The market carnage extended for a fourth straight week, dragged down by investors wrestling with a flip-flopping tariffs policy and intensifying recession fears. This week, the S&P 500 tumbled 2.3% and the Nasdaq Composite fell 2.4%. Both sharply rebounded Friday but failed to exit correction territory—defined as a drop of 10% or more from a recent high.

While there is pain, Fundstrat Head of Technical Strategy Mark Newton reminded investors that the declines are in line with what is historically noted during the first quarter of any new administration. Besides, it was a mere 17 trading days ago that the S&P 500 set a fresh all-time high, he pointed out.

“The economy arguably is still in very good shape, the earnings picture is good—even as fear levels are higher,” Newton said during the weekly huddle. “I don’t think we can jump to conclusions and talk ‘recession’ just based on these declines.”

Stocks’ “dire” situation is not shared by bonds, Head of Research Tom Lee said. Sure, Treasury Secretary Scott Bessent said that there is no Trump put for stocks, but “there may be one on the economy,” meaning that the White House could be forced to turn around its policies if it sees the economy deteriorate too much, Lee highlighted.

The bond market is also pricing in odds of 3.4 interest-rate cuts from the Federal Reserve this year, up from 1.5 previously, he said. The divergence between stocks and bonds has historically been a “pretty good entry point for stocks,” said Lee, citing data from Renaissance Macro Research.

On the technical side, Newton has been encouraged to see stocks down to the same levels of oversold territory as the ones that coincided with bottoms seen in August and April of 2024. “People are disgruntled, but we’re certainly not seeing evidence of true fear,” he said.

He expects that lows to this sell-off could be “achieved within the next two weeks from a timing perspective, and prices are nearing possible support.”

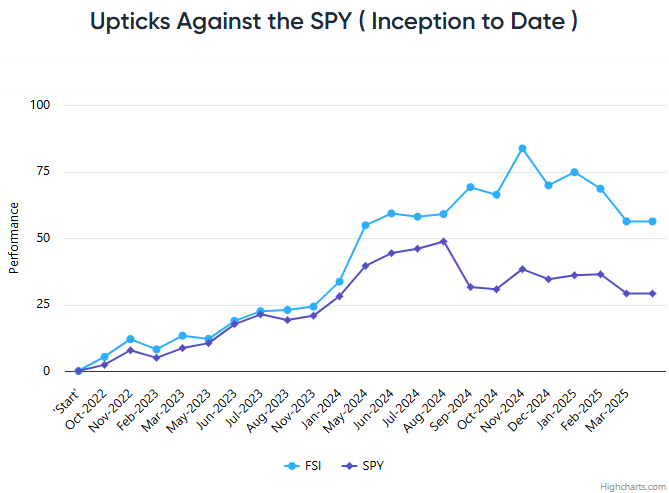

Chart of the Week

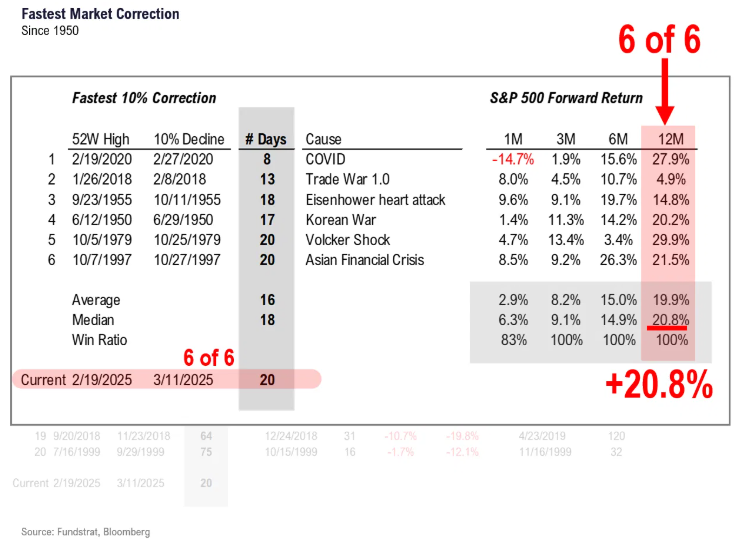

Putting the recent declines into perspective, Fundstrat Head of Research Tom Lee said that the 10% correction noted in the S&P 500 is the fifth-fastest in the past three quarters of a century, taking 20 days. The median gain from all prior declines was 21% over the next 12 months. The quickest was from the Covid decline, prompting Lee to say, “Is this worse than the global pandemic? I don’t think so.”

If one needed evidence that U Mich survey is polluted by political leanings, see the latest survey results of 1-yr inflation – Dems now +6.5% – Republicans +0.1% Feb Core CPI showed inflation tanking

