Last week, all eyes were on the inflation data. Headlines about CPI data, released Tuesday, refueled tariff-related worries from those already inclined to see them in the pipeline. Fundstrat Head of Research Tom Lee is still not one of them.

“I think inflation is falling like a rock underneath the noise that’s coming from tariffs,” he said. That’s not to say that tariffs won’t affect consumers, however. There is a likelihood that they will cause a one-time increase in prices. Nevertheless, “tariffs are actually a tax on companies,” and taxes typically do not cause inflation.

Although stocks pulled back after the CPI release, the hammering got a little quieter the next day when core PPI came in about as benign as it gets. As Lee noted, not only was it far lower than consensus expectations, it came in at “basically zero.” As a reminder, PPI measures wholesale inflation and thus is viewed as a leading indicator of CPI.

So to recap, consumer inflation is trending below expectations, while wholesale inflation is suggesting this will continue. Lee also notes that from July to October CPI readings will benefit from easier comparisons (relative to 2024). “Put together, these establish the conditions for a dovish Fed surprise in the second half of the year,” he said.

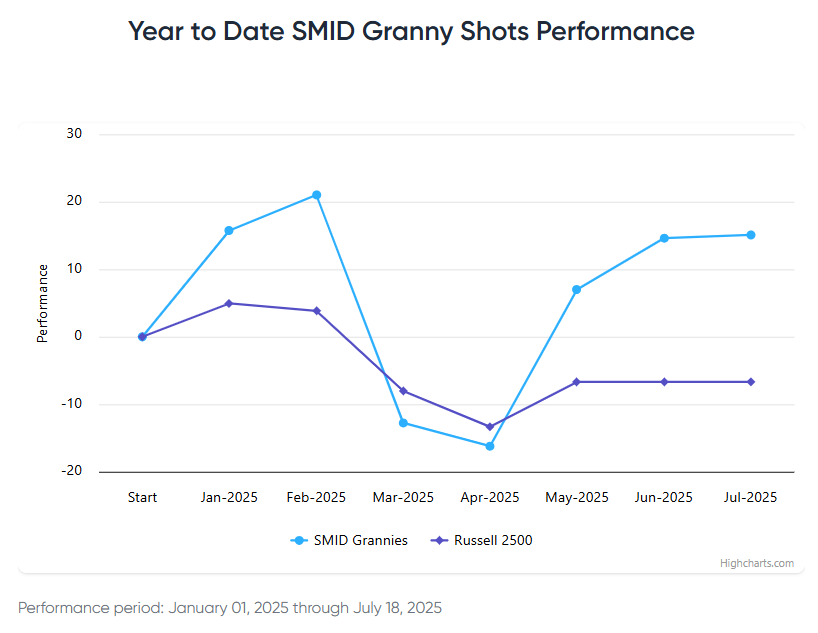

One likely beneficiary if that surprise materializes is small-caps, a sector Lee favors that has outperformed the broader S&P 500 for the past month or so. For Head of Technical Strategy Mark Newton, this move by small-caps is further evidence that the investment environment has changed. “The texture of the market has changed a bit in the last couple weeks versus what we saw back in April, May, June. We did see a nice broadening out in late June,” he told us at our weekly research huddle.

However, “something I’m watching,” Newton told us, “is the ratio of equal-weighted discretionary versus equal-weighted staples. If discretionary is outperforming strongly, that generally means the market is in pretty good shape. When it starts to roll over and staples start to outperform and discretionary, that’s when markets can start to lag.” So what does it look like now? “For right now, the ratio is still in good shape, trending up, and it looks like we’re going to push up into August,” he said. “Based on timing, it looks like we have about another three or four weeks of gains in this.”

Chart of the Week

To Fundstrat’s Tom Lee, the real story from last week’s macroeconomic data is that for the fifth straight month, “actual, delivered core CPI came in below consensus [as shown in our Chart of the Week]. That’s what I’d call a trend, right?” he asked rhetorically. The fact that core CPI readings are consistently coming in below expectations reinforces an observation Lee has been making for some time: “I think that fundamentally, there’s a lot of people who have inflation hammers and [thus] think everything is a nail.”

Big bipartisan wins for crypto in the US House today. GENIUS Act passes 307-122. Now goes to White House for Trump signature CLARITY Act passes 294-134. Now goes to the Senate

The one meaningful technical move I’m seeing today revolves around WTI Crude oil breaking its trend from early May more than two months ago. Today’s decline to multi-day lows does appear like a short-term negative unless erased by day’s end, and could drive prices down to test and break 6/24 lows at $64 in front month WTI Futures. I suspect that this should eventually happen, and lead WTI down to the high $50’s before a bottom. Key initial support under 64 lies at 60.83, and then 55.40 might seem extreme, but would represent a full 100% alternative wave projection to the initial decline from 6/23. Thus, i expect that Energy will prove to be a near-term laggard over the next two weeks, and XOP might fall to 121, OIH might reach 223, and XLE could fall to $83.75, or 82 before the start of 2H 2025 strength for WTI Crude and Energy. At present, unless immediately erased, today’s move is a short-term technical negative.

This research is for the clients of FS Insight only. FSI Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or FS Insight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FS Insight. At the time of publication of this report, FS Insight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FS Insight is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

FS Insight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of FS Insight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by FS Insight clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of FS Insight, which is available to select institutional clients that have engaged FS Insight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

FS Insight does not have the same conflicts that traditional sell-side research organizations have because FS Insight (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by FS Insight and/or affiliates of FS Insight. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of FS Insight.

This research is for the clients of FS Insight only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but FS Insight does not warrant its completeness or accuracy except with respect to any disclosures relative to FS Insight and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where FS Insight expressly agrees otherwise in writing, FS Insight is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fsinsight.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.

- these figures improved to 4.4% YoY from 5.0% last month

- Dem respondent dropped from 9.3% to 7.7% and is main reason

Suggets consumers not viewing tariffs as driving a sustained rise in inflation. Overall, a decent data point