand and experience while having cutting-edge technology and products.

Wealthtech/Capital Markets Tech

Wealthtech is the only area of FinTech where venture investment didn’t contract in 2022. This involves the support of the wealth management industry and players that have reimagined how consumers interact with a brokerage. Robinhood (HOOD 0.60% ) would be a prime example of a household name from this space. Zero-commission trades have fundamentally disrupted what came before but have also challenged business models and changed incentives. Capital markets technology is changing the way capital is sought and offered. Cloud technology, artificial intelligence, mobile computing, the internet of things, and crypto/blockchain are all changing the possibilities of how capital is raised. While there are promising opportunities in this space, this segment of FinTech has received the lowest amount of investment from the venture community over the previous years.

Incumbents Taking Advantage of Recent Weakness, Inherent Advantages

Let’s not give all the limelight to the new entrants, startups, and disruptors. Given the entrenched nature of existing players, they often dominate their industries through oligopoly. Visa and Mastercard are a great example, they have been among the most profitable companies in the S&P 500 for decades because of the competitive advantages conveyed to them as a result of their powerful duopoly. The fact that the credit card duopoly hurt consumers is a raison d’etre for many FinTech players, especially BNPL and online lenders. The fact that Visa and Mastercard are one of the most entrenched duopolies is also a reason why they’re incredibly difficult to disrupt.

Sometimes new entrants simply introduce new technologies and processes that legacy operators can effectively take from them through acquisition or other means and use more effectively through their established networks of trusting customers. With their sprawling networks of loyal customers who trust and regularly use them, the incumbents have proved more entrenched than they might have seemed back in 2008.

A vast regulatory overhaul in the wake of the financial devastation caused by the crisis helped to prevent the kind of abuses that led to the public admonishment of the banking sector. The banks also revarnished their reputation partially by being incredibly helpful to customers and the government in the dog days of the pandemic. These institutions are better capitalized and more highly regulated than at any time in recent history. Default rates on different types of consumer credit have never again returned to the extreme levels reached in the wake of the mortgage crisis. So, credit standards have tightened, but many digital lenders compete with banks for affluent customers that banks can usually serve more profitably.

The banking industry used to dominate financial services completely. While it has given up some ground to bright and shiny FinTech entrants, it still possesses many advantages over them. Many FinTechs, for example, cannot fund loans through accepting deposits but must be beholden to asset-backed securities trusts that significantly raise their funding costs. So, despite the flowery language and lofty goals often describing FinTech ambitions, we still think many incumbents retain inherent advantages in key areas like lending, which will be difficult for new entrants to overcome without massive investments. The customer acquisition cost just appears too high for the new guys and many of their investments made in the hyper growth driven by pandemic anomaly are likely to be ill-fated in our estimation.

Many of the newer FinTech entrants tried to make such investments to fuel growth, but subsequent developments and a reinvigorated incumbent competition makes the 2021 P/E ratios at the height of market exuberance unlikely to return anytime soon for many FinTech companies. Still, some were made during an incredibly anomalous time where growth in things like Buy Now, Pay Later occurred at levels that likely won’t be eclipsed anytime soon. Klarna, a BNPL darling considered one of Europe’s best startups, recently had an 85% write-down on valuation in their recent funding round.

It’s a Bird; It’s a Plane, It’s a Super App!

Whereas in most areas of Technology, the Chinese tend to copy innovations and try to refit them to their domestic market, the opposite is occurring in FinTech. AliPay and WeChat Pay created financial super apps that are often the primary financial destination for Chinese consumers to accomplish all their financial needs. Even ancillary services like ride sharing are done through these one-stop shops.

Key players, and even a large retailer you might not expect, are trying to follow the lead of these prodigious financial super apps and become one-stop shops for US consumers as their Chinese counterparts did. We think this is largely a dubious strategy and this lofty aspiration runs into several major obstacles that we see in the US market. The US market and other developed economies in Europe have a very different competitive and regulatory environment than China did in the period over the rise of their two financial super apps.

