We publish on a 3-day a week schedule:

– SKIP MONDAY <– Traveling

– SKIP TUESDAY

– Wednesday

– SKIP THURSDAY

– Friday

______________________________________________________________

We discuss: It’s been a data heavy week, but the big news is ECB yesterday and it’s dovish impact on bond markets.

Please click below to view today’s Macro Minute (Duration: 5:36).

______________________________________________________________

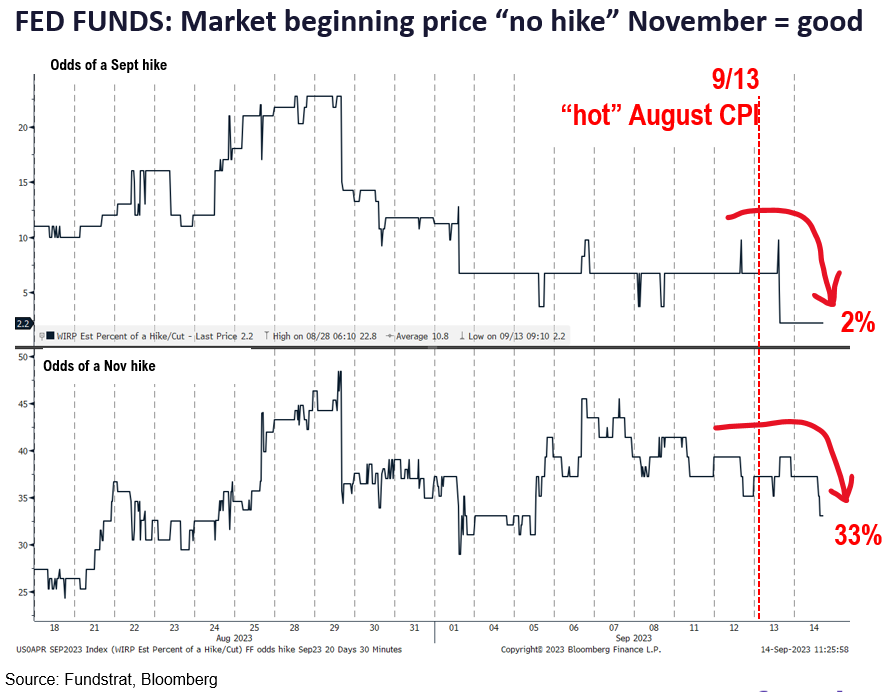

The Federal Reserve FOMC will announce its September interest rate decision on 9/20 at 2:00pm ET. The August PPI, released yesterday, is last key “hard data” point and futures markets have now priced in a mere 2% probability of a hike in September. And the odds of a November hike have tanked recently to 33% from 48% a few weeks ago. And as we have written multiple times over the past few months, we believe these odds eventually fall to 0% and that the July hike is the last hike of the cycle. To me, this is the most important development in the next few months and also the cornerstone for why we see equities rallying into year-end.

