With the outcome of the election emerging far more quickly and more definitively than many expected, markets proceeded to surge. Indeed, the major indices – the S&P 500, Nasdaq, Dow, and last but not least, the small-cap Russell 2000 – recorded their best weeks of the year. As Head of Technical Strategy Mark Newton noted, “We saw a historic move in small caps on Wednesday, getting our long-awaited breakout in IWMabove the key 227 level. It was the largest move after an election for small caps that we’ve seen since the inception of Russell 2000 in 1978. The second-largest, by the way, was in 2016, the day after Trump was elected the first time.”

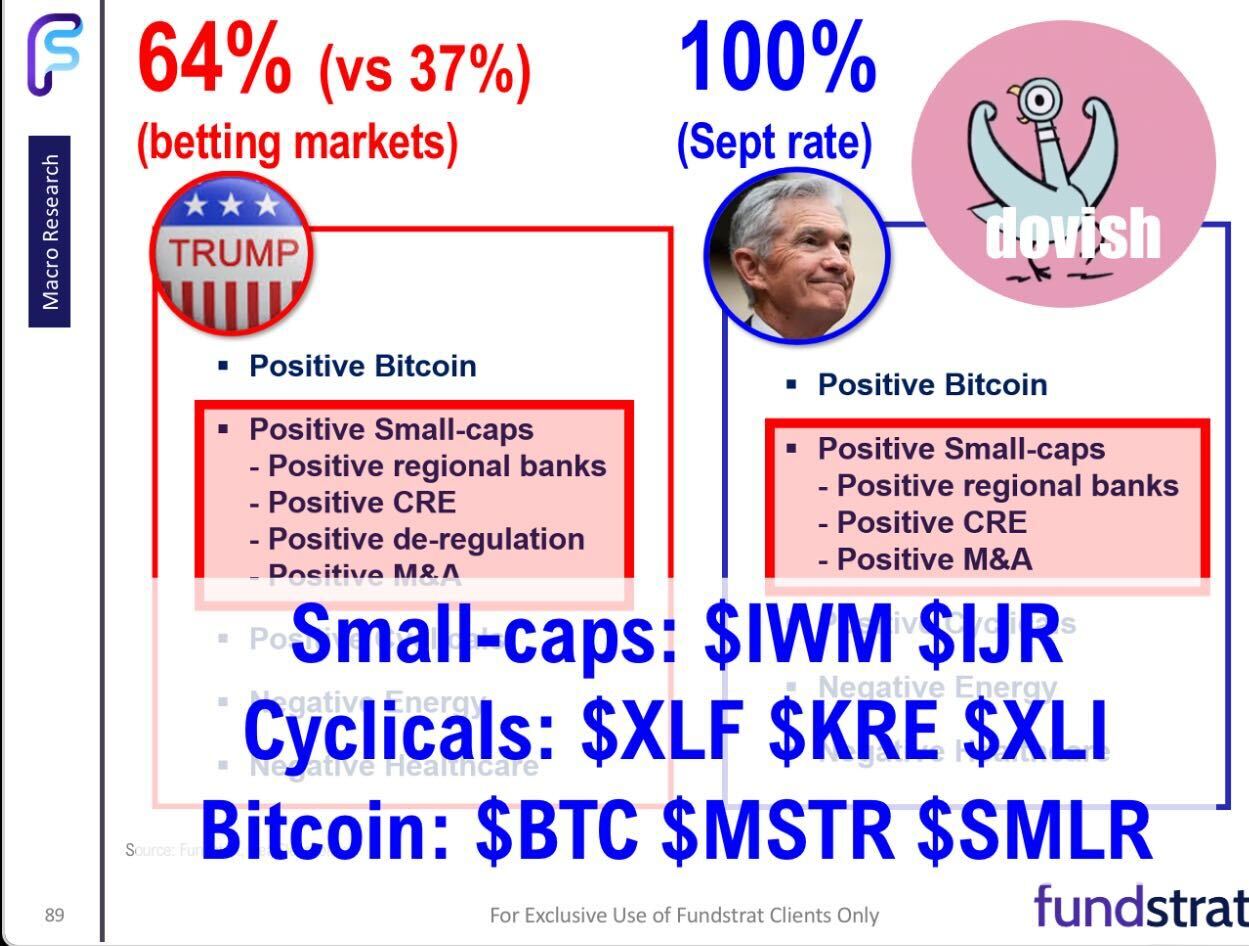

Ahead of the election, Fundstrat Head of Research Tom Lee noted that he expected stocks to do well into the end of the year regardless of which candidate emerged on top. However, with Donald Trump quickly claiming victory, the election uncertainty that has affected markets for the past eight weeks quickly dissipated. As he has written before, “the trades for a dovish Fed and the trades for a Trump victory are the same: small-caps, Bitcoin, Financials, and Industrials.