The two Chinese FinTech giants were able to grow in very different circumstances than the crowded field of US contenders are now facing. Firstly, the super app itself is essentially a technological product of inferior mobile phones used in China during the period of critical development. Chinese phones simply couldn’t support many apps, so these providers let third-party “mini programs” add functionality. These were added at less than half the cost of developing a separate app. The rapid consolidation was also mainly because China primarily used cash and didn’t have a comparable card network to what we have in the West. This was really the fuel for the mass adoption of super apps. Most FinTech firms with a lot of active users acquire them through payments functions, and this is much harder to do effectively in the US. The firm that came closest to a similar path was PayPal but given their recent troubles we consider them a ‘show me’ story.

So, there’s more competition and a much more developed financial system in the West. There is also a lot more regulation. While the unregulated Chinese market allowed these prodigious apps to spread their tentacles throughout the economy with little friction, this would not be the case in the United States. In China, banks weren’t really competing with FinTechs. In America, the banks are putting up stiff competition to FinTechs, as are the major card providers. For example, BNPL features are now available on many major credit cards.

Another consideration is that a vast user base is one of the most important components to build a successful super app. Owing to the obstacles just mentioned (regulation, competition, maturity of the financial system), US companies cannot proceed down the same path the Chinese giants blazed. Instead, incumbents or new entrants that already have large user bases that they can convert to new products with low acquisition cost seem to have a distinct advantage over new entrants that have to take time and invest significant resources to grow their active users to competitive levels. Also, many Americans, especially millennials, don’t appear interested in a super app and are comfortable having multiple financial relationships. Because of this, we have selected a mix of incumbents and newer FinTech firms for our favorite stocks in the area. Financial Technology itself is often being used effectively by incumbents to acquire and retain customers more effectively than many of the new kids on the block.

Lemonade (LMND -5.74% )

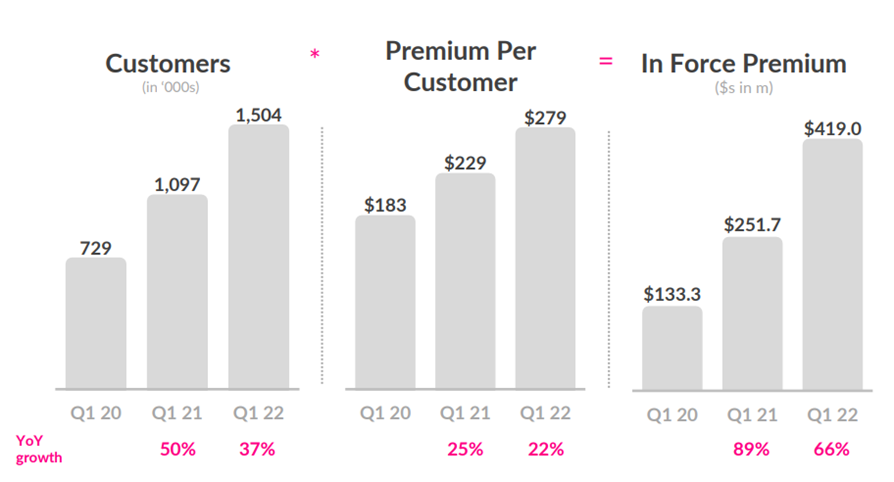

Lemonade is an Insurtech name that provides technologically enabled insurance solutions. Its underwriting is holding up solidly and it has made some strategic acquisitions to shore up its position recently. The firm offers insurance products in Europe and the United States. The company operates a variety of insurance projects covering accidents, personal liability, landlord insurance, car and life insurance.

The company has generated strong second quarter growth recently and beat on the top and bottom lines. In a disruptive area like FinTech leadership, experience is always key, and we think the company’s leaders have the appropriate insurance experience to properly understand the industry. The company has plenty of runway and is well off the post-IPO highs where valuation was stretched. The company’s app is user friendly, and they can execute insurance transactions faster than incumbents.

Lemonade still has valuation risk despite a steep decline if growth projections don’t prove sustainable. However, the company has both been growing at a healthy pace and has been growing value per customer. The stodgy insurance names that it is trying to disrupt might be able to adopt its technology. It obviously doesn’t do as well in a Fed tightening cycle and incumbent competitors have a lot more earnings and often pay high dividends. The consumer experience is very solid, and we expect that to continue to fuel cost-effective customer acquisition.

