Equities Stage Partial Recovery With Likelihood of Rally Into Thanksgiving Array ( [cookie] => 51e6f3-f91aef-486fbc-ca0275-c6ee8e [current_usage] => 1 [max_usage] => 2 [current_usage_crypto] => 1 [max_usage_crypto] => 2 [lock] => [message] => [error] => [active_member] => 0 [subscriber] => 0 [role] => [visitor_id] => 198617 [user_id] => [reason] => Usage under limits [method] => ) 1 and can accesss 1

Our Views

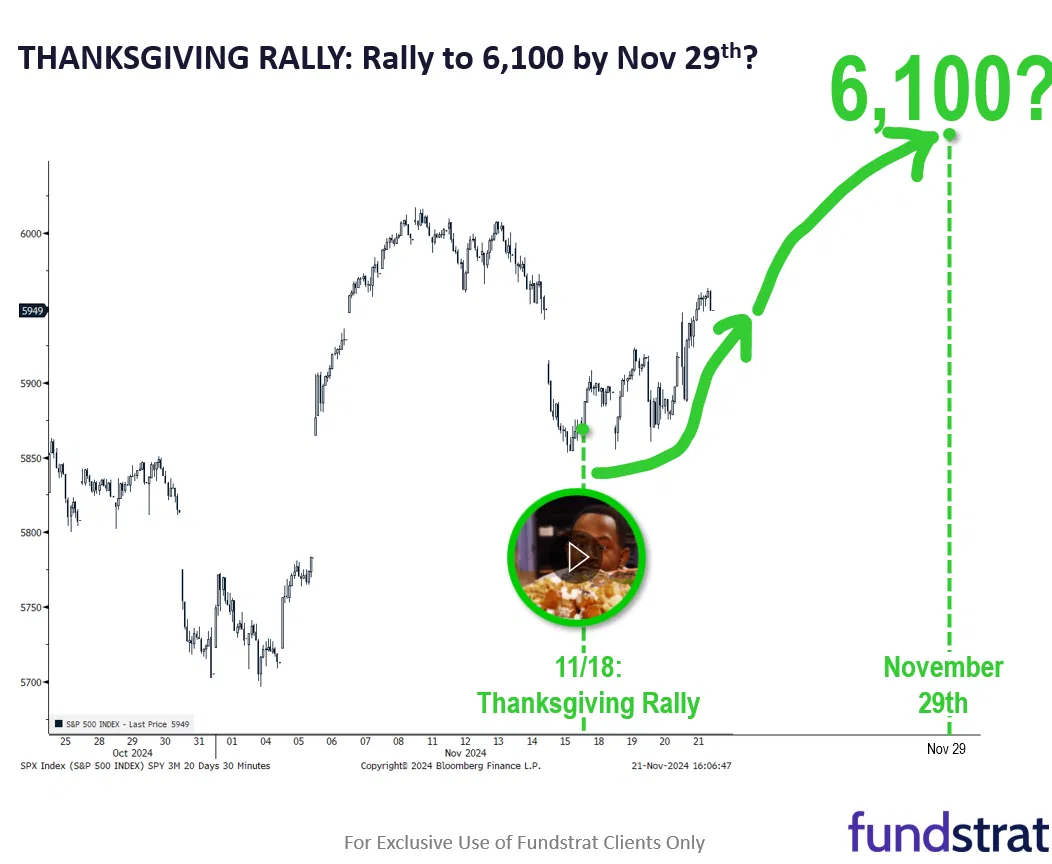

- Equities have modestly recovered this week, rising +1.68% (+4.13% for small-caps IWM -0.44% ). In our view, the case for a “Thanksgiving rally” remains intact (rally thru 11/29), and we potentially see the S&P 500 reaching 6,100.

- As we noted at the start of this week, we saw several drivers for this “Thanksgiving rally”: the “Trump put” on the markets (a Treasury Sec. announcement would remove “uncertainty”); a “Fed put” (even if a Fed that is “slowing cuts” is still dovish in our view); and markets pulling back to technical support (per Newton)

- Nvidia closing higher Thursday in the face of extremely high expectations for their earnings report is a positive outcome, in our view, and its outlook reinforces our view that the AI demand story remains intact. Nvidia trading up suggests there is still more upside for Nvidia’s share price near term.

- We still see room for sentiment to rise. In our view, when sentiment reaches a “bullish extreme” is when we see equities priced to “perfection.” Based on Goldman Sachs prime brokerage data, FINRA margin debt, and AAII’s net-bull percentage, we are not at that point yet.

- Bottom line: Stay on target into year-end.

- Equity trends from August remain bullish, but lower than recent peaks seen around 11/11/24. Tuesday’s stabilization is suggestive of a bounce in US Equities between now and next week’s Thanksgiving holiday.

- Treasuries also seem to be turning higher, and it’s thought that both Treasury yields and the U.S. Dollar might retreat into December following the unraveling of the so-called “Trump trade.”

