Stocks have been largely flat of late, with the S&P 500 creeping up ever-so-slightly last week and the Nasdaq Composite showing similarly modest gains. These numbers are the result of improving breadth and performance in sectors outside of technology. The larger tech stocks have largely felt pressure in the face of continued concerns about AI, punctuated by recent news from Broadcom (AVGO -0.67% ) and Oracle (ORCL -4.48% ).

Oracle reported funding issues for its planned Michigan AI center, with Blue Owl Capital notably declining to provide backing despite having frequently done so for Oracle in the past. But as Fundstrat Head of Research Tom Lee reminded us, this does not necessarily reflect on the viability of the AI thesis. “Progress in AI will never be a straight line up and to the right,” he pointed out, “and this setback, to us, seems like a normal course of business.” He added, “Not every deal will have the same set of partners.”

Similarly, Head of Data Science “Tireless” Ken Xuan seemed largely unperturbed about Broadcom’s earnings (and the market’s reaction to them) during our weekly research huddle. “I thought the earnings numbers were fine, they show that the business is still growing,” he told us, though he acknowledged that Broadcom’s ASIC-focused business is arguably more prone to competitive pressures.

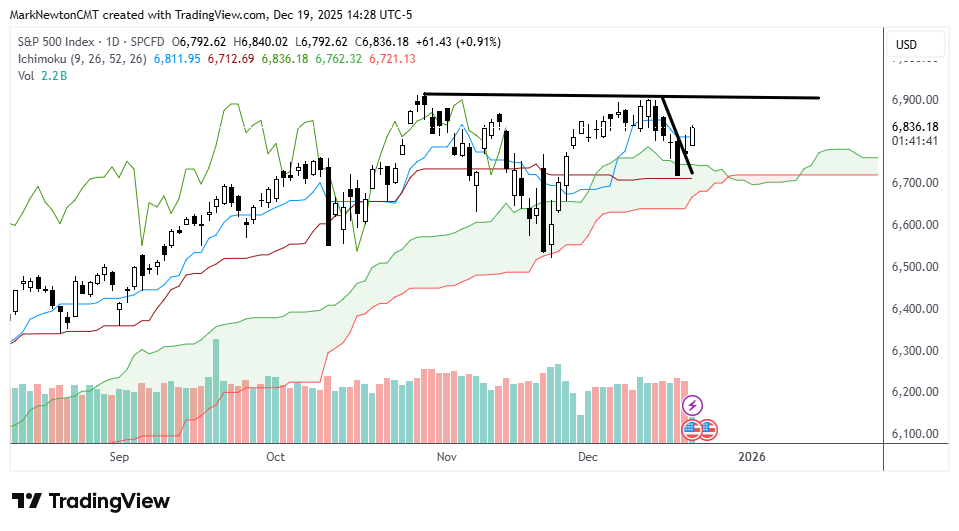

Head of Technical Strategy Mark Newton sees near-term constructivism as justified. “It’s interesting that growth projections continue to rise, which would be great for earnings, and inflation appears to be potentially nonexistent. To me, that’s a real Goldilocks-type scenario for the market, at least in the short run.”

Though broader indices have not exactly wowed casual observers this week, Newton told us “the market is really not as bad as what the tape has shown. Breadth in the last two weeks has actually gone straight up,” he continued, with new highs in view for equal-weighted S&P 500, small caps, and Dow transports. “Those are all very big positives,” he asserted. The S&P 500 successfully exceeding 6,800 on Thursday gave Newton optimism for a rally over the last two weeks of the year. “This, to me, suggests that we are likely going to 7,000 between now and end of year.”

That’s a call that puts Newton’s near-term views largely in line with Lee’s, who wrote that “seasonals remain favorable, and we see at least 5% upside into year-end which implies S&P 500 at 7,000 or more.”

[Editor’s note: FS Insight Snapshot will not publish on Dec. 28, 2025. It will return Jan. 4, 2026. We wish all members of the FS Insight community a happy holiday season and a healthy, prosperous 2026.]