The Federal Open Market Committee also met last week, voting to lower the target rate by another 25 bp to 4.5% – 4.75%, as widely anticipated. Federal Reserve Chair Jerome Powell told reporters afterwards that “we have gained confidence that [inflation is] on a sustainable path down to 2%.” He also affirmed that “in the near term, the election will have no effect on our policy decisions” given the time it will take for the new administration and Congress to decide on economic policy changes and the time it will take for data about the impact of those decisions to emerge. For Lee, the most important takeaway was that “even though inflation reports recently were slightly ‘hotter’ than expected, and regardless of election results, the Fed is committed to cutting rates. Overall,” he concluded, “this was a dovish meeting and it reinforces the tailwinds for equities into year-end, with Fed cuts boosting the economy.”

The post-election rally was marked in particular by strength not just in small caps, but meaningful advances in Financials and Technology. For Newton, the move in Transports was perhaps just as important. “Transports finally broke out to new all time highs after about three years of going sideways,” he said at our weekly huddle. “To me, that’s a fairly important development that’s going to positively influence the Industrials. For Dow theory purists, it’s a very big positive to see for Dow Theory purists to see Transports finally join the Industrials, to join the Utilities, back at new highs, and it’s a comforting thing for overall market structure.”

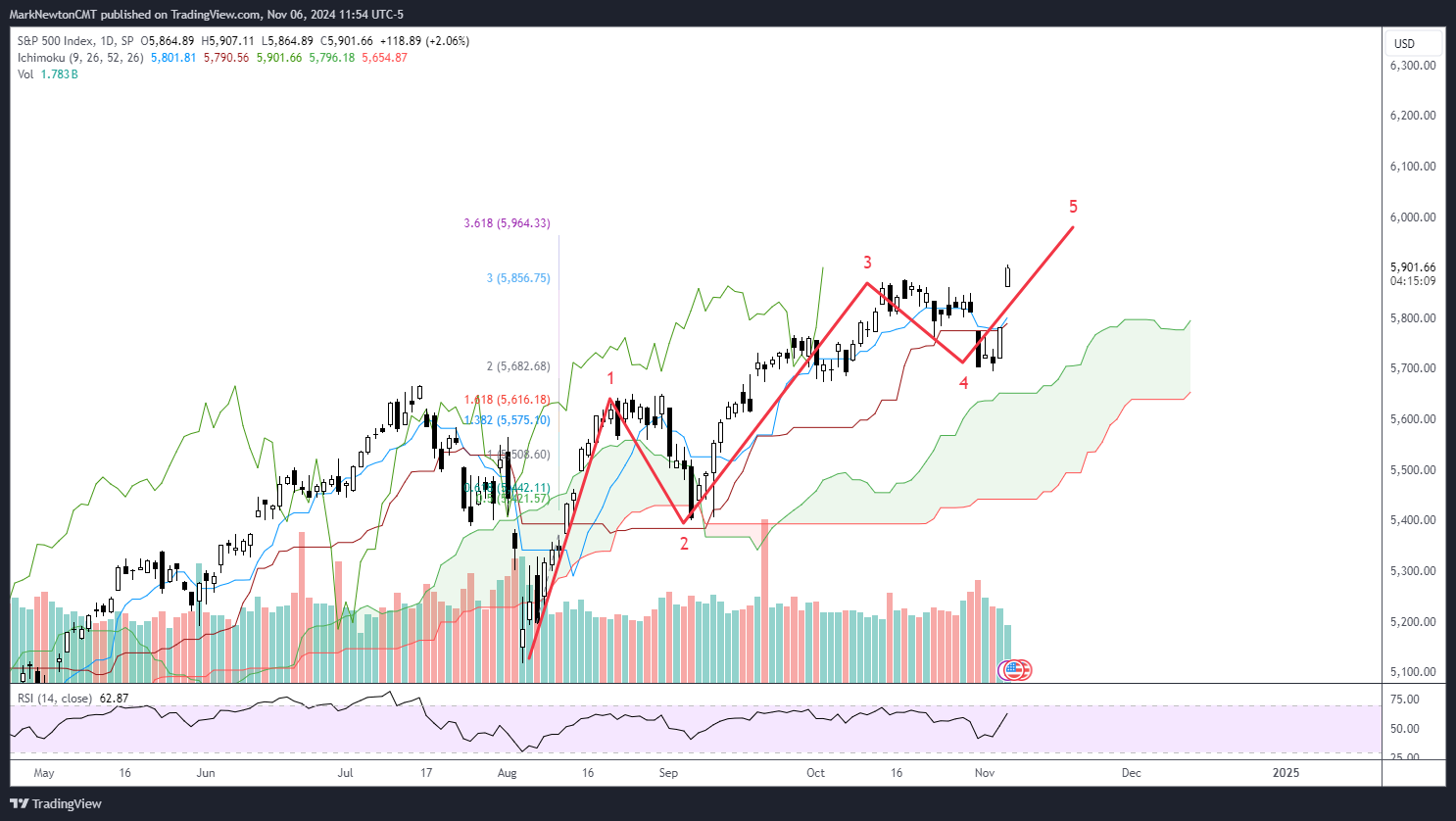

Newton has some near-term concerns however. “The post-election activity was overall a very healthy move, but in my view, the S&P 500 has now gotten a little bit stretched on this breakout.” Expanding on that, he noted that though the larger index numbers showed strength, “I have some issues about breadth. There’s a lot of stocks – about a third of the S&P – that did not participate on [last week’s] rally. I’d want to see that improve, and that would really help me to gain conviction.” The bottom line for Newton: “My thinking is that we’re obviously still running up in the short term. I think that probably continues for another three to five days for those who are tactical, and then I expect we’ll probably see some weakness or consolidation in the back half of November.“

Chart of the Week

With the election cycle over, “I think it’s now time to focus on how to position between now and year end,” Fundstrat Head of Research Tom Lee told us. As he has previously written, those areas and sectors most likely to benefit from a Trump victory coincide with those that he has been flagging as benefiting from the Fed moving further into the rate-cut cycle. “These are also what worked after Trump won in 2016,” he noted, and this is shown in our Chart of the Week.

