A decline in shares of risky, glitzy companies didn’t bother the S&P 500 too much but weighed on the tech-focused Nasdaq composite in the new year.

The S&P 500 added 0.2% on the first trading day of 2026, with eight of the 11 sectors finishing in the green.Cyclical corners of the market, such as the energy, utilities, and materials sectors, were the top performers on Friday. The broad-based index finished the week down about 1%.

The Nasdaq composite, meanwhile, was unchanged on Friday, and the Dow Jones Industrial Average added 0.7%. Over the holiday-shortened trading week, they fell 1.5% and 1.3%, respectively.

Shares of Tesla fell 2.6% Friday, after the electric-vehicle maker reported a second straight annual drop in vehicle deliveries. Instead, Chinese carmaker BYD is the top seller of EVs across the globe. Other laggards this week were AppLovin, with shares of the mobile advertising platform down 13%, while Palantir and Carvana fell 11% and 8.7%, respectively.

Their stocks have been on a roller-coaster ride in recent months, but the losses this week could have been exacerbated by low trading volume, a hallmark of the year-end.

The declines could also be a sign that investors are reconsidering some of the more risky parts of their portfolios due to worries about AI companies overspending on capex with no clear path to monetization. AI-related companies were trading sideways during most of the second half of last year.

Among the areas of the market that were in the green on Friday were shares of chipmakers. Nvidia shares rose 1.3% and Intel added 6.7% on Friday. In particular, memory-chip makers posted a furious rally, with Micron and SanDisk shares up 11% and 16%, respectively.

As an exception to investors’ risk-off mood in 2026, bitcoin rose 1.3% Friday. The cryptocurrency faced steep losses in 2025, falling 6.3%.

Editor’s Note: As our research heads were on a well-earned holiday break this week, they didn’t publish research. We will resume sharing their latest commentaries next week.

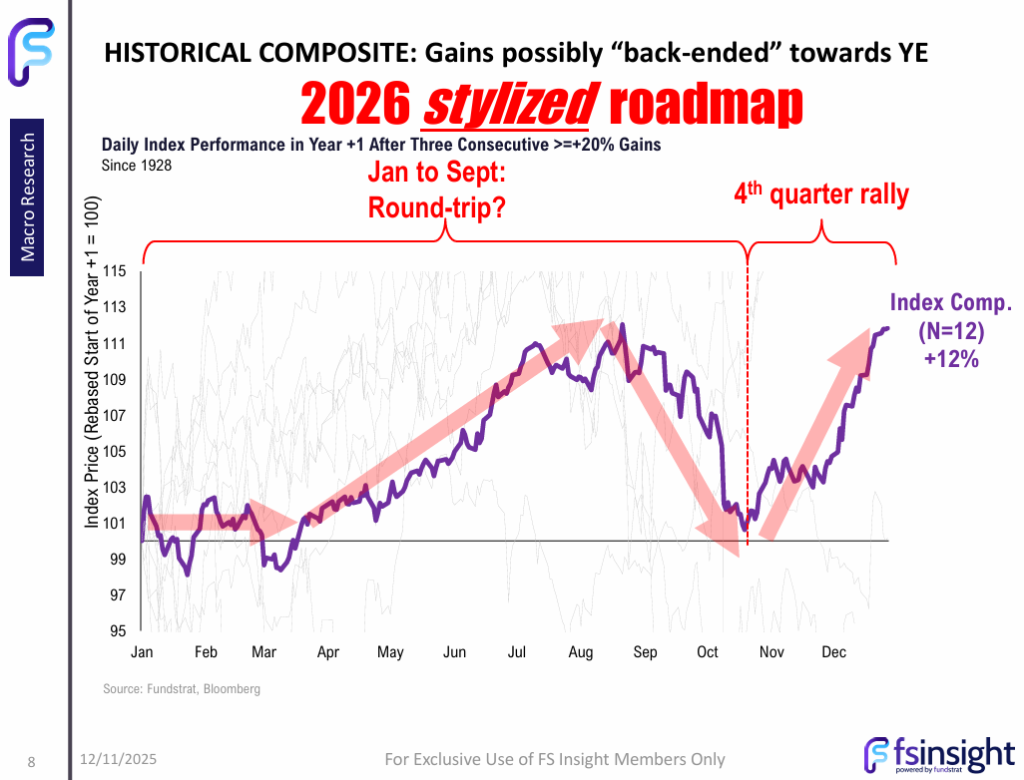

Chart of the Week

There were few economic reports released over the week, so the Federal Reserve’s minutes on Tuesday were in focus, which further showed just how divided officials were on Dec. 10 regarding the final decision to cut interest rates by a quarter-percentage point. With the current Fed chair’s term set to finish in May, the expectations are that the new Fed chair will be dovish. Our Chart of the Week has more details on how we expect it to affect stocks this year. The yield on the 10-year U.S. Treasury note was at 4.187% to end the week, compared with 4.137% last Friday.

We continue to be hit with a plethora of Economic data and today’s GDP at 4.3% Annualized seen as a huge positive and being driven by Consumption. Exports recorded their strongest quarter in a year, and despite being lagged data, (happening ahead of the Govt Shutdown), this is a reassuring signal for the market. What’s interesting though remains the lackluster sentiment of the Consumer, as Consumer Confidence showed nearly the lowest reading in five years. Thus, there’s an interesting divergence between the actual spending (consumption) vs. how Consumers “feel”. As Tom Lee has noted for months now, however, this remains a very politicized data point, but lackluster sentiment data like this certainly continue to be an arrow in the quiver for the Bulls

^SPX has now risen to test the highs of this resistance Triangle which was formed in late October nearly two months ago. However, more sectors are lower today than higher and breadth is negative by around a 3/2 margin. (This won’t matter to many outside of those who are truly short-term focused) However, some good broad-based representation among today’s leaders, as FCX 2.38% JBL 5.07% GILD -0.93% AZO -3.44% and C 1.78% are leading today, covering most major sectors. However, Technology is down -0.67% today in equal-weighted terms, while XLK 0.28% is positive, so there’s some definite evidence of NVDA’s gains helping large-cap tech along with JBL and SNDK. Trends are bullish and QQQ continues to lag performance with QQQ well below initial resistance near 627 and then 637, both being important for QQQ. However, as shown below, SPX is doing better structurally and leading the major indices heading into late December. For now, 6903 will be the “line in the sand” for SPX bulls and i do anticipate an eventual period of catchup for QQQ as NVDA”s rally starts to grow stronger into January.

FSLR 5.02% breakout worth following after having exceeded the base that’s held this stock range-bound since early November. UPTICKS holding First Solar likely should push higher to test June 2024 peaks initially, near $306.77, then $321, $362. Volume on this breakout is already $2mm and is likely to be heavier than any time in the last few months. It’s right to be bullish, and today’s move should lead to upward acceleration, technically speaking.

This research is for the clients of FS Insight only. FSI Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or FS Insight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FS Insight. At the time of publication of this report, FS Insight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FS Insight is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

FS Insight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of FS Insight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by FS Insight clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of FS Insight, which is available to select institutional clients that have engaged FS Insight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

FS Insight does not have the same conflicts that traditional sell-side research organizations have because FS Insight (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by FS Insight and/or affiliates of FS Insight. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of FS Insight.

This research is for the clients of FS Insight only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but FS Insight does not warrant its completeness or accuracy except with respect to any disclosures relative to FS Insight and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where FS Insight expressly agrees otherwise in writing, FS Insight is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fsinsight.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.