The first full week of May every year is National Pet Week. We therefore thought it might be interesting to take a look at businesses that help keep our beloved animal companions fed, healthy, and happy – from an investor’s perspective, of course.

On April 30, Walmart (WMT -0.75% ) announced that it was closing all 51 of the healthcare clinics it had been operating in stores across the U.S., ending its virtual healthcare offerings as well. The company disclosed that the initiative, which had targeted underserved communities with limited healthcare access, proved to be unprofitable due to the “challenging reimbursement environment and escalating operating costs.”

Walmart’s announcement did not mean that it was exiting the field of health care entirely, however. The company is simultaneously expanding its offerings in health care for a different type of customer – the four-legged variety. On September 20, 2023, Walmart announced the opening of a Walmart Pet Services center inside its store located in an Atlanta suburb, where customers could bring their furry friends in for veterinarian visits and dog grooming. The retail chain said it planned to open more such centers in the near future, to be staffed by PetIQ (PETQ), which has been renting Walmart store space for its own clinics since 2016.

Of course, Walmart has sold pet food and other pet-related products for decades, but the new clinic appears to suggest that the retail giant sees potential in the pet-related market. There are some reasons to be optimistic, but it is also true that many pet-related stocks have not done well in the past year.

Pet ownership

Walmart isn’t alone in seeing potential growth in the pet-related market. Academia does as well, apparently: faced with increased demand for veterinary services (and a shortage of veterinarians), the AMVA last fall announced that 11 universities had announced plans to launch veterinary schools. In a November 2022 report, Morgan Stanley researchers projected 8% annual growth in the pet industry by 2030.

That growth begins with the increase in pet ownership – both in the U.S. and around the world. The American Pet Products Association estimates that 66% of U.S. households own a pet. That figure has grown steadily since 1988, when just 56% of households owned a pet, and this trend is expected to continue.

Also noteworthy is that among those households with pets, the percentage with more than one pet has also grown:

Meanwhile, pet ownership is also surging in countries with a growing middle class. For example, The Economist reports that China’s pet industry grew an estimated 25% to $58.6 billion in 2022, driven in part by many young professionals opting to have “fur babies” instead of human ones. Meanwhile, the research consultancy Market Decipher estimates that increasing pet ownership in India should lead to a tripling of the country’s pet economy over the next decade.

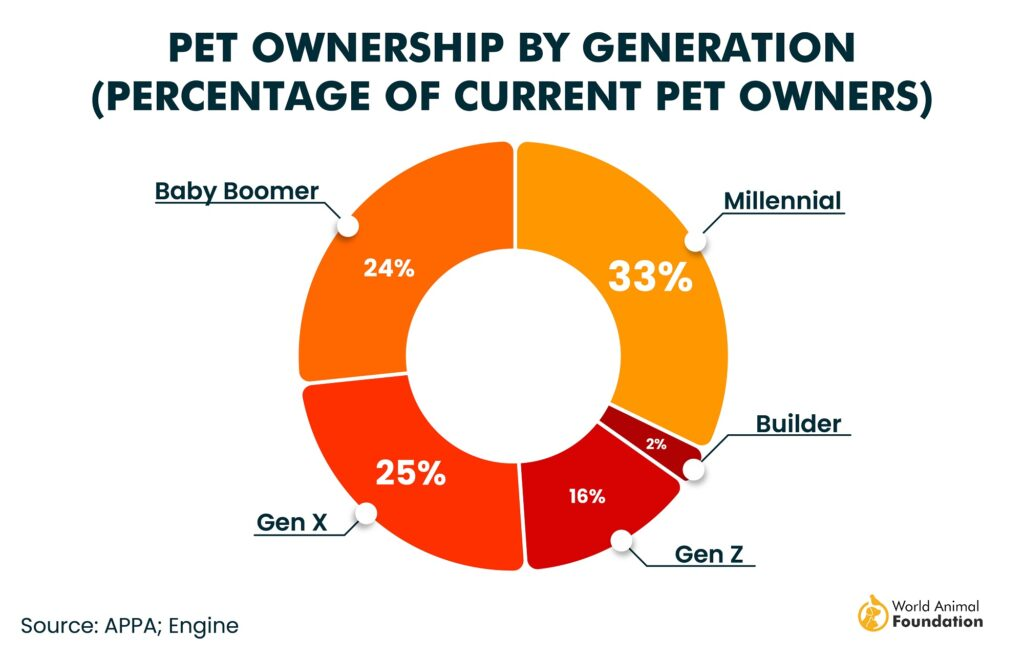

Within the U.S., pet ownership is very much popular across generations, but especially the younger generations. Millennials make up the largest demographic within this group – 33% of pet owners are of this generation, but as Generation Z advances into adulthood, they are following suit.

As Fundstrat clients have heard Head of Research Tom Lee say many times, demographics are destiny. This might bode well for the companies that are part of the overall pet economy – companies are generally grouped into the Consumer Staples category. Surveys show that during economic down cycles, spending on pets tends to be somewhat stable. MarketPlace, a market-strategy research firm, found in a survey that 19% of pet owners would sooner cut spending on their own food expenses during tough economic times than reduce spending on their pets.