Today’s gap back to new all-time highs is a technical positive for risk assets, as the Trump win has led Cryptocurrencies, Small-caps, and Transportation stocks to all make constructive breakouts. Market breadth is a bit less than desired, at only 3/2 positive, but the movement in Financials, Industrials, Technology are indeed quite constructive in the short run. ^SPX 0.43% likely could have resistance from 5950-6000 on this rise, and as this chart shows, it looks like the fifth wave from August is underway. While this has bullish implications, it also likely will require consolidation before being able to push up into and through November and into year-end. I’m still of the opinion that the back half of November could be down, so important to watch market breadth carefully and what participates on any additional rally post FOMC.

TSLA 4.11% broke out of the same triangle as many indices and ETF’s today. Exceeding 271 helped this to reach the highest levels since early 2023 and suggests a move up to 300-2 initially then 314-5 before some consolidation. Great structural move and very heavy volume today, not dissimilar from its July breakout. 314 is important as it’s a 100% alternative projection of the April-July rally from the August lows. The fact that TSLA closed near its highs of the day following the opening gap is also constructive for the days ahead.

This research is for the clients of FS Insight only. FSI Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or FS Insight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FS Insight. At the time of publication of this report, FS Insight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FS Insight is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

FS Insight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of FS Insight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by FS Insight clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of FS Insight, which is available to select institutional clients that have engaged FS Insight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

FS Insight does not have the same conflicts that traditional sell-side research organizations have because FS Insight (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by FS Insight and/or affiliates of FS Insight. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of FS Insight.

This research is for the clients of FS Insight only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but FS Insight does not warrant its completeness or accuracy except with respect to any disclosures relative to FS Insight and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where FS Insight expressly agrees otherwise in writing, FS Insight is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fsinsight.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.

- small caps IWM 1.98%

- financials and industrials KRE 2.86% XLF 1.22% XLI 1.29%

- bitcoin BTC SMLR -4.18% MSTR 7.81%

Today’s open validates these views. Stick with them. Add if you have not added exposure.