Key Takeaways

- Alblemarle (ALB 3.14% ) is the dominant player in lithium mining and extraction and has some of the most valuable and economic lithium reserves in the world.

- The company also has leading conversion facilities and intellectual property to help give it a competitive advantage against the limited amount of other lithium miners.

- The company is pretty well diversified across three segments. Lithium, Catalysts and Bromine specialties. The chief catalyst would be the rising demand and favorable supply picture for lithium because of the rise of EV, but the bromine and catalysts have respectable strategies.

- The company has a clear strategy to maximize productivity, grow profitably by anticipating future demand and to reduce capital intensity for higher CAPEX returns.

- This company should benefit from long-term changes to the economy from electric vehicles. It has a diverse and profitable portfolio of mining assets that put it ahead of its peers and make it a key picks and shovels play to the rise of EV, literally.

One great way to pick a stock is to find a consolidated specialty industry where there are only a handful of operators, then to find the best one amongst that group in terms of competitive advantage. There are a lot of ways to pick stocks but finding companies with a durable competitive advantage and doing your homework to identify it is one way that can pay off handsomely. However, remember that durable competitive advantage is not something you trade on, it is something you want to own.

When we polled some of the members of the public to ask Our Head of Research, Tom Lee, some questions one of the major ones we received was the following: what are some of the biggest trends that will affect markets and the economy over the next decade? Mr. Lee answered that electric vehicles and the expansion of the commercial space sector were two of the most promising.

There are only four competitors to Albemarle and none of them have proven as adept at extracting the stuff, or have as much of it in as high-quality of sites. Don’t feel like looking at EV blueprints or talking about whether a truck was rolled or actually drove down a hill? We’ve got a good way to take advantage in a more “picks and shovels” way, literally.

Albemarle is undoubtedly the best in its small class. It has the best resource portfolio, it is more vertically integrated in process technology and can pivot to changing demand cheaper and better than competitors. Very importantly it has key rules for CAPEX that ensure they give shareholders some breathing room compared to WACC, which is not necessarily the case with most competition.

It has a global footprint and it also is a leader in sustainability and balance sheet health relative to peers. When you throw in a crack management team with expertise to boot and a demonstrated track record of being superb stewards of shareholder capital, then you hit our little column’s sweet spot. We love a management team that has proven its meddle over multiple cycles.

A Materials Play With Staying Power

We want to stress that this is playing off of a long trend and is not a trade. Our technical analysis department doesn’t see the strongest setup for this stock compared to some of the lists they have recently come out with, so please keep this in mind. This is a long hold because it is benefitting from a major trend that will progress at a speed we cannot possibly anticipate today.

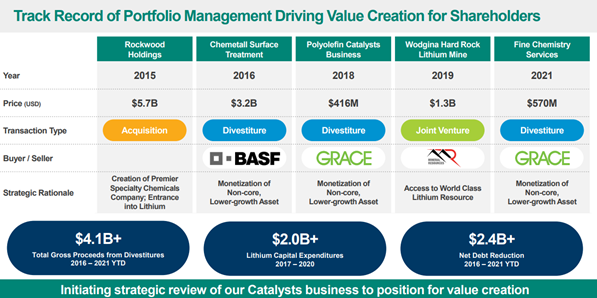

This column generally tries to highlight companies we feel have an endurable competitive advantage compared to peers. This is definitely the case for Albemarle. They are the most integrated of anyone else mining lithium and the other resources that this company does. Importantly, in resource extraction there are a lot of different metrics to measure by, and Albemarle has a sterling portfolio most ways you can look at it. Over the next five years revenue is projected to double, and this could be low.

This company’s portfolio seems more economically viable and lower risk than the assets of many competitors. Firstly, let’s take a look under the hood of this company because while Lithium may be the main reason investors are attracted to this name, it is not currently responsible for the majority of revenue. It likely will be in the future given current trends though.

The Lithium Supply Chain Need To Change With Demand And Albemarle Leads The Race

Firstly, we want to explain the Albemarle currently only generates about 40% of net sales from Lithium. The two other segments of Bromine Specialties and Chemical Catalysts comprise 35% and 25% respectively. The other two segments have significant growth opportunities, which we will elaborate on after we introduce the uniquely predictable opportunity in Lithium.

