The last trading day of February has come to a close. The S&P 500 closed the second month of 2026 down 0.87%. That number is arguably far from catastrophic, but as Fundstrat Head of Research Tom Lee noted this week, “I think many people are going to be glad to put this month behind us,” acknowledging that it was “quite turbulent.” As he has been pointing out, the market in February felt like a bear market to many investors for a number of reasons, including concerns about what AI means for software stocks, and a “thematic ballast shift” within the AI trade itself—away from the metaphorical AI “armies” of the Magnificent Seven and toward the “bulletmakers” that supply them, such as data-center construction, energy companies, and others.

Yet even before these trends appeared on the horizon, historical precedent had suggested the possibility of a largely flat February. Since 1950, there have been 36 years in which the first five trading days of the year and the month of January have both been positive for stocks. The win ratio has largely amounted to what Lee depicts as a “coin flip,” with median gains of 0.4%. Yet that same historical precedent suggests the likelihood of a stronger March.

“I do think that March is likely an up month,” Lee said, and that’s not just due to the precedent. As he noted, February has arguably reset valuations for the Mag Seven (see our Chart of the Week below). His views for March are arguably an improvement from last week, when he tempered his optimism by telling investors at the time that there’s “no need to be a hero.”

For Head of Technical Strategy Mark Newton, however, this caution is still warranted. At our weekly huddle, he suggested that investors might wish to refrain from “getting too emboldened” at the moment. “My own cycles tend to think that the spring could bring about some consolidation,” Newton said.

Yet despite the slight differences in their views on timeframes, the two are largely in agreement about one thing: software. “Software is on the verge of trying to turn,” in Newton’s view. From a tactical perspective, “I’m increasingly looking at making a bet on being long software and to be short semiconductors,” he said. “It might be wise to consider […] thinking we’re due for a pretty good bounce in this group” over the next couple of months.

Lee’s views are similar. “I think for software, a lot of the bad news is priced in, and the sellers are largely done selling,” he said.

