Summary

- The shale industry is looking attractive given high oil prices and recent trends in the industry that responded to investor concerns and previous failures.

- EOG Resources has been a leader in the industry not only in reducing costs but also in reducing environmental externalities.

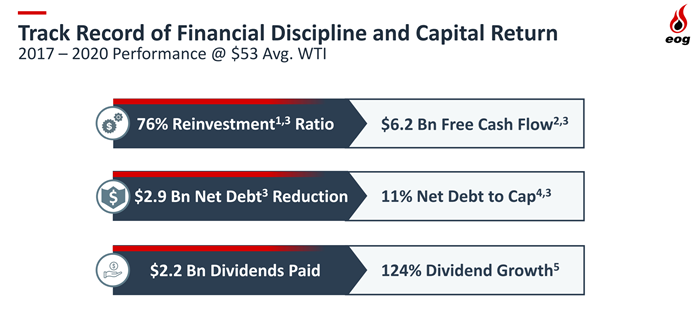

- The company significantly mitigates the effect of the inherently volatile nature of Shale E&P by consistently reducing costs and increasing efficiency over time and also providing consistent dividend payments directly to shareholders.

- The company had a record quarter for FCF in Q1, enough so to offer a special dividend of 1$ per share.

- There’s a lot to like about it from a technical, fundamental and earnings potential perspective about this established upstream play.

Times are looking up for shale. It’s proven proclaimers of its premature death wrong again. We are emerging from a macabre pandemic reality where millions have perished. We’ve all seen shocking numbers tallying the dead day in and day out. What is less evident in such a profound moment is that certain caricatures of the past have likely forever perished as well.

What is a shalesman? Something that’s not really around anymore in the days of tightening belts and uncompromising dedication to cost efficiency. The shale exploration and production business is the riskier side of an industry that makes a living drilling holes in the ground.

While the environmental concerns may be at the more relevant end of the headlines today (and our subject is as well-positioned in that area as any company in the industry), there are many stories of excess, duplicity, and a long trail of bankruptcies that give investors legitimate reasons to have hesitancy about this adventurous side of the Energy sector that harkens the uniquely American, raw go-get-em’-ness of San Francisco in 1849. It is highly cyclical, and to say it is a ‘boom, bust’ industry wouldn’t tell you the half of it. In 2013 and 2014, an exodus of strippers and sex workers flocked to North Dakota of all places.

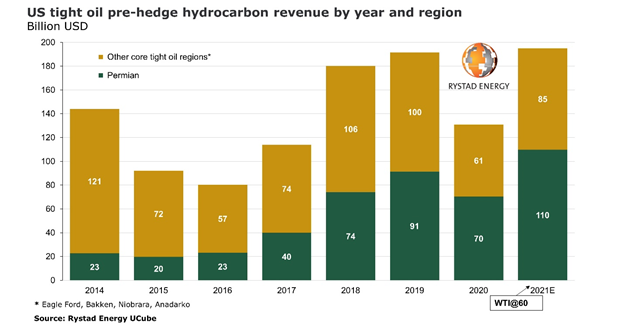

Source: Company Reports

Why? Well, the armies of Bakken roughnecks overindulged on lobster and filet and drunk on Johnny Walker Blue (often probably supplied at the expense of investors and shareholders) made easy marks, and many girls were able to rake in up to $10,000 a night. There were probably even a few who accepted Bitcoin and found a pleasant surprise in their wallets a few years later, but we digress.

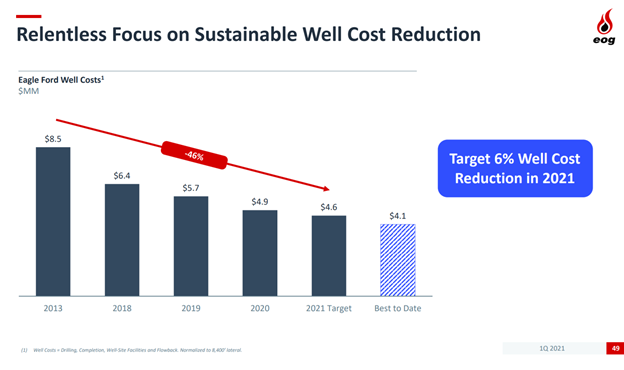

Of course, many pointed out that this mania was unsustainable. However, in 2014 when oil dropped from over $100 to $43 in relatively short order, the industry defied the naysayers and survived. Not only did it survive, but it also matured. EOG has been one of the leaders in reducing the cost and making shale more attractive to investors by balancing the inherent volatility with consistent dividends fueled by tight asset management and shrewd acquisitions. Shale is an industry where relentless focus on the small things can pay huge returns, and this company excels at this and has done so before the additional pandemic incentives.

Source: Company Reports

Is The High-Drama Of Shale a Thing of The Past?