Chart of the Week

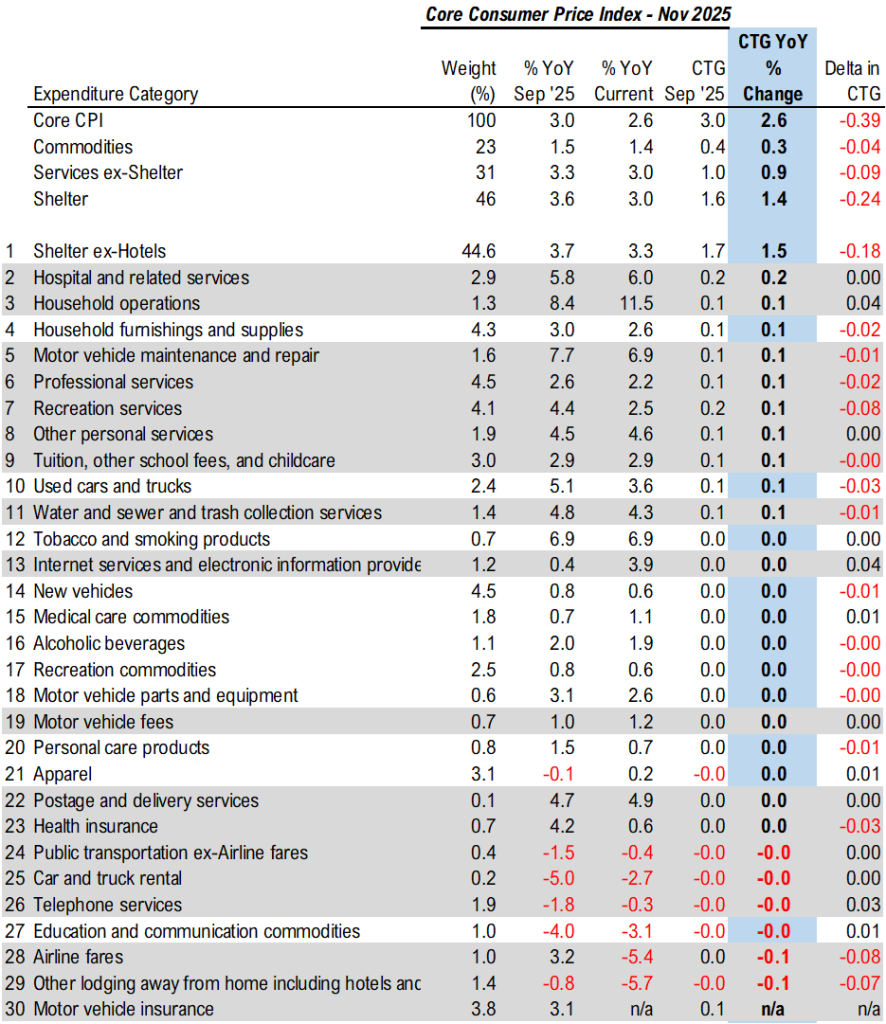

Our Chart of the Week shows a drill-down of the latest CPI report, comparing November with September. (Due to the federal government shutdown, October 2025 CPI was not compiled.) The latest inflation numbers are supportive of a constructive thesis for stocks as we look forward: Core CPI coming in at 2.6% YoY, significantly lower than consensus expectations of 3.0%. As Fundstrat Head of Research Tom Lee notes, falling inflation arguably leaves the Federal Reserve free to focus on the other part of its dual mandate – supporting a high level of employment. In his view, “this means a Fed ‘put’ is now in place for the economy.” To him, “a Fed put on the economy is bullish for stocks, because the quickest way to strengthen the economy is the wealth effect – for stocks to rise.”

With 90 minutes left of trading today, ^SPX remains near the highs of the day and is not giving up gains like it did partially in trading yesterday. SPX should be pushing back to new highs over the next couple weeks and the first area of real importance now on the upside lies near 6900 but should be exceeded into year end if my thinking is correct. Technology is the overwhelming leader today, and the only sector higher by more than +1.50% Meanwhile, Consumer Staples is lower by nearly 1% and generally fits with a risk-on theme as Defensive areas continue to underperform.

Nov CPI report released. Came in way under consensus 2.6% YoY vs consensus 3.0% Inflation falling like a rock This is bullish and why we stay constructive on stocks We see S&P 500 7,000-7,300 by year end

Lows to this pullback from early December are likely in place, as ^SPX has exceeded the minor downtrend from 12/11 highs at 6772 and should begin trending back to highs. CPI came in weaker and as Tom Lee discussed earlier, inflation is “falling like a rock”. Market breadth is nearly 3.5/1 bullish which is a very good sign and should drive SPX up to 6902 and then over to 7000-7100 potentially into year-end. Technology’s 2% rally today along with 1% gains in Industrials, Discretionary are very good signs to thinking “Mag 7” likely should be bottoming and starting to push back to new highs

This research is for the clients of FS Insight only. FSI Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or FS Insight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FS Insight. At the time of publication of this report, FS Insight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FS Insight is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

FS Insight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of FS Insight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by FS Insight clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of FS Insight, which is available to select institutional clients that have engaged FS Insight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

FS Insight does not have the same conflicts that traditional sell-side research organizations have because FS Insight (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by FS Insight and/or affiliates of FS Insight. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of FS Insight.

This research is for the clients of FS Insight only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but FS Insight does not warrant its completeness or accuracy except with respect to any disclosures relative to FS Insight and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where FS Insight expressly agrees otherwise in writing, FS Insight is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fsinsight.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.