Chart of the Week

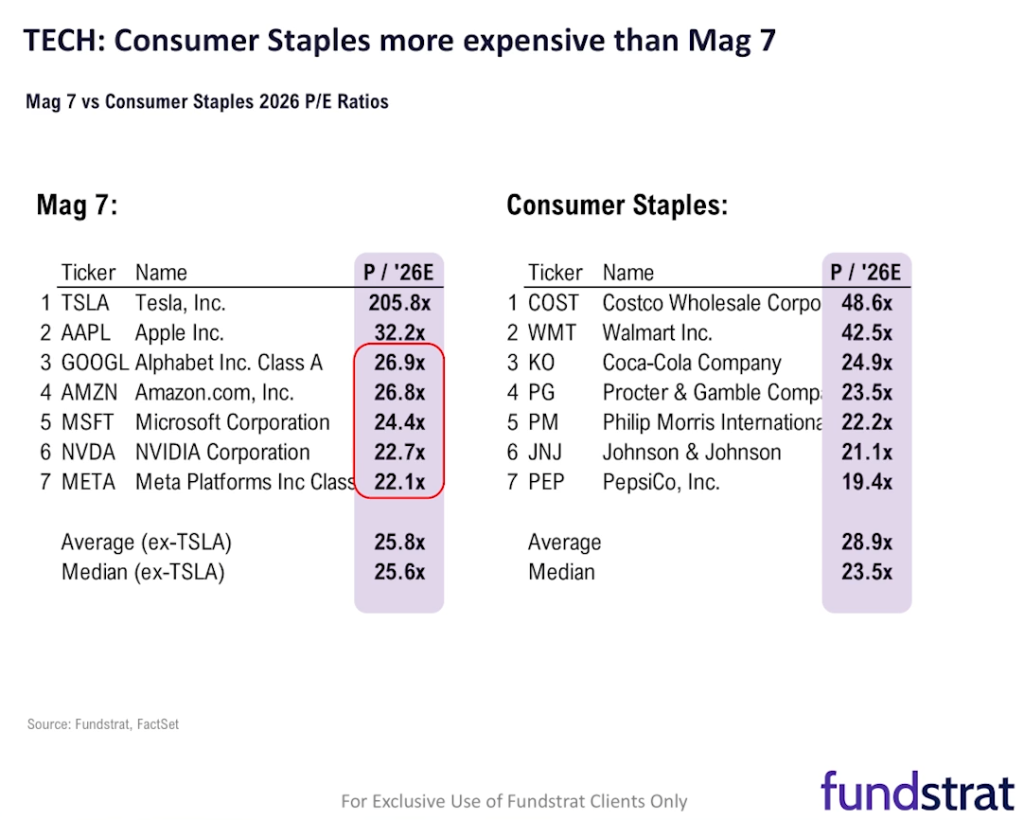

One reason for Fundstrat Head of Research Tom Lee’s constructive outlook for March has to do with Magnificent Seven Valuations. February arguably reset those valuations to the point where they are trading at a discount relative to the aforementioned bulletmakers (see above) in the AI trade. In fact, as Lee noted, Mag Seven P/E ratios are now comparable to—and in some cases, lower than—the multiples of some stocks in the staid consumer staples sector. This is illustrated in our Chart of the Week.

NVDA -4.02% has managed to clear prior highs of the last couple months ahead of today’s earnings report, which is a mild positive if/when NVDA manages to close above $194. My cycle studies which i presented night suggest that a possible turn back lower might happen in NVDA in mid-March, so my feeling is that today’s earnings might present a “sell on the news” type event if/when NVDA pushes higher after earnings into tomorrow. Above $194 the first resistance that stands out lies near $200.94 and if this holds within the next three days on any sort of muted reaction, than i would suspect this should be strong resistance and might result in a reversal into next week. (Above $200.94 on any upside gap lies $212.16, the intra-day highs from 10/29/25. Bottom line, this move above $194 is happening before the earnings are even out and given its sideways range since last Summer, i am not inclined to “chase”.

At 9:00 tonight President Trump will need to walk a fine line as he tries to recapture the momentum he had last year when Congress approved his Big Beautiful Bill. As he stands at the podium looking out at Congress, his Cabinet, special guests and likely some of the 6 Supreme Court Justices who voted against his tariff policy he will need to stay on message and stick to the speech in the teleprompter. He is expected to cover a broad range of issues including tariffs and the economy, healthcare policy, possible attack on Iran, his Board of Peace and Gaza/Israel situation, status of his immigration actions, and the shutdown at the Department of Homeland Security. With this full agenda the President has warned it will be a long speech. SOTU speech usually has a large audience of over 40 million viewers. It gives the President the opportunity to reestablish his agenda and reconnect with the voters who sent him back to the White House for his second term.

The key takeaway from this weekends announcements are that Tariffs are not going away anytime soon, even if SCOTUS has ruled against his emergency tariffs under IEEPA as the Administration can still put in a full embargo even if they cannot collect right away and other methods such as Section 122 can be utilized, so Scott Bessent discussed revenues being unchanged as other methods are available. However, the unexpected news on 15% levels has resulted in some early week selling in US Equities ahead of the State of the Union speech and NVDA earnings, but has not resulted in any meaningful technical damage. Crude oil and precious metals are both higher this morning and ^SPX is lower by -0.70% led by Consumer Discretionary, Technology and Industrials. Yet, six sectors are higher this morning (albeit mostly defensive groups except for Comm. Svcs) and as such market breadth is lower by just 3/2 negative. As shown below, this area near 6850 in SPX initially has importance based on the minor uptrend from last Tuesday’s lows and under its proper to watch 6833. On the upside, any reversal which manages to eclipse 6917 would help the rally get back on track.

This research is for the clients of FS Insight only. FSI Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or FS Insight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FS Insight. At the time of publication of this report, FS Insight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FS Insight is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

FS Insight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of FS Insight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by FS Insight clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of FS Insight, which is available to select institutional clients that have engaged FS Insight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

FS Insight does not have the same conflicts that traditional sell-side research organizations have because FS Insight (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by FS Insight and/or affiliates of FS Insight. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of FS Insight.

This research is for the clients of FS Insight only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but FS Insight does not warrant its completeness or accuracy except with respect to any disclosures relative to FS Insight and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where FS Insight expressly agrees otherwise in writing, FS Insight is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fsinsight.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.