Equity trends show no evidence of wavering. February managed to finish with gains greater than 5% on the heels of three prior months of gains, and this winter rally still shows very little signs of “letting up” as more and more sectors have begun to show participation. Following new monthly all-time high closes in S&P’s Equal-weighted S&P 500 (RSP 0.25% ) as well as the NASDAQ Composite to join SPX, QQQ, and DJIA, further gains look possible into mid-March ahead of possible minor consolidation. Outside of US indices, it’s proper to note that Europe’s STOXX 600 index has hit new all-time highs along with Australia’s ASX, India’s BSE Sensex, along with the Japanese NIKKEI 225, which finally managed to claw back to new all-time highs after peaking out nearly 35 years ago in 1989.

(No change in commentary over these next few paragraphs from earlier this week )

Equity markets remain in a sweet-spot right now as February has come to a close having shown no real evidence of weakness that traditionally is possible in Februarys of Election years.

Trends remain upward sloping on short and longer-term timeframes. Momentum is positively sloped and while overbought on daily and monthly basis, has not really begun to diverge meaningfully. Technically strong sectors like Technology have been joined by strength in Healthcare, Industrials and Financials while this week’s above-average gains have been seen in other sectors like Consumer Discretionary and Materials.

While I’m on the lookout for evidence of DeMark based exhaustion and/or sector deterioration that might prove problematic, at present, we’re seeing the opposite, and the cyclical weakness possibility for mid-February has come and gone and SPX, QQQ and DJIA are all now pushing back higher along with cryptocurrencies.

While the US Dollar and US Treasury yields have largely moved sideways over the past few weeks, this has not proven detrimental to the US Equity market. I suspect that a rally might be possible for both the US Dollar and Yields sometime in March which could take these both back to new monthly highs, despite a lack of Treasury supply until 3/11/24. (Note: Friday’s soft ISM number did cause a Treasury rally with yields pulling back to multi-day lows. However, this doesn’t look technically significant, and broader two-month trends are still positive and could lead yields higher throughout March.)

Below is a weekly chart of the NIKKEI 225, which deserves more attention than S&P’s move back to new all-time highs, as this index just hit new all-time highs last week for the first time in over 34 years.

Further gains look likely in NKY following this move to new all-time highs, and similar to commentary on SPX following its own push to all-time highs, such a development rarely coincides with an appropriate time to lighten up, purely based on technical reasons.

EWJ at approximately $70, (MSCI Japan Index fund) should push higher to test 2021 peaks near $74 without much trouble. While I do not expect USDJPY to move over 152 in the next few months, and should begin to turn back down, any move back above 152 would argue that DXJ (WisdomTree Japan Hedged Equity Fund) might prove to be a more timely choice than EWJ, as it hedges out its Japanese Yen exposure.

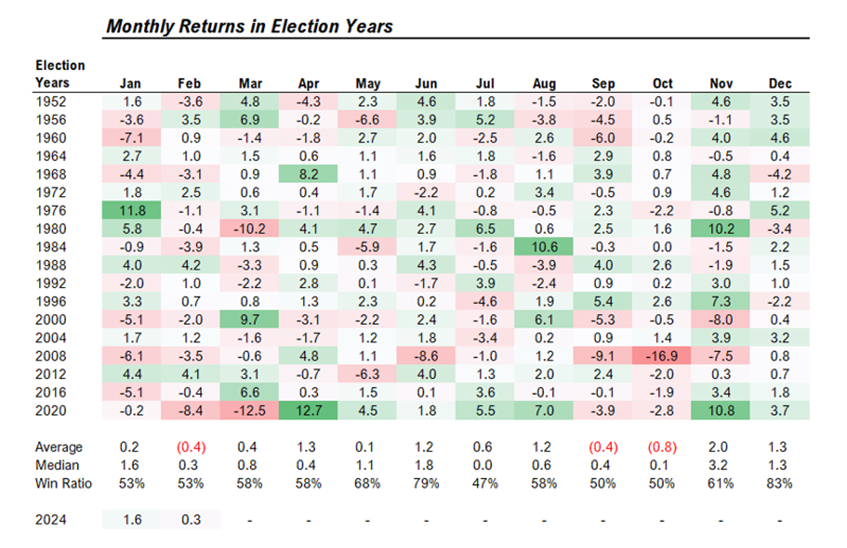

How does March typically unfold in Election years?