The ridiculously high break-even prices to make wells profitable began to drop as innovation increased. We would consider EOG one of the leaders of this new, responsible shale that reveres shareholders and the environment rather than seeing them as Daddy Warbucks and people with concerns about flammable water as mere Cassandras. Their focus on rewarding shareholders with dividends and building long-term value by constantly re-investing in more efficient projects has paid significant dividends, literally.

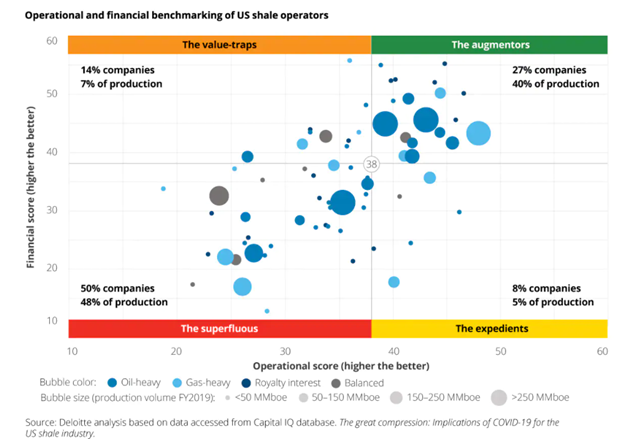

They are executing a common-sense, shareholder-oriented strategy. EOG Resources isn’t a fox-hole convert to seeing things shareholders’ way either; it’s been a trailblazer. This company has a track record of fiscal discipline and sound management instinct for accretive acquisitions. This distinguishes it from the Lord make me pure, but not yet attitude of others in the industry. EOG is an upper right quadrant name for sure!

Source: Deloitte

The world has changed. Gone are the days of reckless profligacy. Despite the solid state of debt markets, investors have gotten more discerning on shale after learning hard lessons. The old caricature of the Shalesman is likely gone as supply dynamics are decidedly in the industry’s favor but also as this converges with a balance of power that has tilted decisively in favor of investors.

For all the controversy around shale, it revolutionized American energy production. It is the bane of Sheikhs and the source of economic elan of certain corridors of rural America, much of which would have otherwise been considered wasteland. The solidness of the company’s management and position can be seen in its EPS forecast trends compared to peers. Our Head of Global Portfolio Strategy, Brian Rauscher, also has seen positive developments in his work on the name.

Source: Fundstrat, Bloomberg

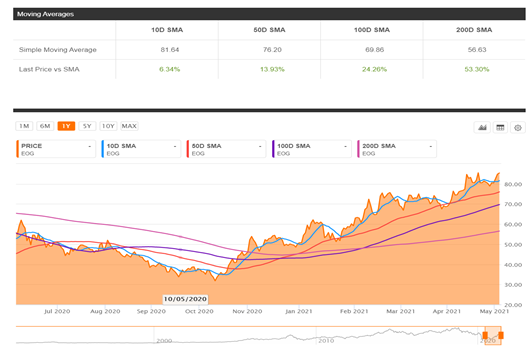

A Great House In A Neighborhood That Is Getting Better

Source: SeekingAlpha.com

The firm is looking very healthy from a momentum perspective and is trading above major moving averages. It has participated in Energy’s latest rally and it’s consistent track record means it will probably be a good candidate to attract institutional capital as it likely piles into Energy in line with our Head of Research, Tom Lee’s prescient prediction.

EOG’s management ensures that it is one of the premier shale plays across multiple dimensions, including the increasingly important ESG angle. In an industry known for getting by on transitory derivatives gains, EOG has a strong balance sheet and is ruthlessly executing a sound strategic vision. It’s making cash and giving it to shareholders.

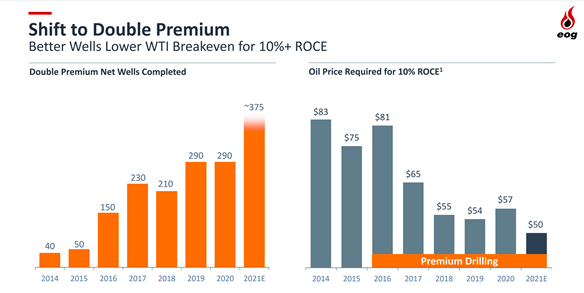

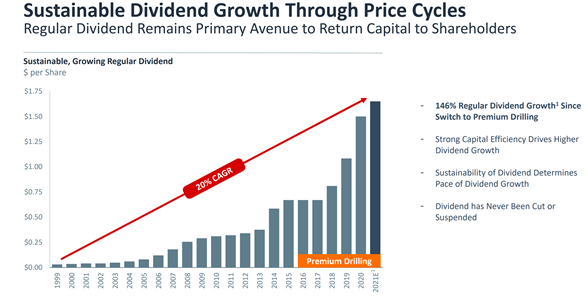

Over the past four years, it has had triple-digit dividend growth. The price of oil necessary to achieve a 10% ROCE has gone down from $80 over the same period to an estimated $51 in 2021, and management actions should result in it continuing to drop.