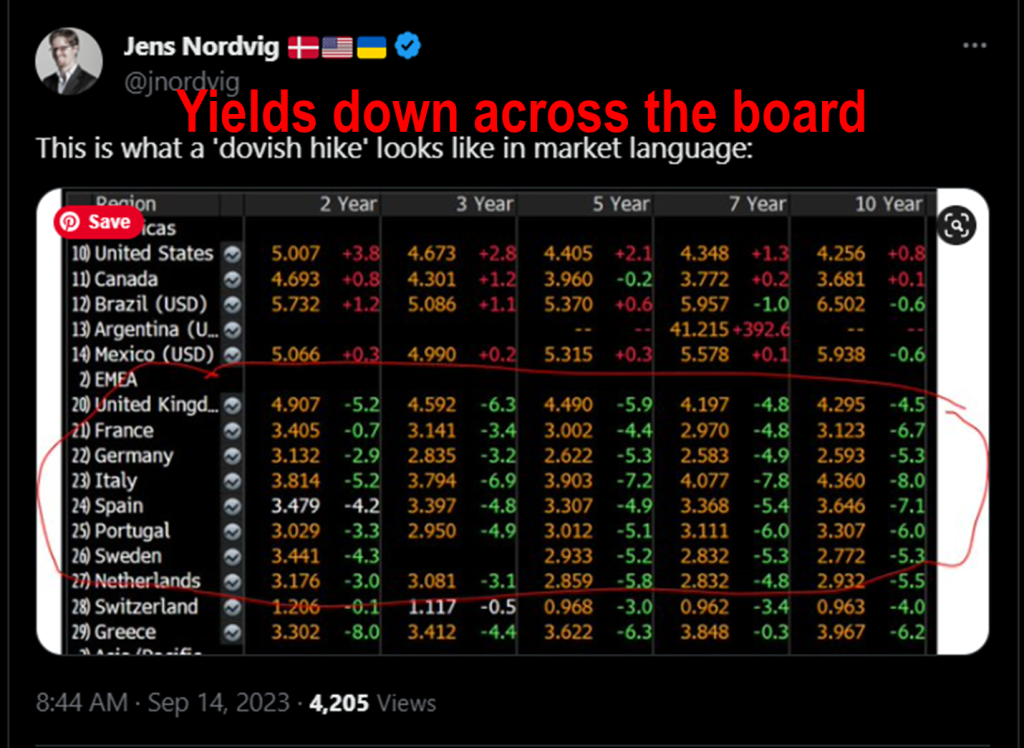

- Yesterday, the ECB raised interest rates by +25bp, its 10th consecutive hike, to 4% and the ECB President suggested this could be the last hike. The reaction is immediate in markets as the future hikes were quickly repriced away and yields throughout the Euro area fell and triggered a large risk rally. Fed funds futures also repriced meaningfully yesterday, aided by the ECB and by the August PPI. And the odds of a Sept and Nov hike are at multi-week lows (see above).

- To me, the market reaction to ECB is a prelude to how markets will react when the Fed eventually reaches that same point. The point when the incoming data (“data dependent Fed”) will convince the Fed to no longer see the need for further hikes. On that day, we expect multiple markets to reprice:

– long-term yields likely fall

– interest rates across the board adjust as markets start to believe “cuts” are possible

– 30-yr mortgage rates fall by 150bp or more, as the excess spread disappears - In all, yesterday’s ECB and the market’s reaction is a harbinger of the 1982 moment ahead for the S&P 500. We have written previously about this, but the key takeaway is equities went to an all-time high 17 trading days after Volcker publicly considered “ending the inflation war” (NY Times 1982).

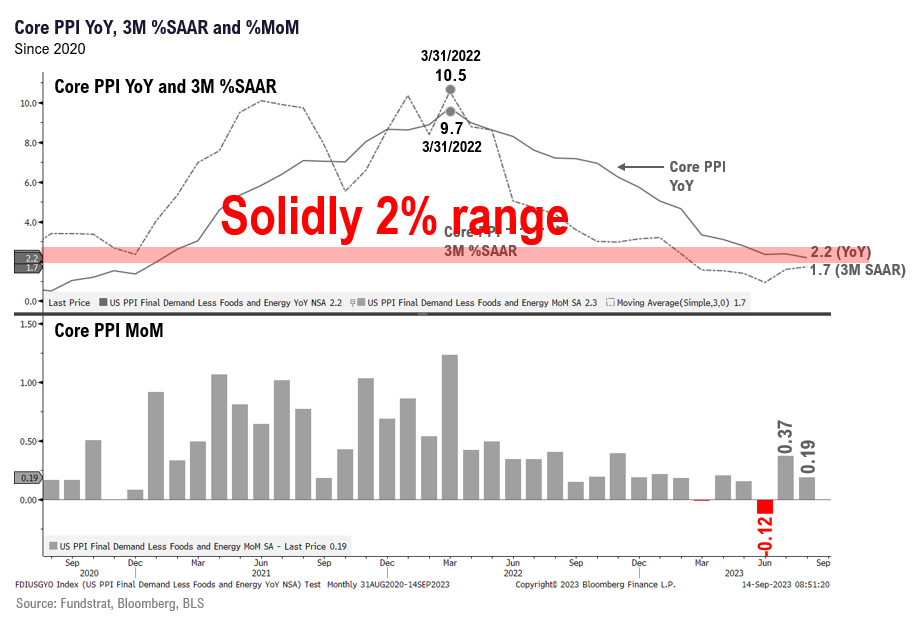

- Yesterday’s August PPI was inline and core (ex-Energy and ex-Food) is still running a very very good 2% YoY range. So, inflationary pressures for producers have been very stable at below 2%. That is bolstering our view that CPI will stay muted as well. After all, producers/corporates pay worker salaries. And with elevated wage gains, PPI is still below 2%. Think about that.