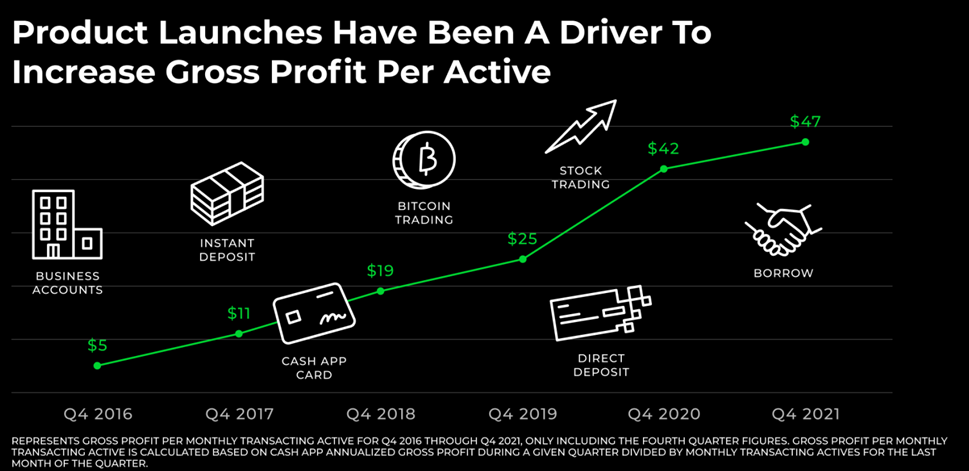

Block (SQ)

Block was originally known as Square when Jack Dorsey founded the firm. It’s a great example of how a successful company can build a thriving ecosystem from one original strength. This firm originally sold a hardware POS solution that was highly desirable for small businesses and individual merchants – think of the little white Square reader for contactless payments. It then built an analytics platform on top of that and other hardware to support its growing business.

The company also offers various software products, and its Cash App is a leader in the growing person-to-person payments segment. You can also store money on Cash App. It offers a developer platform and software development kits to facilitate more functionality in its growing ecosystem. The stock remains attractive from a valuation perspective after its precipitous fall in the first half of 2022. The company has also added crypto functionality and is very active in trying to make blockchain more mainstream for payments. Given the real economy footprint and potential of the Cash App ecosystem, we think this is a good long-term buy.

Square is subject to risks as it invests to add large bundles of products. If consumers respond negatively to the new suite of tools, this could be a major problem for the firm. Since Cash App is primarily driven by payments it is definitely sensitive to economic activity. The large banks have set up Zelle, which while it is not a standalone entity, still has proved to be a source of competition that could temper Cash App’s fast growth rates. Square seems to be pursuing the super app, and we have already discussed the pitfalls of this approach.

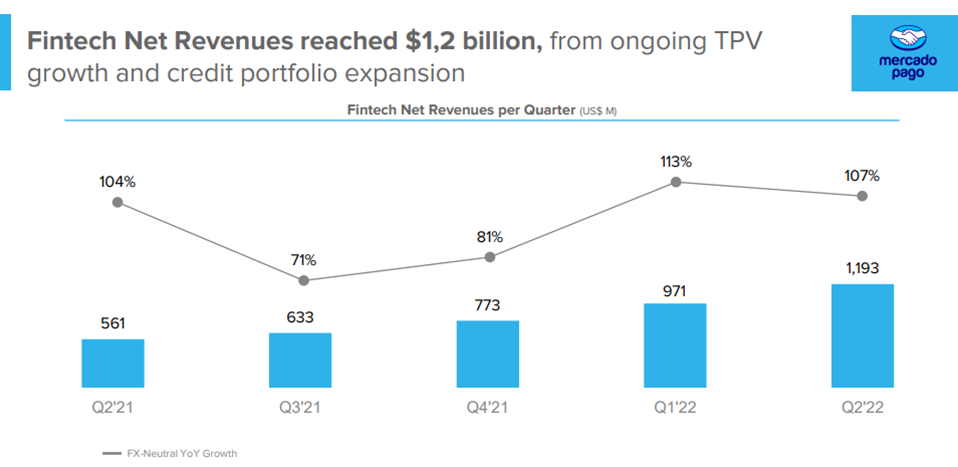

Mercado Libre (MELI -0.62% )

We mentioned that there are a lot of economic and regulatory hurdles that might prevent American companies from attaining the critical mass that super app proponents find necessary for the realization of their vision. However, these impediments are not as pronounced in Latin America. This company has become an ecommerce giant across Latin America. It has been referred to as the “Amazon of Latin America.” The platform facilitates transactions both on and off of its marketplace and the payments segment is reminiscent of PayPal’s early days. While discussions of which company in the United States can fulfill the super app role, Mercado Libre is executing to fill this role in the Latin American market and already has made significant headway in terms of users and transaction volumes. The company is diversifying its revenue streams and even provides an advertiser platform. In our estimation, Mercado Libre is following the lead of Alipay and WeChat Pay for the Latin American market more effectively than any American company.