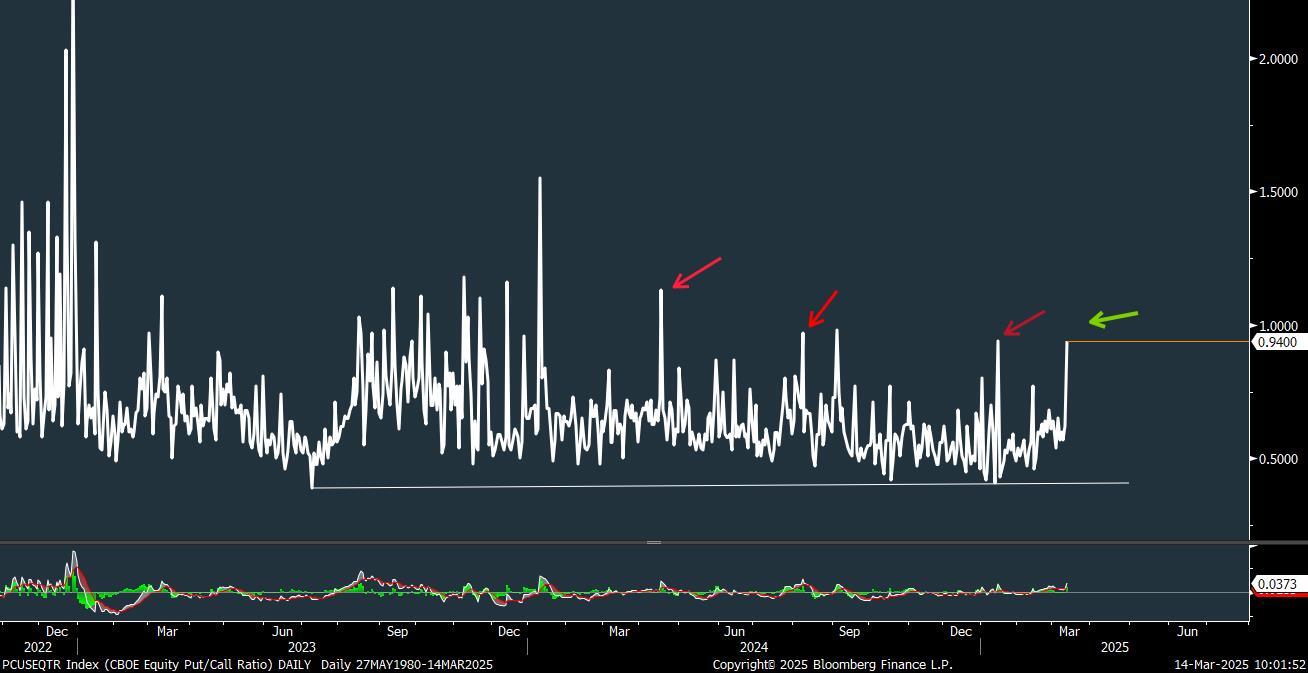

Last night’s data on Equity Put/call did in fact get back into the zone of fear, reaching 0.94, the highest reading since January. I had discussed last night that seeing a spike in Equity Put/call ratio was important in showing some evidence of capitulation which henceforth had been lacking despite the chronic bearishness. While the volume readings haven’t yet produced abnormally high readings on the downside via the TRIN, or Arms index, seeing nearly an Equal level of Put options being traded as Calls is an important piece of the sentiment puzzle that suggests that market lows are growing close.

This research is for the clients of FS Insight only. FSI Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or FS Insight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FS Insight. At the time of publication of this report, FS Insight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FS Insight is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

FS Insight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of FS Insight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by FS Insight clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of FS Insight, which is available to select institutional clients that have engaged FS Insight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

FS Insight does not have the same conflicts that traditional sell-side research organizations have because FS Insight (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by FS Insight and/or affiliates of FS Insight. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of FS Insight.

This research is for the clients of FS Insight only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but FS Insight does not warrant its completeness or accuracy except with respect to any disclosures relative to FS Insight and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where FS Insight expressly agrees otherwise in writing, FS Insight is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fsinsight.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.

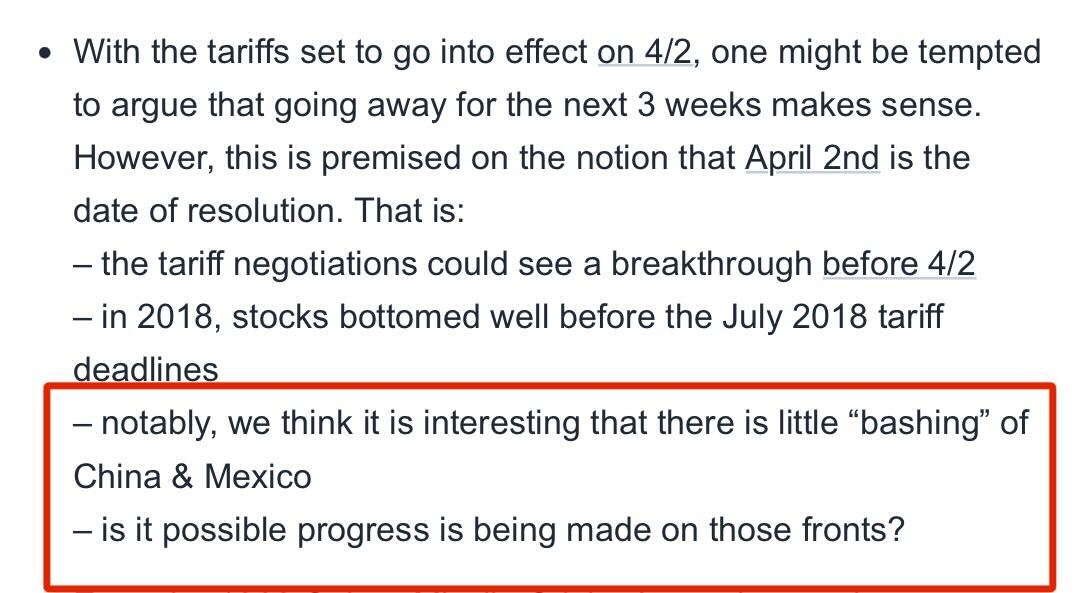

- I would put >50% probability that a deal with one of those 2 countries is announced within the next 2 weeks

This would end talk of “White House wants a recession” Stay the course