Gox Wallet Movements Still Present a Risk, But Macro & Politics Keeps Us Allocated Here (Core Strategy Rebalance)

Key Takeaways

- Despite our view that the amount of sell pressure from Mt. Gox coins is more FUD than fact, our learnings from the past week suggest that wallet movements still pose a near-term risk to BTC.

- ETHBTC has shown strength following the recent drawdown. We expect clarity on ETF approval soon. The supply overhang for ETH is minimal, making it a favorable risk/reward option.

- The partisan nature of crypto has intensified once again, presenting an overlooked potential tailwind heading into November.

- Overall, today’s CPI print and recent softening job data create a suitable macro environment for crypto to find a near-term bottom.

- Core Strategy – We acknowledge the near-term risk to the market from the impending transfer of BTC out of the Mt. Gox estate, which could result in short-lived downside volatility. However, inflation continues to fall, economic data remains non-recessionary, and political tailwinds are intensifying, leaving us fully allocated. Given the positive macro environment and the near-term market risk, we believe it is prudent to trim some of the underperformers from the core strategy and shift relative allocation among majors from SOL to ETH.

Discussing the Supply Concerns

On balance, macro conditions have moved in our favor thus far in early Q3. We have received soft jobs numbers and softer ISM reports, and cooler inflation figures, which have sent rates and the DXY lower. Unfortunately, the mere reveal of imminent sales from the German BKA and the solidification of the Mt. Gox disbursement timeline were not enough to put a bottom in for bitcoin.

German BKA

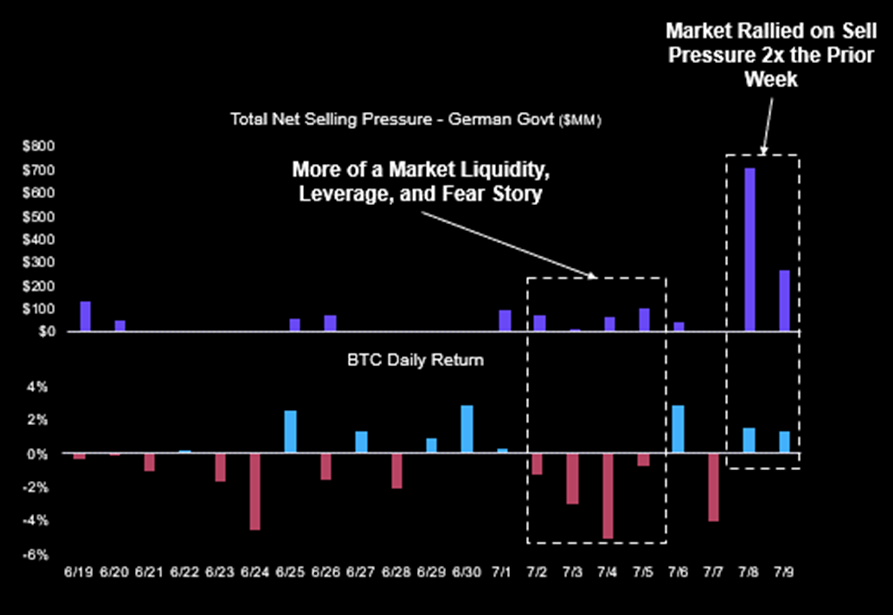

The actual movement of coins from German wallets caused massive selling from market participants. It is important to note that it wasn’t necessarily a simple supply/demand mismatch that caused the drawdown, but rather a hit to market psychology during a rather illiquid time. As shown in the chart below, the Germans started moving their coins to partner exchanges during the week of July 4th, which is intuitively a much less liquid week for all assets as many Americans are away from their desks. This sparked fear in the market, leading traders to close out positions, resulting in cascading liquidations across derivatives markets.

Fast forward to this week, and we have since rebounded considerably from the drawdown to $53.5k, as the market has absorbed the selling of the German coins quite seamlessly. This rebound occurred despite the Germans selling much more BTC than they did the week prior. In fact, on Monday alone, they sold twice as much BTC as they did all of last week. This is likely because traders were back at their desks, markets were once again liquid, the market was deleveraged, and the fear of the Germans selling had already been priced in.

As seen in the chart below, we are almost through all of the German holdings, which is a positive sign. Further selling from this entity is unlikely to have a significant impact on asset prices.

What is FS Insight?

FS Insight is a market-leading, independent research boutique. We are experts in U.S. macro market strategy research and have leveraged those fundamental market insights to become leading pioneers of digital assets and blockchain research.

Tom Lee's View

Proprietary roadmap and tools to navigate and outperform the equity market.

Macro and Technical Strategy

Our approach helps investors identify inflection points and changes in equity leadership.

Deep Research

Our pioneering research provides an understanding of fundamental valuations and risks, and critical benchmarking tools.

Videos

Our macro and crypto videos give subscribers a quick and easy-to-understand audiovisual updates on our latest research and views.

US Policy Analysis

Our 40-year D.C. veteran strategist cuts through the rhetoric to give investors the insight they need.