There is a great deal of political risk in Latin America. The banking system there is vulnerable, but can also sometimes enjoy robust protections from the state. The company could face competition from large technology companies that have robust international expansion plans as well which could eat into growth projections as competition increases in its primary markets.

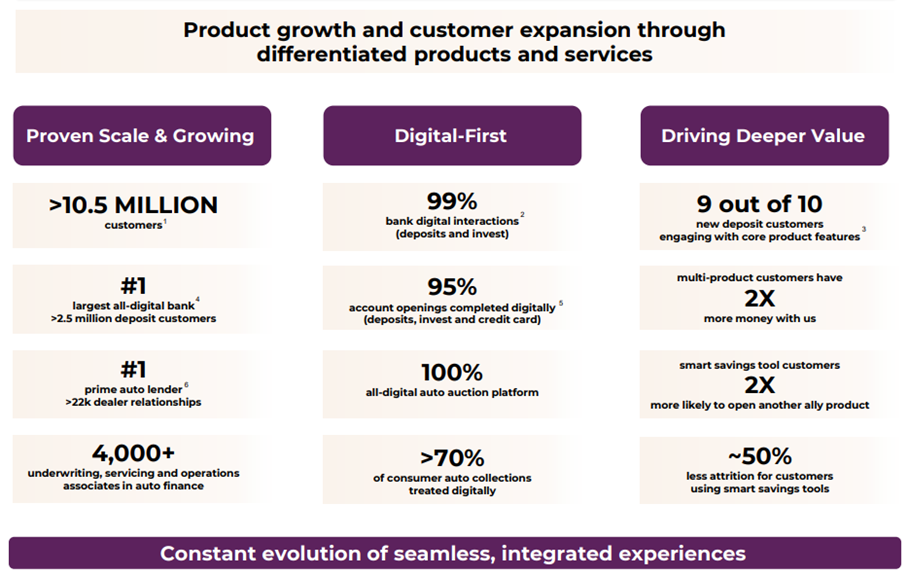

Ally Financial (ALLY -0.48% )

As we mentioned, it’s very hard for lenders funding loans through debt to effectively compete with banks that fund loans with deposits. Banks funding with deposits generally realize greater net interest margins than through other funding methods. Ally was formerly the lending arm of General Motors that provided credit to consumers purchasing vehicles. So it has a long and storied history in auto loans in particular that comes with deep expertise. After the financial crisis, what was known as GMAC Bank was transformed into Ally Bank with a technology-forward and pro-consumer bent. The firm has since been spreading its tentacles into various areas of FinTech.

It acquired TradeKing Group in 2018 and built Ally Invest, which is a brokerage and wealth management platform. Wealth management platforms generally increase daily active users because customers check them frequently. Ally also has launched its Clearlane Service, which is effectively a marketplace that connects lenders and borrowers. There are other established incumbents looking to make a name in FinTech, such as Walmart and Goldman Sachs, but we think Ally’s expertise and continued efforts to bolster the breadth of its product offerings with first-rate technology set it apart.

The company has a heavier exposure to subprime loans than many peers. This is a double-edged sword. Returns should be higher during good times, all else being equal. However, if there is a recession, Ally’s loan portfolio will be more economically sensitive than banks and FinTechs that focus on affluent consumers. Warren Buffett just took a large position in this stock as well, which is always a nice endorsement.