The costs of pet ownership are not insignificant. In the U.S., household expenditures related to pet ownership in 2023 totaled $147 billion, including pet products and pet-related services, and the American Pet Products Association expects the 2024 sum to reach $150.6 billion. With pet ownership expected to grow, the companies in these industries are arguably positioned to benefit.

Pet foods and other products

Unsurprisingly, one of the biggest costs of pet ownership involves food. The market research company NielsenIQ estimates that U.S. households will spend $66.9 billion on pet food this year (pet food includes snacks and treats), up from $64.4 billion in 2023.

Many of the most recognized brands of pet foods are manufactured by food conglomerates such as Nestle S.A. (NSRGY), which owns brands like Purina, Friskies, and Fancy Feast; J.M. Smucker (SJM -2.51% ), owner of Meow Mix and Milk-Bone; and Post Holdings (POST -1.25% ), owner of Kibbles & Bits and 9 Lives. One specialized pet-food company is Freshpet (FRPT -1.56% ).

Freshpet (FRPT -1.56% ).

Unlike traditional dry, wet canned, and semi-moist pet foods, Freshpet’s offerings are – appropriately – fresh, in that they need to be kept refrigerated. Fresh pet food is the newest, smallest, but also fastest-growing market segment of the pet-food space – data by market-research firm Circana shows that fresh dog food sales are up 86.5% from 2021 to 2023, and fresh cat-food sales are up 63.8% over the same period.

Consumers also spend on pet-related products, a category that includes over-the-counter medications. While major retail giants like Walmart stock both pet food and pet-related products, several retailers specialize in selling goods geared toward animal companions.

Chewy (CHWY 4.12% )

Chewy is an online retailer of pet products, including food, supplies, and accessories, primarily focused on sales through subscriptions and auto-ship options. The company also has pet healthcare offerings that include pet insurance, telehealth, and prescription medications. It recently began expanding outside the U.S., launching its Canadian operations in 2023. There have been concerns that Chewy might lose out to the e-retail giant Amazon, but company statistics suggest that as many as two thirds of its customers shop with Chewy despite having an Amazon Prime membership.

Petco Health and Wellness Company (WOOF 0.41% )

Petco sells pet products through roughly 1,500 brick-and-mortar locations in the U.S. and Mexico. Like Chewy, Petco has also been expanding its range of products and services, including prescription drugs, dog grooming, telehealth and in-person veterinary services, dog training, and insurance.

Healthcare

The other major expense related to pets involves health care. As with their human counterparts, most healthcare providers for pets are privately held. One exception to this is PetIQ (PETQ).

PetIQ (PETQ)

PetIQ offers veterinarian services through partnerships with retailers such as Walmart, Meijer supermarkets, and various pet-supply stores. At these in-store clinics, PetIQ offers checkups, vaccinations, microchipping, and more. The company also has a line of prescription and over-the-counter pet medications, treating conditions and ailments including arthritis, diabetes, parasite infections, and antibiotics.

The demand for prescription-level medicines for pets is significant and growing. Some familiar names from the (human) pharmaceuticals sector have taken notice. Merck, for instance, reported that 3.2% of its 2023 revenues came from its “companion animal” division. (The company also offers a range of medications for livestock.)

In general, the animal pharmaceuticals industry is noted for having significant pricing power due to industry fragmentation, limited competition, and – unlike with human pharmaceutical companies – the lack of third-party payment intermediaries such as insurance companies or government programs like Medicare.

Zoetis (ZTS 0.23% )

Zoetis is one of the largest animal-focused pharmaceutical companies, deriving roughly 60% of its revenue from pet-related treatments, vaccines, and diagnostic tools. (It also develops healthcare products for livestock.) Its companion-animal treatments cover a range of ailments, from arthritis to noise aversion and separation anxiety.

Elanco (ELAN 1.74% )

Originally part of Eli Lilly, Elanco offers more than 200 products to treat a wide range of animals, including pets and livestock. For companion animals its products include treatments for parasites, arthritis and pain relief, and skin/coat conditions, as well as nutritional supplements. The company is also a leading manufacturer of pet microchips.

Idexx Laboratories (IDXX 1.26% )

Last but not least, Idexx is a maker of diagnostic products and practice-management software for veterinary practices and animal hospitals. The company has operations around the world, and while it has long been active in the livestock space, it has recently begun to focus more on products for use by companion-animal veterinarians.

In closing, we wish to reiterate that this piece should serve merely as an examination of the various industries that help owners keep companion animals healthy and happy, and the investment potential they might represent. Several of the companies mentioned above, though prominent in their respective industries, nevertheless seem to be on uncertain footing. Careful additional research should be done before making a decision to invest in them. As usual, Signal From Noise should serve as a starting point for further research before making an investment, rather than as a source of stock recommendations.

We encourage you to explore our full Signal From Noise library, which includes deep dives on airliner manufacturing and opportunities arising from the urgent need for strong cybersecurity. You’ll also find a recent discussion of weight loss-related investments, artificial intelligence, and the Millennial generation.