The Nasdaq Composite closed above 20,000 points for the first time on Wednesday, though it slipped slightly to end last week at just under the 20K mark. The rally has been driven by tech heavyweights such as Google, Tesla and Apple. However, the S&P 500 slipped into what Fundstrat Head of Research Tom Lee has called the “zone of uncertainty” this week, with the broad-based index dipping slightly after three consecutive weeks of gains.

As Lee had anticipated, investors responded to worries about inflation, particularly after CPI and PPI reports. Head of Technical Strategy Mark Newton noted that the CPI numbers showed “big progress” on two inflation components that have proven stubborn throughout 2024 – used cars and housing. However, the war against price increases continued to weigh on the broad-stock index. Worries about continued “stickiness” in inflation ramped up after Thursday’s PPI report showed hotter-than-expected wholesale-inflation numbers. (The PPI report is considered to be a precursor to consumer-inflation trends.)

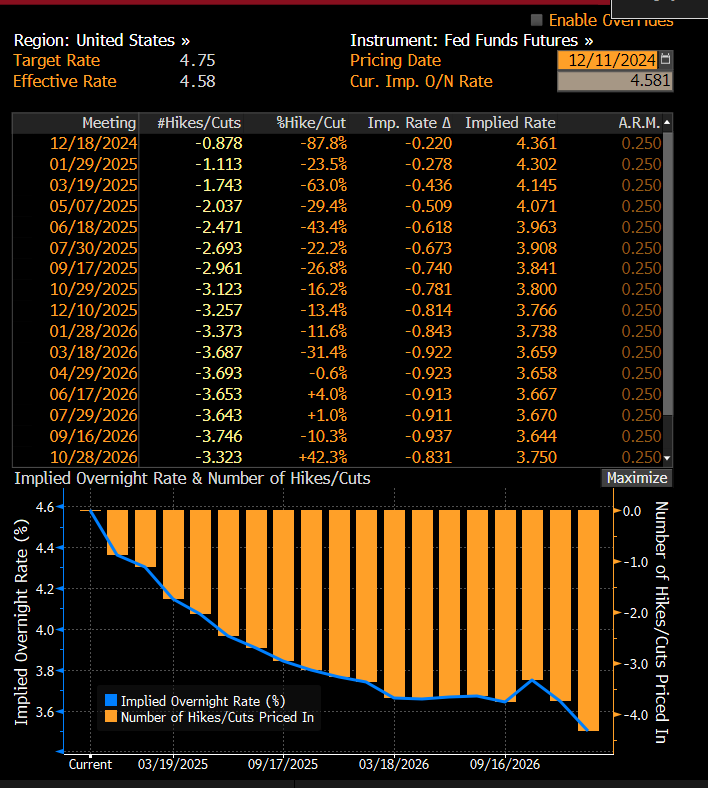

This in turn raised worries about prospects for further rate cuts from the Federal Reserve. While the market continues to anticipate that the Federal Open Market Committee (FOMC) will cut rates by 25 bps on December 18 (as implied by Fed Funds futures trading), it also largely anticipates that the Fed will then pause its cutting cycle on January 29, 2025. (Fed Funds futures trading implied odds of a January pause at 81.0% as of Friday afternoon.)

For those worried that inflation will return, Lee has this to say: “I think a lot of people are making the mistake of seeing inflation as something that has an on-off switch. Inflation is probably going to have a second wave, but it’s not actually a spike or a resurgence. It’s more that we overshot to the downside and so it’s bouncing. I’d call it more of an echo.” In other words, Lee continues to see inflation tanking and declining.

The market’s reaction to the PPI numbers had Newton telling us that “backing and filling is possible next week ahead of the FOMC meeting,” but his work nevertheless shows that “the bull market rally looks back underway.” Furthermore, his examination into trends in the equal-weighted S&P 500 (RSP) has him optimistic about “small-caps, Transports, and the DJIA all pushing back to new highs into the end of the year.” That’s consistent with Lee’s base-case constructive scenario for the rest of the December.

Chart of the Week

Fundstrat Head of Research Tom Lee presented his highly anticipated2025 Market Outlook last week, taking viewers through all the reasons why markets could continue to climb until the end of 2025. Importantly, however, Lee does not see the all sectors of the market rising in unison. Nor, as illustrated in our Chart of the Week, does he see the advance continuing in a straight line.

AVGO 24.44% strong 20% gains are causing some outsized strength in the Semiconductor sector, despite Technology overall being lower today. SOX(Philadelphia Semiconductor sector) is up 2% but as can be seen, price has rallied to multi-day highs but remains at a key level of trendline resistance which will need to be exceeded before expecting a larger bounce out of this sub-sector which has been trending largely sideways since July. As can be seen on this daily SOX chart, the early strength failed right at 5185 and this is an important area for the Semis which when exceeded, would suggest a larger upside rally for this group. This would be further helpful to Technology which has already shown some good outperformance since the beginning of December.

CPI comes in in-line at +0.3% MoM, and 2.7% YoY causing a bit of a pop in US Equity futures and pullback in 2yr yields. largely keeps the Fed’s CUT plans intact as Swap market shows an 86% chance of a 25bp Cut. However, this is the largest print in 7 mths, but nonetheless, a largely expected result for today. Used cars only moderately higher, and Owners Equivalent rent at 0.2% is half of last month, so some progress on inflation in housing. and big progress on both of these

IWM -0.81% has now closed down from its opening price on nine of the last 10 trading sessions, down for 5 of the last 7 trading days, yet has merely given up 50% of the rally from mid-November. Thus, while it has weakened at a time of Large-cap Tech strength, i view the recent consolidation as being pretty benign and not all that meaningful. TD indicators show IWM to be one day away from generating a TD buy setup, and my expectation is the the maximum amount of downside happens to 233.6 before this starts to turn back higher. Overall, tomorrow’s CPI print very well could prove to be the catalyst for the low to this minor pullback in US Equities that’s occurred, and from an absolute basis, IWM is getting to a very attractive area of support which should occur this week.

This research is for the clients of FS Insight only. FSI Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or FS Insight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FS Insight. At the time of publication of this report, FS Insight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FS Insight is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

FS Insight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of FS Insight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by FS Insight clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of FS Insight, which is available to select institutional clients that have engaged FS Insight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

FS Insight does not have the same conflicts that traditional sell-side research organizations have because FS Insight (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by FS Insight and/or affiliates of FS Insight. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of FS Insight.

This research is for the clients of FS Insight only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but FS Insight does not warrant its completeness or accuracy except with respect to any disclosures relative to FS Insight and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where FS Insight expressly agrees otherwise in writing, FS Insight is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fsinsight.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.