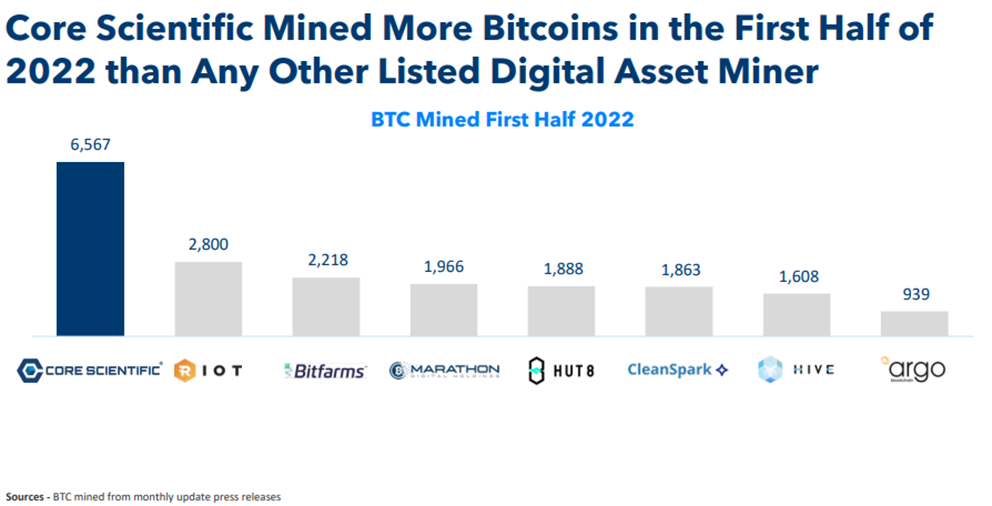

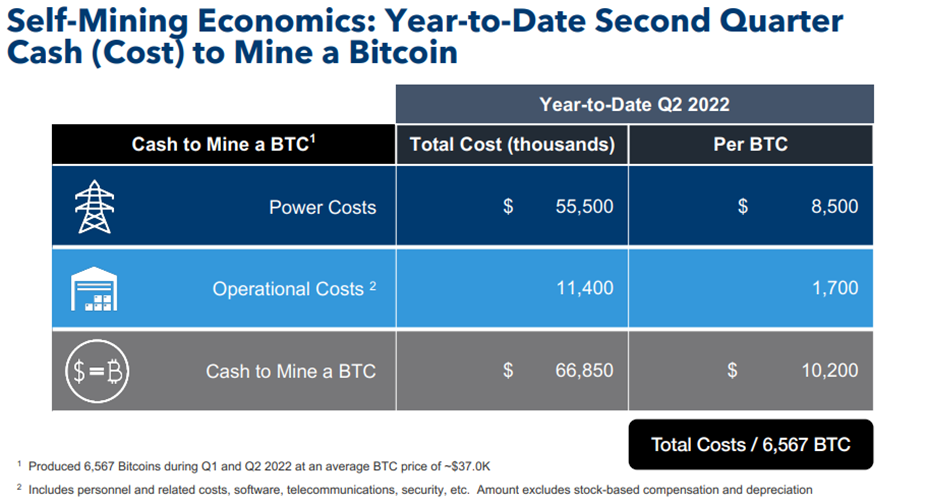

Core Scientific (CORZ 4.14% )

Well, that was a short crypto winter. Crypto miners are quite volatile and often misunderstood. Some are asset-light, such as (MARA 6.40% ). However, we’re convinced that the asset-heavy approach of Core Scientific is a superior business model long-term. Generally, our team feels that a growth scare is more likely than a major recession and we believe that bitcoin will recover from current levels. CORZ 4.14% has massive physical assets that it uses for cryptocurrency mining. It also hosts folks who want to mine using its hardware. The firm also develops blockchain-based platforms and apps, and has particular expertise in managing the complicated computing infrastructure needed to economically mine Bitcoin.

When Bitcoin has a strong year, as it did in 2021 the upside can be quite enticing; revenue grew ten-fold that year. Be aware though, the price of this stock is highly correlated to Bitcoin. These names are akin to a leveraged play on Bitcoin. Also, if the price of Bitcoin drops below the mining break-even rate these names can start hemorrhaging cash, as was seen during the latest crypto sell-off. The stock dropped as low as $1.41 compared to a 52-week high of nearly $15. This is a high-risk, high-reward name that’s also a leader in Bitcoin mining technology.

The company has considerable risks as miner. Many undercapitalized firms have been struggling and like a commodity producer, the fortunes of these firms are tied to the price of what they mine. Any weakness in Bitcoin below the company’s break-even point can cause dire financial consequences. However, CORZ has a lower breakeven rate than many competitors and building their prowess for hosting seems to have been a prescient move.