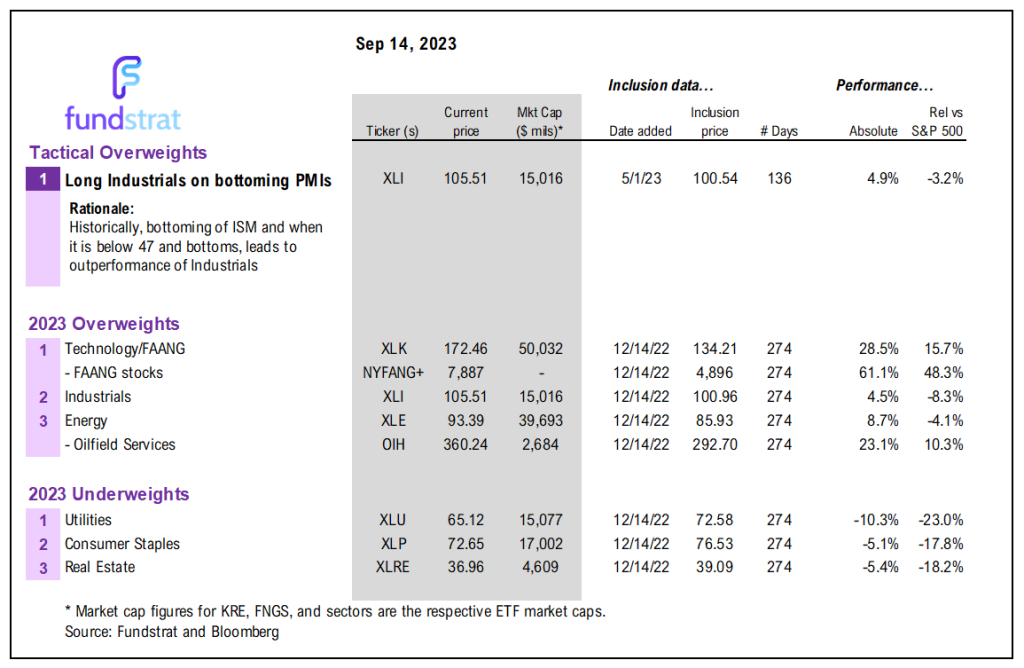

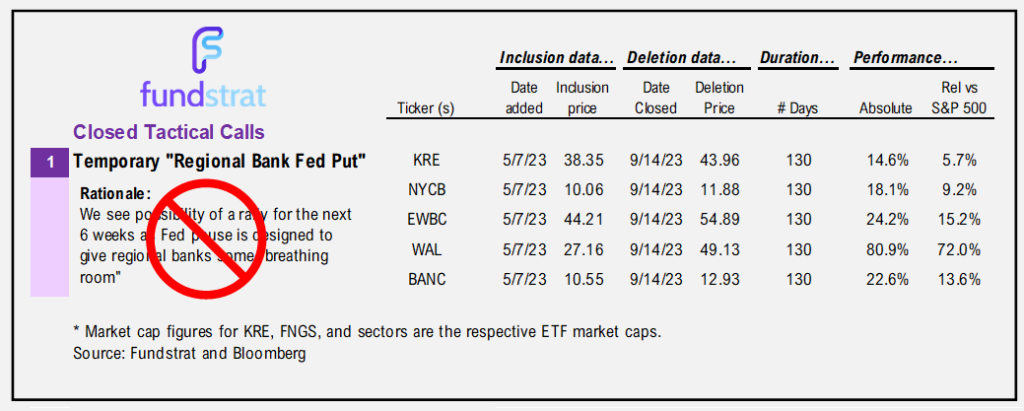

BOTTOM LINE: Our base case is Sept softness is “front loaded” and rally into month-end. Ending Regional Bank OW.

