A daily market update from FS Insight — what you need to know ahead of opening bell.

“There’s an ancient tension between wanting to savor the world as it is and wanting to improve on the world as given.” — Leon Kass

Overnight

Trump halts enforcement of antibribery law WSJ

Trump removes director of government ethics office CNBC

Japan investment in US hits record levels in shift away from China SEM

Trump says no exemptions with metal tariffs to start in March BBC

EU says AI race ‘far from over’ as bloc pledges 50-billion-euro investment boost CNBC

Canada vows swift retaliation to ‘unjustified’ Trump tariffs BBC

Elon Musk reportedly offers $97.4B for OpenAI, Sam Altman says ‘no thank you’ YF

BYD shares hit record high after EV maker rolls out driver assistance tech with DeepSeek’s AI help CNBC

McDonald’s U.S. Sales Drop as Customers Spend Less WSJ

Coca-Cola sales easily top estimates as global demand rises CNBC

Southwest Airlines names Tom Doxey as CFO RTR

Hamas delays planned hostage handover to Israel amid ceasefire dispute SEM

Man pleads guilty to role in SEC social media account hack that led the price of bitcoin to spike AP

Japan ministry worker loses sensitive files during night of drinking BBC

Chart of the Day

| Overnight |

| S&P Futures -22

point(s) (-0.4%

) Overnight range: -26 to -2 point(s) |

| APAC |

| Nikkei flat Topix flat China SHCOMP -0.12% Hang Seng -1.06% Korea +0.71% Singapore -0.37% Australia +0.01% India -1.32% Taiwan +0.57% |

| Europe |

| Stoxx 50 +0.11%

Stoxx 600 -0.05% FTSE 100 -0.02% DAX +0.11% CAC 40 +0.09% Italy +0.06% IBEX +0.02% |

| FX |

| Dollar Index (DXY) -0.01%

to 108.31 EUR/USD +0.09% to 1.0316 GBP/USD -0.06% to 1.236 USD/JPY +0.07% to 152.1 USD/CNY +0.03% to 7.3072 USD/CNH +0.0% to 7.3111 USD/CHF +0.08% to 0.912 USD/CAD +0.18% to 1.4342 AUD/USD -0.03% to 0.6275 |

| Crypto |

| BTC +0.66%

to 98046.06 ETH +1.46% to 2703.68 XRP +2.52% to 2.4897 Cardano +13.52% to 0.7969 Solana +1.35% to 202.91 Avalanche +3.15% to 26.49 Dogecoin +4.33% to 0.2653 Chainlink +3.98% to 19.43 |

| Commodities and Others |

| VIX +1.39%

to 16.03 WTI Crude +1.24% to 73.22 Brent Crude +1.29% to 76.85 Nat Gas +1.71% to 3.5 RBOB Gas +1.21% to 2.13 Heating Oil +0.89% to 2.473 Gold -0.16% to 2903.75 Silver -1.03% to 31.72 Copper -1.99% to 4.614 |

| US Treasuries |

| 1M -1.1bps

to 4.3177% 3M -2.0bps to 4.3123% 6M -4.8bps to 4.2846% 12M -1.9bps to 4.2107% 2Y +0.2bps to 4.277% 5Y +1.8bps to 4.3557% 7Y +2.4bps to 4.4406% 10Y +2.4bps to 4.5211% 20Y +3.2bps to 4.7908% 30Y +3.2bps to 4.7389% |

| UST Term Structure |

| 2Y-3

M Spread narrowed 0.6bps to -6.9

bps 10Y-2 Y Spread widened 2.4bps to 24.2 bps 30Y-10 Y Spread widened 0.6bps to 21.4 bps |

| Yesterday's Recap |

| SPX +0.67%

SPX Eq Wt +0.28% NASDAQ 100 +1.24% NASDAQ Comp +0.98% Russell Midcap +0.3% R2k +0.36% R1k Value +0.25% R1k Growth +0.98% R2k Value +0.24% R2k Growth +0.47% FANG+ +1.52% Semis +1.89% Software +1.7% Biotech -0.99% Regional Banks -1.16% SPX GICS1 Sorted: Energy +2.15% Tech +1.45% Utes +1.07% Indu +0.91% Cons Staples +0.78% SPX +0.67% Comm Srvcs +0.58% Materials +0.52% Cons Disc +0.5% REITs +0.19% Healthcare -0.06% Fin -0.79% |