Secondly, we want to elaborate on another reason why you don’t want to trade this one. Lithium is a an incredibly valuable commodity but there are also tons of costs and steps from getting it out of the ground into a usable form for end-products, particularly the exciting ones. So, price of the commodity not only varies by region, but the way Albemarle monetizes it is usually through longer contracts.

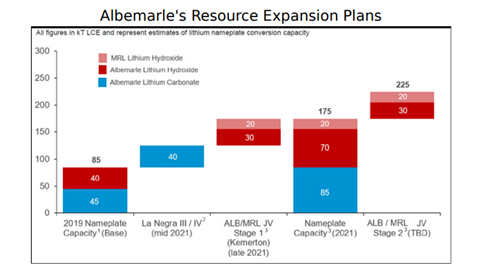

As the contract cycles go further into a future stressed by demand outpacing supply, the margin expansion doesn’t happen over night but over the life of contract resets, which may vary. One advantage the company also has it’s ability to offer greater security of supply for customers. This company is slowly specializing and shifting its capacity to get more access to the highest growth elements of Lithium demand, but this is a multi-year process for sure.

Renewable energy and electric cars are bigger than the Beatles right now, and you can benefit from these trends without idiosyncratic risk of project-specific plays when you get this company that is way farther up the supply chain for the crucial and scarce element that these two trends run on.

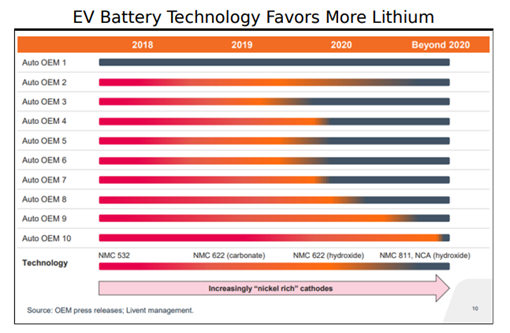

People who make money by digging holes in the ground have a special tenacity that is hard to teach. When they have a major competitive advantage and advantage in scale, they are even tougher in our opinion. Lithium Carbonate is the easier kind to produce but its high stability makes it hard to work with for desired end-applications.

The nature of demand has changed radically as the batteries needed require the much more difficult lithium-hydroxide which is needed for batteries and other energy storage functions. Importantly, the company is adding more capacity to produce the essential lithium-hydroxide which will continue to pay dividends over the years. This stock also has been increasing dividends for years, but the rate isn’t too consequential. Nonetheless, better than not having one.

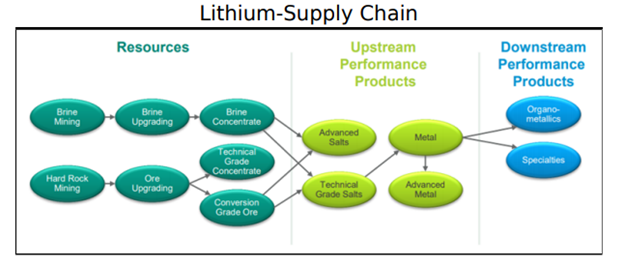

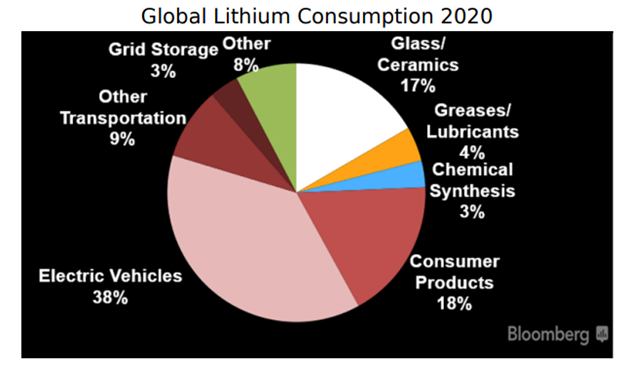

In order to get to lithium end products there are a lot of steps, but there are also a lot of end products besides just car batteries. Subsurface “bring” is recovered and converted to ore deposits which then must be synthesized into Lithium carbonate, which is the building block for all other lithium derivatives. The end-markets are very diverse and include everything from ceramics and glass to aluminum, greases and lubricants. It is of course used in pharmaceuticals as well.