Source: Company Reports

The company’s consistent track record of making the right moves at the right time in the industry have resulted in it having a significantly better balance sheet in many respects than peers. Its low-cost and low-hanging-fruit approach to shale production have continually rewarded shareholders both in terms of dividends and definitely in price appreciation since the nadir of the pandemic.

However, shale is a sub-industry that is prone to value traps and we think the mid-level valuation compared to peers is actually a positive in that respect and shows that the market is rewarding the companies that reward shareholders and don’t destroy the weighted average cost of capital with debt activities.

Source: Company Reports

The focus on premium drilling which significantly reduces costs has also continued to benefit the company and is now a strategy that is being copied by many competitors.

However, one thing competitors can’t copy is the attractive portfolio of shale assets that the company has acquired over the years. It has great assets, low costs of production and is leveraging physical assets with its technologically advanced network that not only helps lead the industry in reducing environmental externalities but also helps it to continually reduce costs and build value.

This indefatiguable persistence in reducing costs that has occurred across multiple cycles and supposedly apocalyptic downturns shows that there’s a unity of vision and execution over the years that again stands in stark contrast to some of the stereotypes about the industry. This seasoned Houston management team has the secret sauce and keeps delivering.

Source: Company Reports

Epicenter of Energy Was Already Moving Toward Efficiency Before COVID-19

The under-the-gun, innovate or die situation that has now befallen many industries due to the most significant economic shock of our lifetimes is standard procedure for the volatile and highly leveraged shale industry.

Indeed, by the Economist’s calculations, the shale industry has had a net negative cash flow of $300 bn and has impaired $450 bn of capital since 2010. In addition, there have been nearly 200 bankruptcies. So discernment and caution when investing in this space are critical.

We think EOG passes muster, and from the sounds of how their management is prioritizing the interests of shareholders, you’d be hard-pressed to associate them with the antics of the shadier sections of their industry. EOG is a classic Epicenter story innovating on the fly, boosting efficiency and production, and slashing operating costs.

Their boyscout management stands in stark contrast to the wildcat reputation of the shale industry. One thing is for sure; when oil does well; shale does very well. In a world where the Permian can produce 12% returns at $45 a barrel and Saudi Arabia’s break-even price has risen to $64 from $51 in three years, it would appear bright days are ahead.

These days will likely be brighter than any in the past for shale players that do right by shareholders, and we think EOG is the exemplar.

Source: Company Reports

American entrepreneurialism has always had a rugged component. Gentlemen and members of titled families often founded Europe’s industries. American entrepreneurialism has far more ruffians, rebels, and rogues in origin stories of our business dynasties.

The banking system took much longer than a century to get to the stability we see today. Many old banks in the Old West would have sparse gold and cash covering the top of a barrel of nails to give the illusion of financial propriety.

Few industries exemplify the old wild-cat nature as the American Shale Boom did after its volatile and storied rise over the past decade and a half. The technological innovation that has kept this industry alive through several periods where its death has been prematurely proclaimed is both revered for its effectiveness and detested for its environmental impact. As a result, this industry is one of the more controversial in the United States.

Still, it has matured, and EOG’s management and prioritization of shareholder interests make them seem more like choirboys than the cowboys you expect from the industry’s reputation. We think their track record of execution and delivery proves they really do have hearts of gold from the perspective of a shareholder.

Risks and Where We Could Be Wrong

As we have noted, the shale industry is full of risks but a lot of them have materially declined over the years. One of the key risks was exposure to low oil prices. However, as we mentioned EOG has been an industry leader in getting these costs down and mixing the expected price volatility with consistent dividends over a few different tumultuous periods.

We would say the consistency and pace of dividend growth is one mitigating factor for any price risk that exists. While this method of mitigating risk might not be as in fashion as it used to be, it still matters and it still works!

In a world where the company has survived negative oil, the price risk seems like less of a concern, but it is still a major factor in profitability and management’s ability to continue delivering to shareholders like it has. Therefore, COVID-19 and the associated uncertainty regarding its potential impact on demand remain the major risk for this name, like so many other Epicenter stocks.

That being said, there are still plenty of other risks. Despite being a leader in efforts to reduce the environmental impact of the industry’s practices, a major risk still remains that capital simply won’t find the industry appealing over time. While the image has certainly cleaned up partially by EOG’s efforts, the fringe of bad actors could always bring back some of the reputational damage that affects even the good guys.

Hopefully, this will be avoided by the empowerment of shareholders as other sources of capital have become less plentiful. There are always major risks that management can blow up a derivatives trade or that they can fall behind technologically. However, we see their decentralized and innovation-friendly culture as another mitigating factor to this key risk.