| USD HY OaS |

| All Sectors -0.6bp

to 301bp All Sectors ex-Energy -0.4bp to 287bp Cons Disc +1.8bp to 241bp Indu -1.4bp to 224bp Tech -2.4bp to 306bp Comm Srvcs -1.1bp to 500bp Materials -1.0bp to 271bp Energy -3.1bp to 290bp Fin Snr -2.4bp to 261bp Fin Sub +0.3bp to 208bp Cons Staples +1.2bp to 282bp Healthcare +0.6bp to 352bp Utes +0.2bp to 226bp * |

| Date | Time | Description | Estimate | Last |

|---|---|---|---|---|

| 2/11 | 6AM | Jan Small Biz Optimisum | 104.7 | 105.1 |

| 2/12 | 8:30AM | Jan CPI m/m | 0.3 | 0.4 |

| 2/12 | 8:30AM | Jan Core CPI m/m | 0.3 | 0.2 |

| 2/12 | 8:30AM | Jan CPI y/y | 2.9 | 2.9 |

| 2/12 | 8:30AM | Jan Core CPI y/y | 3.1 | 3.2 |

| 2/13 | 8:30AM | Jan PPI m/m | 0.3 | 0.2 |

| 2/13 | 8:30AM | Jan Core PPI m/m | 0.3 | 0.0 |

| 2/14 | 8:30AM | Jan Import Price m/m | 0.4 | 0.1 |

| 2/14 | 8:30AM | Jan Retail Sales m/m | -0.2 | 0.4 |

MORNING INSIGHT

Good morning!

The buy the dip regime remains intact and we expect Wed’s Jan CPI to quell inflation worries.

Click HERE for more.

TECHNICAL

- SPX and QQQ have pushed back up to challenge triangle resistance highs.

- Copper breakout last week occurred during a time of very bullish seasonality.

- Copper cycles indicate a tactical rally likely until Spring 2025, then a likely reversal.

Click HERE for more.

CRYPTO

The lack of a market reaction to new steel and aluminum tariff announcements might mean the market is finally in the clear regarding tariff-driven volatility.

Click HERE for more.

First News

A soaring U.S. dollar is putting a collar around tech titans.

Amazon.com said in its fourth-quarter earnings report that its first-quarter guidance forecasts a $2.1 billion headwind from foreign exchange rates. Microsoft reported a lower-than-expected revenue forecast, partly because of the dollar. Apple warned investors that it expects foreign exchange to be a headwind and to have a negative impact on revenue of about 2.5 percentage points on a year-over-year basis. Google-parent Alphabet said it expects a larger crimp to its topline from the strengthening of the dollar in the first quarter compared to three months ago.

The greenback is the world’s go-to currency for trade and many transactions, so when it increases in value, it reduces the value of goods purchased in nondollar currencies.

The DXY Dollar Index, which measures the strength of the dollar against a basket of foreign currencies, has added 2.6% over the past three months, boosted by President Donald Trump’s threat of tariffs and hopes of cutting down excess government spending.

Trump is making good on both those promises so far, which could help the dollar extend its yearslong climb higher. Over the weekend, fresh tariffs were announced on all steel and aluminum imports.

