Although the S&P 500 closed down 1.28% and the Nasdaq slipped 1.09% this week, Fundstrat Head of Research Tom Lee reiterated his call that any pullbacks are likely to be shallow, as we remain in what he describes as one of the “most-hated V-shaped rallies” in his experience. Last week’s renewed hostilities in the Middle East might have raised some investors’ anxieties, but the actual impact on the market was arguably minimal. As Lee noted, VIX rose to elevated levels, but with a peak around 22 (as of Friday close it was just under 21), these were levels we also saw in late May. “And late-May was hardly a time to be de-risking,” he noted.

Investors were arguably more focused this week on the press conference that followed the conclusion of the Federal Open Market Committee (FOMC) meeting on Wednesday. The Federal Reserve left rates unchanged, as widely anticipated, but Fed Chair Jerome Powell’s responses to a question about inflation expectations apparently spooked investors. “Everyone that I know is forecasting a meaningful increase in inflation in coming months from tariffs because someone has to pay for the tariffs,” Powell said. “It will be someone in that chain that I mentioned, between the manufacturer, the exporter, the importer, the retailer, ultimately somebody putting it into a good of some kind or just the consumer buying it.”

Lee understands the alarm. To him, the response signaled “a change in the Fed’s view from data dependence to forward-looking,” and based on multiple follow-up questions, other reporters also appeared to interpret Powell’s answer in this manner. Arguably, so did investors. “Ultimately [investors] are saying this doesn’t make much sense,” Lee said. “The Fed is essentially finding more reasons not to cut and look at long-term rates,” which largely weakened this week, including ahead of the FOMC meeting.

Still, Head of Technical Strategy Mark Newton saw a bright note in the FOMC meeting. “The biggest positive following the FOMC meeting is that the traders’ outlook for rate cuts now aligns with what the FOMC said,” he noted, pointing out that when there is a disparity between market and Fed expectations on rates, “there can be some jitters in the market.” Two cuts now appear likely by year-end, and as he noted, this has triggered some bullish steepening in the yield curve and improved sentiment around risk.

The week’s declines did not do any technical damage to the overall pattern, in Newton’s view. “In general, we are setting up for a classic ‘ABC’ type of corrective pattern” that ultimately “could give way to a move back to new all-time highs,” but “not anytime soon.” The possibility exists for an impending move back up to around the 6,100 level, Newton acknowledged, but that would likely be followed by a stallout or pullback. Thus, Newton used words like “choppy” and “grind” to describe his expectation for markets over the next month or so. For those with a focus on the longer term, however, “I do think it’s right to be still positive.”

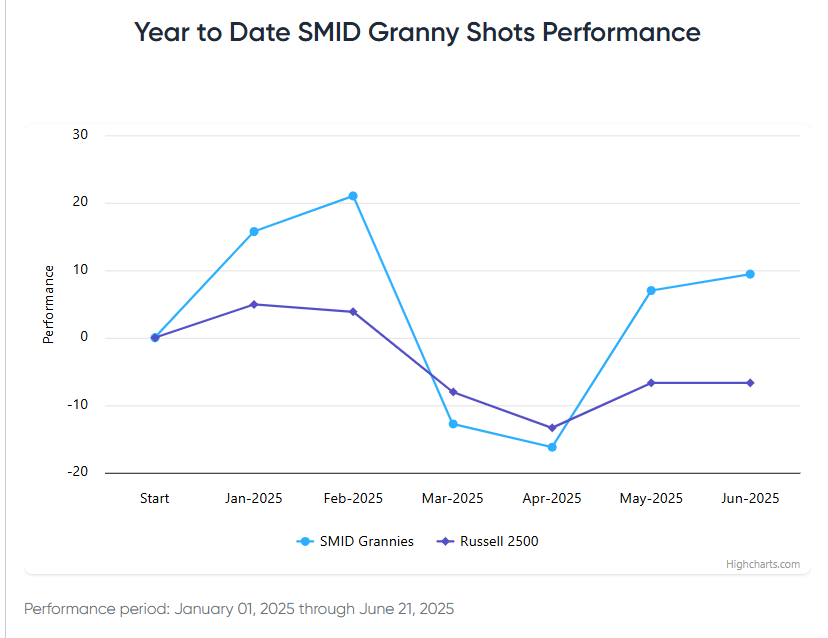

Chart of the Week

Although wars have very real and serious human consequences, they tend to have little long-term impact on equity markets. For this reason, Fundstrat’s Tom Lee said, We expect any dips to be bought, especially as we know that many investors are not even exposed to stocks at the moment.” This underweighting in equities is supported by a look at hedge funds’ net-positioning in the S&P 500, as shown in our Chart of the Week.

President Trump revealed US attacked nuclear sites in Iran Regarding war, the adage is “sell the build up, buy the invasion.” This means markets are worried as war fears mount and signs loom. But once the US takes action, investors are already de-risked This allows stocks and risk assets to gain once the action happens. Bitcoin was down over the past week on these concerns. We view this as a proxy for what will happen to equities this coming week https://truthsocial.com/@realDonaldTrump/114724035571020048

TSLA 0.06% has shown a bit of consolidation in the last week following its steep runup since early June, but its seen as a technical positive that the stock has been able to recoup roughly 61.8% of its decline from late May in just about one-week’s time. In my view, it’s more likely that this recent consolidation should be resolved by a push higher which should be confirmed on a move over $332. This would allow for a move to $349, but one can’t rule out a test of late May peaks near $371. Thereafter i anticipate some consolidation in July ahead of the start of a larger rally. Overall, TSLA’s weekly and monthly momentum (based on MACD) are positive, while daily is still negative. However i expect that the stock should have a much better 2nd half of 2025 than first, as Self-autonomous driving, Robotaxi news and Occulus starts to ramp up as expected.

Chair Powell’s press conference focused on two themes: uncertainty largely caused by tariff policy and the Committee’s view that the Fed is in a good place to deal with the uncertainty. My guess this is not what the White House wanted to hear. Chair Powell stayed clear of any comments on views expressed by President Trump.

This research is for the clients of FS Insight only. FSI Subscription entitles the subscriber to 1 user, research cannot be shared or redistributed. For additional information, please contact your sales representative or FS Insight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FS Insight. At the time of publication of this report, FS Insight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FS Insight is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.

FS Insight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of FS Insight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by FS Insight clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute the research of FS Insight, which is available to select institutional clients that have engaged FS Insight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.

FS Insight does not have the same conflicts that traditional sell-side research organizations have because FS Insight (1) does not conduct any investment banking activities, and (2) does not manage any investment funds.

This communication is issued by FS Insight and/or affiliates of FS Insight. This is not a personal recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment products or other financial instruments or services. This material is distributed for general informational and educational purposes only and is not intended to constitute legal, tax, accounting or investment advice.

The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Intended for recipient only and not for further distribution without the consent of FS Insight.

This research is for the clients of FS Insight only. Additional information is available upon request. Information has been obtained from sources believed to be reliable, but FS Insight does not warrant its completeness or accuracy except with respect to any disclosures relative to FS Insight and the analyst’s involvement (if any) with any of the subject companies of the research. All pricing is as of the market close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, risk tolerance, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies. The recipient of this report must make its own independent decision regarding any securities or financial instruments mentioned herein. Except in circumstances where FS Insight expressly agrees otherwise in writing, FS Insight is not acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of 1934. All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client website, fsinsight.com. Not all research content is redistributed to our clients or made available to third-party aggregators or the media. Please contact your sales representative if you would like to receive any of our research publications.