While my attention to DeMark exhaustion indicators following SPX’s push up to all-time highs would be suggestive of a rally into mid-March, the average seasonality trends seem to argue the opposite in Election years.

Specifically, prices normally tend to peak in the first week and trend lower into mid-month before pushing up into April.

As discussed earlier, more evidence of near-term trend failure is warranted before growing too antsy in selling into this parabolic equity rally. However, if this traditional pattern of seasonality for Election year March shows up this year, then a possible minor peak might be possible next week in SPX which would result in fractional consolidation only before a push higher into April.

Given that the larger cycle composite seems to favor a bottom in the month of May, some type of peak would likely seem plausible in March and/or in early April. At this time, there’s not enough to go on to suggest that the graph below becomes reality. However, it’s worth showing given that the front half of March has normally proven to be worse than the second half.

March tends to be a lot better than February most Election years

While February of 2024 wildly outperformed normal election year tendencies, it’s worth just showing this seasonality chart of Election years to illustrate that March can often be much better than the average February.

Following four straight months of gains, a seasonal slide could be possible at some point between March and May. However, I’m not willing to bet on it just yet. For now, it’s still right to expect higher gains in March, as this has proven to be the 6th best year in performance in Election years.

When stripping out the anomaly of March 2020 due to COVID-19, this would certainly put much better odds in March’s corner.

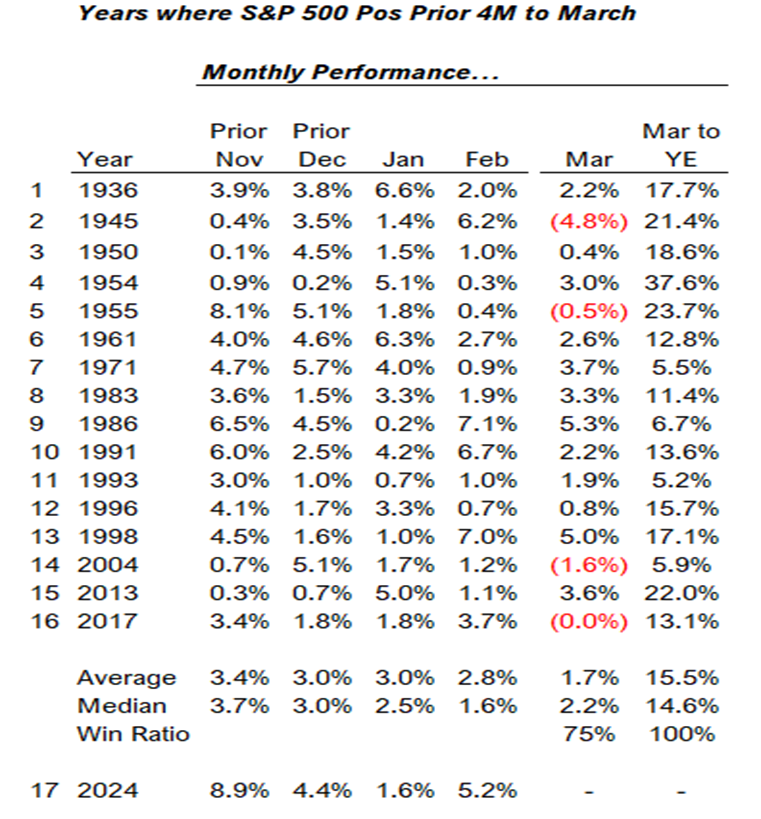

Four straight months of gains during the Winter months has had a perfect track record for full year performance for SPX

Don’t look now, but SPX has managed to turn out four straight months of gains following last October’s 2023 market bottom. November, December, January and February have all been positive, a feat that’s only happened on 16 prior occasions over the last 90 years.

Interestingly enough, each time this has happened, the entire year has shown positive returns, for a perfect record of 16-0.

Moreover, the average return from March until year-end has averaged 15.5% with a median return of +14.6%.

March’s average return in those 16 years where the prior four months showed consecutive gains was also +2.2%, much higher than the average +0.4% and median return of +0.8%.

Overall, given this undefeated record of gains, I feel that 2024 could prove to be a stellar year. Furthermore, my SPX-5175 target will have to be raised at some point this year, as SPX finished less than 1% away from my entire 2024 year-end target.

At present, the key takeaway here is that “Momentum usually begets more momentum”, and as the popular saying goes, “The trend is your friend until it ends”. While an intra-year pullback is normal and even likely, 2024 should prove to be a positive year, and recent gains and momentum seem to back that up. Happy Friday.