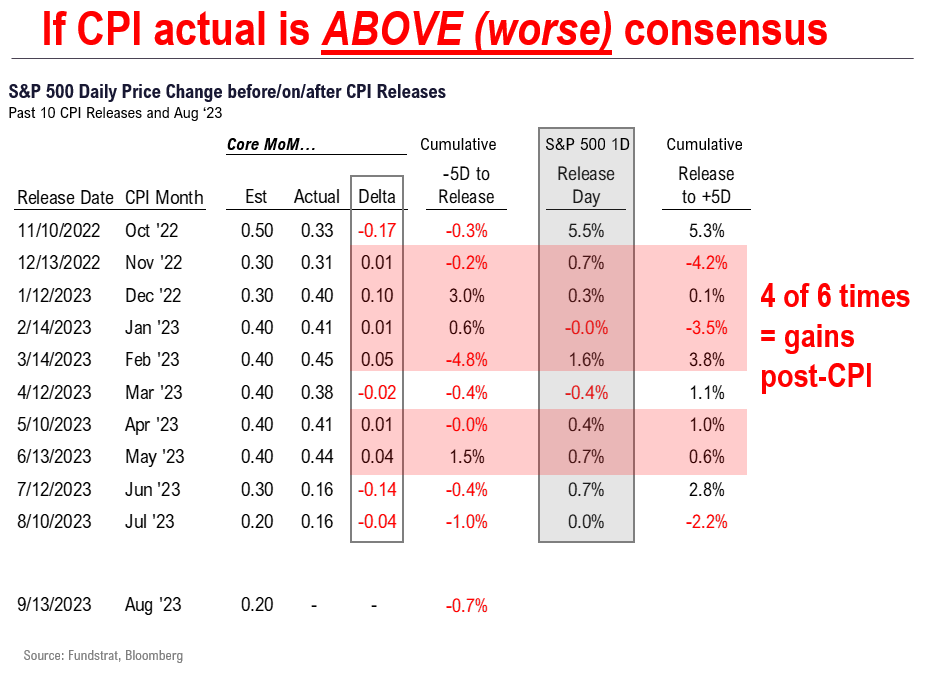

Since the end of July, equity markets have again become a “game of inches” and frustrating. Our base case is that September weakness is front-loaded and that the overall tone of markets should improve into month-end and the possibility of a rally of 2%-3% from Sept 4th onwards. Equity markets are tracking to this view and even the relatively positive follow through on the “hot CPI” report this past week is a sign of that.

- We are removing our Tactical OW of Regional Banks today. The KRE has been consolidating the past few weeks and we think it is prudent to become more selective. Since our OW:

– KRE has risen 15% from 5/7 to now

– S&P 500 SPY is up 9%

– NYCB EWBC WAL BANC all gained 19% to 81% as well

– the outperformance is >570bp and we think it is prudent to take profits - The equity put-call ratio surged to closing high of 1.2 yesterday, the 3rd such elevated reading in 6 months. And we flagged a week ago, a 1.2 or greater reading has seen equity lows within 1-2 days. This strengthens our view that equity markets likely drift higher into month end.

- UAW strike was last night, so investors likely want to see how stocks react today. But we take the view this will be a nothing burger.

- We stay Cyclical and like

- Technology/FAANG XLK

- Industrials XLI

- Energy XLE OIH XOP

Key incoming data September

9/1 8:30am ET August Jobs ReportTame9/1 10am ET August ISM ManufacturingTame9/6 10am ET August ISM ServicesMixed9/6 2pm ET Fed releases Beige BookTame9/8 9am ET Manheim Used Vehicle Index August FinalTame9/8 2Q23 Fed Flow of Funds ReportTame-

9/13 8:30am ET August CPIMixed -

9/14 8:30am ET August PPITame - 9/15 8:30am ET September Empire Manufacturing Survey