- If/when Technology cannot mount any larger rally into next week, then markets might show further consolidation into early to mid-December; this would line up with cycle projections and recent lackluster breadth.

- At present, a rally seems to be underway into early next week and needs to be watched carefully for evidence of structure and broad-based participation (or lack thereof).

- Short-term correlations with major equity indices have broken down over the past couple of weeks, with BTC showing resilience despite the minor pullback in broader risk assets.

- We attribute this decoupling to a combination of (1) strong corporate demand and (2) favorable regulatory tailwinds.

- With Solana reaching a new ATH and on-chain activity remaining robust, the “Casino Stack” trade still offers incremental upside.

- For those initiating positions now, JTO stands out as the best risk/reward play in the basket, provided macro conditions and on-chain trends continue to support the broader Solana ecosystem.

- Core Strategy: Corporate buying and strong regulatory/political tailwinds bridged us through a choppy time for risk assets. Our current base case is that these tailwinds extend through inauguration day. We remain overweight on SOL with and still like altcoins such as BNB, HNT, JTO, BONK, RAY, STX, and CORE, emphasizing assets with high SOL and (potential) BTC beta.

- President Trump continues to put forth nominees for key posts in his upcoming administration, notably with Rep. Matt Gaetz (R-Florida) withdrawing from consideration for Attorney General and Trump putting forth Pam Bondi in his place.

- Trump continues to interview candidates for the position of Treasury Secretary, with four prospects – all with strong backgrounds in finance – widely rumored in the press to be in consideration.

- Congress will be on Thanksgiving break next week, but a government-shutdown deadline on December 20 is coming up, and Republicans are currently uncertain how they would like to handle it.

Wall Street Debrief — Weekly Roundup

Key Takeaways

- The S&P 500 rose 1.68% this week to close at 5,969.34. The Nasdaq ended the week at 19,003.65, up 1.73% for week. Bitcoin was at $99,057.38 on Friday afternoon, rising about 10.3% from Monday levels.

- All eyes were on Nvidia's quarterly results this week, and Fundstrat Head of Research Tom Lee said the report showed that "the AI demand story remains intact."

- Lee and Head of Technical Strategy Mark Newton each see signs that markets could rally into Thanksgiving.

"Ultimately it is not the stock market nor even the companies themselves that determine an investor's fate. It is the investor." – Peter Lynch

Good evening,

Stocks recovered partially from a rather unpleasant previous week. It was a light week for macroeconomic data, which arguably resulted in even greater focus on Nvidia's earnings report, released after market close on Wednesday (November 20). Although expectations were high, the chipmaker easily beat both top- and bottom-line estimates. Yet, Nvidia shares moved higher only slightly the next day, but Fundstrat Head of Research Tom Lee nevertheless viewed this as a good sign – both for the company and for markets in general.

Lee interpreted Nvidia's report positively, noting that the company's outlook "reinforces our view that the AI demand story remains intact. In this context, Nvidia trading up slightly post-earnings suggests there is still more upside for Nvidia’s share price near term." Perhaps just as importantly, "the release of the earnings is likely to clear some of the uncertainty that has been acting as a headwind for markets as a whole."

Yet from his technical perspective, Head of Technical Strategy Mark Newton expressed near-term concern about the reaction to Nvidia's results and forward guidance. "NVDA -1.23% was set to move up 8% potentially after its earnings report, but it has been pretty much range-bound," he pointed out. This is meaningful for equity investors, because in his view, "as Nvidia goes, so goes the market." As Newton reminded us, "Nvidia is now the largest stock within the S&P 500, so it's important to keep track of where Nvidia is going at all times," even for those who don't have a stake in the company.

"The key level for Nvidia is going to be 137," Newton said. To him, "a move under 137 means we're likely to have a stock market correction in the weeks to come, possibly to the tune of about 5%. Now that's not happening yet, and it might not," he reassured us. "But it is something to keep an eye on." In the immediate term, Newton noted that his work "seems to show the possibility of a rally into Thanksgiving," and in this, he and Lee are in agreement. (Lee's Thanksgiving-rally view is illustrated in our Chart of the Week below.)

Lee sees a supportive backdrop for stocks in both the near- and intermediate-term. In his view, President Trump is likely to be "the most pro stock-market President in history" and thus likely to course correct in response to market concerns, acting as a put on the markets. Similarly, with a rate-cutting cycle underway, the Federal Reserve has turned dovish and this, in turn, will act as a Fed put on the markets, in his view. "Even if the pace at which the rate cuts arrive slows down, this would still be a dovish Fed," Lee noted.

Look further out, however, and Newton is slightly less sanguine. "You know, it could be setting up to be a more interesting December and year end than many people expect, only because the markets have already run up 15% in the last three months. So we've already sort of predated our so-called Santa Claus rally," he suggested.

Furthermore, Newton sees signs of potential consolidation after Thanksgiving. As he has noted in recent weeks, he again pointed out at our weekly huddle that "breadth has been deteriorating in the last couple months. We're down to about 39% of all stocks above their 10-day moving average. That's not incredibly encouraging to see. When the majority of stocks now aren't even above their 10-day moving averages, to me this shows that the market's not really as strong as what the S&P 500 is showing us."