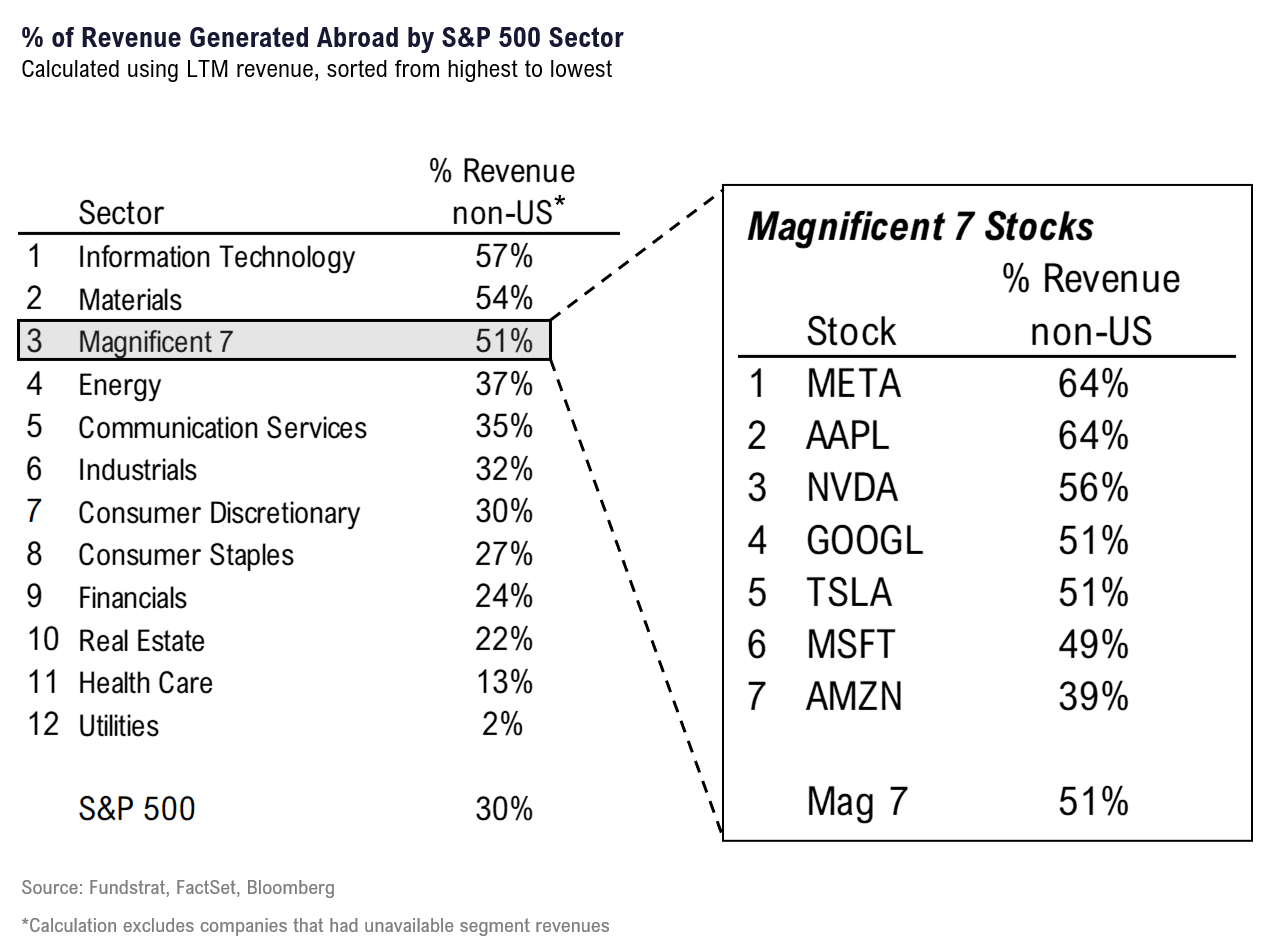

Tech stocks, in particular, are vulnerable to what the dollar does because the S&P 500’s information technology sector generates 60% of its revenue abroad, the largest majority out of the 11 sectors, according to our data team’s analysis. In comparison, the broad-based S&P 500 index earns roughly 30% of its sales outside the U.S.

Here’s how it works: Typically, tariffs propel American companies to increase their domestic manufacturing capabilities and potentially even create more jobs but not without a strong dollar. Without a strong dollar, tariffs only raise the price of imported goods. (On the other hand, when the dollar is strong compared with another currency, it becomes more expensive for customers abroad to buy U.S. products.)

A stronger dollar could drag out the tech sector’s bad start to the year. Excluding Nvidia, the Magnificent Seven, as a group, posted no positive sales surprise for the first time since 2022, according to a CNBC article citing Goldman Sachs’ David Kostin.

No one is immune to fluctuations in the value of the almighty dollar – not even the supreme tech stocks.