- 9/15 10am ET U. Mich. September prelim 1-yr inflation

- 9/18 8:30am ET September New York Fed Business Activity Survey

- 9/18 10am ET September NAHB Housing Market Index

- 9/19 9am ET Manheim September Mid-Month Used Vehicle Value Index

- 9/20 2pm ET September FOMC rates decision

- 9/21 8:30am ET September Philly Fed Business Outlook Survey

- 9/22 9:45am ET S&P Global PMI September Prelim

- 9/25 10:30am ET Dallas Fed September Manufacturing Activity Survey

- 9/26 9am ET July S&P CoreLogic CS home price

- 9/26 10am ET September Conference Board Consumer Confidence

Key incoming data August

8/1 10am ET July ISM ManufacturingTame8/1 10am ET JOLTS Job Openings JunTame8/2 8:15am ADP National Employment ReportHot8/3 10am ET July ISM ServicesTame8/4 8:30am ET July Jobs reportTame8/7 11am ET Manheim Used Vehicle Index July FinalTame8/10 8:30am ET July CPITame8/11 8:30am ET July PPITame8/11 10am ET U. Mich. July prelim 1-yr inflationTame8/11 Atlanta Fed Wage Tracker JulyTame8/15 8:30am ET Aug Empire Manufacturing SurveyMixed8/15 10am ET Aug NAHB Housing Market IndexTame8/16 8:30am ET Aug New York Fed Business Activity SurveyNeutral8/16 2pm ET FOMC MinutesMixed8/17 8:30am ET Aug Philly Fed Business Outlook SurveyPositive8/17 Manheim Aug Mid-Month Used Vehicle Value IndexTame8/23 9:45am ET S&P Global PMI Aug PrelimWeak8/25 10am ET Aug Final U Mich 1-yr inflationMixed8/28 10:30am ET Dallas Fed Aug Manufacturing Activity SurveyTame8/29 9am ET June S&P CoreLogic CS home priceTame8/29 10am ET Aug Conference Board Consumer ConfidenceTame8/29 10 am ET Jul JOLTSTame8/31 8:30am ET July PCETame- 9/1 8:30am ET August NFP jobs report

- 9/1 10am ET August ISM Manufacturing

Key incoming data July

7/3 10am ET June ISM ManufacturingTame7/6 8:15am ADP National Employment ReportHot7/6 10am ET June ISM ServicesTame7/6 10 am ET May JOLTSTame7/7 8:30am ET June Jobs reportMixed7/10 11am ET Manheim Used Vehicle Index June FinalTame7/12 8:30am ET June CPITame7/13 8:30am ET June PPITame7/13 Atlanta Fed Wage Tracker JuneTame7/14 10am ET U. Mich. June prelim 1-yr inflationMixed7/17 8:30am July Empire Manufacturing Survey7/18 8:30am July New York Fed Business Activity Survey7/18 10am July NAHB Housing Market Indexin-line7/18 Manheim July Mid-Month Used Vehicle Value IndexTame7/25 9am ET May S&P CoreLogic CS home priceTame7/25 10am ET July Conference Board Consumer ConfidenceTame7/26 2pm ET July FOMC rates decisionTame7/28 8:30am ET June PCETame7/28 8:30am ET 2Q ECI Employment Cost IndexTame7/28 10am ET July Final U Mich 1-yr inflationTame

Key data from June

6/1 10am ET May ISM ManufacturingTame6/2 8:30am ET May Jobs reportTame6/5 10am ET May ISM ServicesTame6/7 Manheim Used Vehicle Value Index MayTame6/9 Atlanta Fed Wage Tracker AprilTame6/13 8:30am ET May CPITame6/14 8:30am ET May PPITame6/14 2pm ET April FOMC rates decisionTame6/16 10am ET U. Mich. May prelim 1-yr inflationTame6/27 9am ET April S&P CoreLogic CS home priceTame6/27 10am ET June Conference Board Consumer ConfidenceTame6/30 8:30am ET May PCETame6/30 10am ET June Final U Mich 1-yr inflationTame

Key data from May

5/1 10am ET April ISM Manufacturing (PMIs turn up)Positive inflection5/2 10am ET Mar JOLTSSofter than consensus5/3 10am ET April ISM ServicesTame5/3 2pm Fed May FOMC rates decisionDovish5/5 8:30am ET April Jobs reportTame5/5 Manheim Used Vehicle Value Index AprilTame5/8 2pm ET April 2023 Senior Loan Officer Opinion SurveyBetter than feared5/10 8:30am ET April CPITame5/11 8:30am ET April PPITame5/12 10am ET U. Mich. April prelim 1-yr inflationTame5/12 Atlanta Fed Wage Tracker AprilTame5/24 2pm ET May FOMC minutesDovish5/26 8:30am ET PCE AprilTame5/26 10am ET U. Mich. April final 1-yr inflationTame5/31 10am ET JOLTS April job openings

_____________________________

35 Granny Shot Ideas: We performed our quarterly rebalance on 7/18. Full stock list here –> Click here

______________________________

PS: if you are enjoying our service and its evidence-based approach, please leave us a positive 5-star review on Google reviews —> Click here.