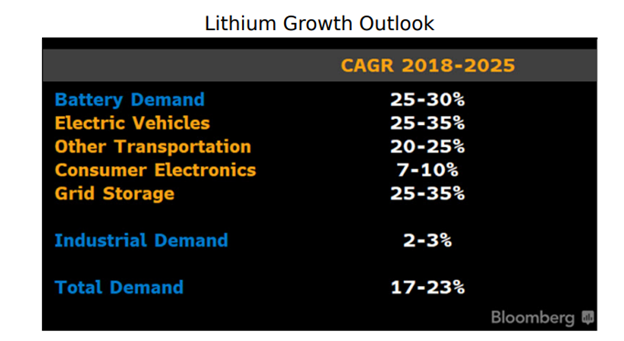

There are many end-uses for lithium, but of course, what had really made Albemarle soar lately is the fact that there is significant pressures on demand from the rising production, prevalence and need for electric vehicles. Even with current demands, the transportation applications using lithium already account for 45% of the demand for 2020.

The Red Headed Step-Children Segments Are Promising As Well

Diversification is a strength here and the company is progressing along many stated goals.

Certainly the narrative around this company has focused on lithium, but the other segments are no slouches either and this give the company options, flexibility and survivability over the long-term particularly when coupled with its exemplary capital discipline strategy.

The Bromine segment has diverse end uses as well, but is concentrated in fire safety solutions. It is also ahead of targets and helping to accelerate growth. California has whole swaths of residential sprawls that are becoming uninsurable. Can you think of anything those might be useful for the in the future we are all entering together?

However, bromine segment also has end markets in the telecom, electronics, automotive, energy and big ag and big pharma. We suspect that the uses could grow and proliferate an unknown, potentially far higher than current consensus path. This is why being the industry leader in scale and available capacity is a major benefit. It has the ability to serve and retain customers better across its diverse segments. Growth in the need for polymers and needs associated with 5G could prove bountiful.

Risks And Where We Could Be Wrong

A materials company with as complex and sophisticated of a global supply chain as this company has is always subject to a huge amount of risks. Global expansion can sometimes run afoul of the Foreign Corrupt Practices Act for example. There is also always the chance that aggressive acquisition strategies backfire, but again here the company has a solid track record.

However, Albemarle’s resource portfolio does avoid some of the trickier geopolitical areas. The mine in Australia it has been developing experienced high construction costs and many of its expansion projects are subject to all kinds of risks.

There are so many experts and interlocking groups of folks who need to successfully coordinate in order to extract what this companies does and then turn it into a usable material for end-customers. The culture of the company and the focus on improvement and cost cutting (which it is ahead of estimates on) is a good risk mitigator for the myriad risks that can encumber such a company.

Right now, it is possible that forecasts for Electric Vehicle adoptions could be higher than it indeed turns out to be in reality. Companies like APTV -0.36% , who we earlier covered, are making the necessary raw materials in EV’s come down to a more comparable level to ICE vehicles.

If there is some major innovation in batteries that reduces the need for lithium, it would certainly put a wrench in the companies plans and change the economics of several ongoing projects. Certain realities may brush up against the coming EV revolution though, like the inability of current power grids to support a rapid shift.

OEMs in the auto space, a key driver of the company’s anticipated future growth have also been very subject to shortages of semi-conductors, both the legacy kind that were so badly effected by the Renesas fire. However, several trends in newer vehicles mean they will also need more cutting edge chips then ever. If chip shortages or supply chain problems continue to curtail auto production, it could put a wrench in the company’s goals in the short-term.

Lastly, the company has enjoyed a good run recently and is definitely subject to some pricing risk in the event of an macro setbacks. The company is up 148% in a year trades at a pretty rich a forward P/E of 47x. Like we said though, these guys are playing the long game and so should you if you decide to purchase this stock.