Looking at sectors, he noted, "Half the sectors have been down for the last month, and if we want to have our year-end rally, it is important that we really start to show more strength across the board." Newton singled out Technology as a leading cause for concern, noting that the top-performing sectors have been Financials and Industrials. "Technology has been down over 1% over the last month, and that's with the S&P 500 at or around new highs," he observed. A weak Technology sector "doesn't always mean that we have to have a correction, but it is important to start to see Tech start to join the party sooner than later."

Lee suggested, however, that with sentiment not yet at peak bullishness, there could be enough upside potential to sustain markets until the end of the year. "As we all know, when sentiment reaches a 'bullish extreme,' that's when we see equities priced to 'perfection.' By several measures, including FINRA margin debt and AAII's net bulls percentage, we are not there at that point yet."

Elsewhere

Cash-strapped battery start-up Northvolt filed for Chapter 11 bankruptcy, dealing a setback for European hopes to counter Asian dominance in electric-vehicle batteries. Northvolt has notched significant misses in battery-production targets, both in terms of deadlines and volumes, and it faces a Swedish investigation into workplace safety practices after an employee died in a factory explosion last year.

Archegos Capital Management Founder Bill Hwang was sentenced to 18 years in prison after his fraud and market-manipulation conviction. The collapse of Archegos caused huge losses for a number of banks, which prosecutors claim were deceived about Archegos' collateral and trading activities. Hwang has indicated he plans to appeal.

The Department of Justice wants Google to divest itself of its Chrome browser business after the company's antitrust conviction for its search-engine monopoly. The DOJ indicated its intentions in a court filing, in which it suggested that it might also ask a federal judge to order the sale of Google's Android mobile operating-system business. Google described the proposal as going "wildly overboard."

Former Brazilian President Jair Bolsonaro was indicted for allegedly plotting a coup d'etat after he lost his 2022 bid for re-election. Under Brazilian law, the indictment will then be referred to Prosecutor-General Paulo Gonet, who will decide whether to file formal charges. The indictment covers 36 other people, most of whose identities were not disclosed.

U.S. prosecutors filed bribery and securities-fraud charges against Gautam Adani, the Indian billionaire and head of the Adani Group. The civil and criminal charges allege that Adani and his co-defendants paid $250 million in bribes to Indian government officials to secure solar-energy contracts for Adany Green Energy. Subsequently, they are alleged to have made false and misleading statements about the company's anti-corruption while raising money from U.S. investors.

Two undersea communications cables in the Baltic Sea were severed, raising European suspicions of sabotage. One of the cables linked Germany and Finland, while the other linked Sweden and Lithuania. German Defense Minister Boris Pistorius asserted that "no one believes these cables were severed by mistake, and I also don't want to believe versions that it was anchors that by chance caused damage to these cables." Russia has denied involvement. The Danish navy has detained a ship registered in China as part of the investigation, but no suspects have been named at this early stage of the investigation.

Super Micro Computer hired BDO as its new auditor after the resignation of two predecessor auditing firms in less than two years. SMCI's fiscal year ended June 30, and Ernst & Young's resignation as auditor caused the company to miss its annual-report filing deadline, putting its Nasdaq-listing eligibility at risk.

And finally: The American Farm Bureau Federation released its annual Thanksgiving Dinner Cost Survey showing that the typical Thanksgiving dinner will cost 5% less than it did last year - though the price is still 19% higher than 2019's pre-pandemic levels. The federation's $58.08 estimate covers a dinner that feeds 10. It includes turkey, cranberries, sweet potatoes, carrots and celery, green peas, dinner rolls, stuffing, homemade pumpkin pie, and whole milk.

Important Events

Prev.: 0.35%

Est.: 722K Prev.: 738K

Est.: 0.3% Prev. 0.3%

FS Insight Media

Stock List Performance

| Strategy | YTD | YTD vs S&P 500 | Inception vs S&P 500 | |

|

SMID Granny Shots

|

+49.81%

|

+26.71%

|

+26.71%

|

View

|

|

Upticks

|

+37.84%

|

+12.98%

|

+45.36%

|

View

|

Articles Read 1/2

🎁 Unlock 1 extra article by joining our Community!

Stay up to date with the latest articles. You’ll even get special recommendations weekly.

Already have an account? Sign In 51e6f3-f91aef-486fbc-ca0275-c6ee8e

Already have an account? Sign In 51e6f3-f91aef-486fbc-ca0275-c6ee8e

Articles Read 1/2

🎁 Unlock 1 extra article by joining our Community!

Stay up to date with the latest articles. You’ll even get special recommendations weekly.

Already have an account? Sign In 51e6f3-f91aef-486fbc-ca0275-c6ee8e

Already have an account? Sign In 51e6f3-f91aef-486fbc-ca0275-c6ee8e