Time to Hold Your Nose and Buy (Portfolio Rebalance)

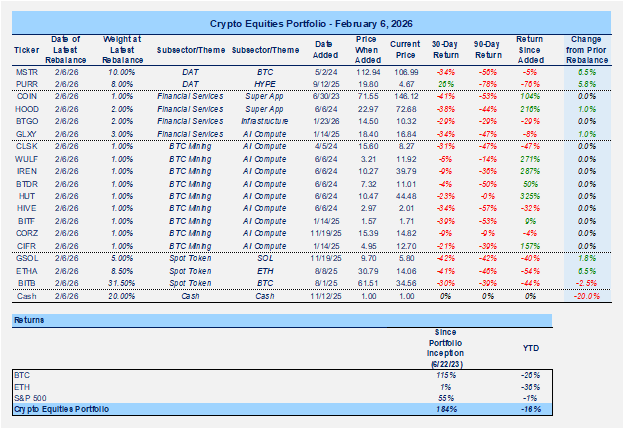

Portfolios

Note: Please see the end of this note for additional commentary on rebalance.

Extremely Oversold

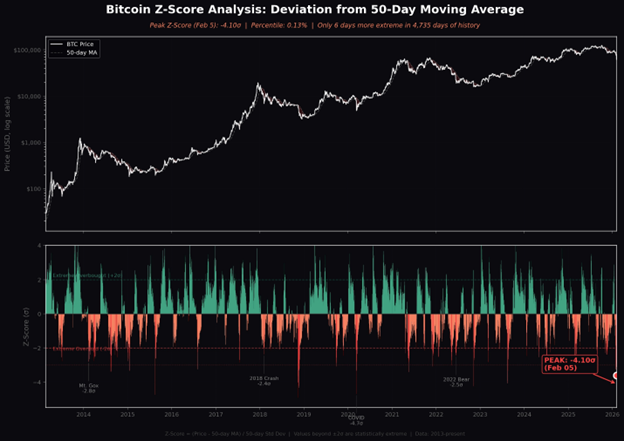

Using BTC as our proxy for the broader crypto market, we can see that relative to historical selloffs, this episode is one for the record books in both pace and magnitude. On February 5th (spot $61,563), BTC’s z-score relative to its 50-day moving average hit -4.10, a reading that falls in the bottom 0.13% of all observations since 2013.

Only six trading days in Bitcoin’s liquid market history have registered a more severe deviation. With BTC now trading down 51% from January’s peak of ~$126,000, this selloff rivals the worst moments of prior bear markets, trailing only the November 2018 capitulation (-4.91) in severity.

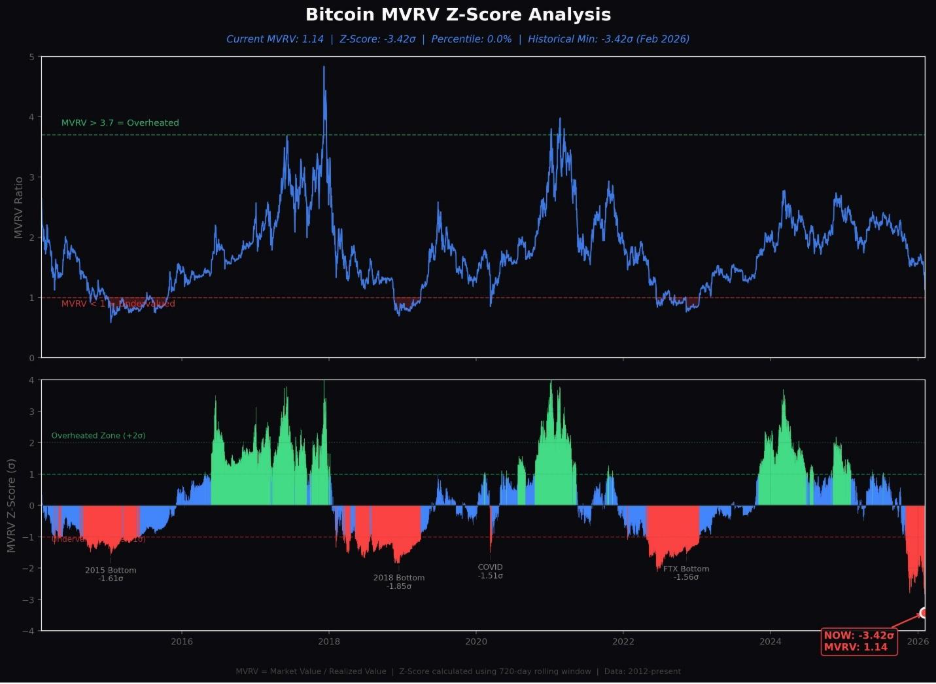

Bitcoin’s MVRV ratio, which compares market value to the aggregate on-chain cost basis of all coins, has plunged to 1.14, producing a 720-day rolling z-score of -3.42. This is the most extreme reading in the metric’s history, surpassing the lows registered during the COVID crash, the FTX collapse, and the 2018 bear market capitulation.

The current MVRV implies that Bitcoin’s market cap sits just 14% above realized value, meaning the average holder is barely in profit. Over the past two years, MVRV averaged 2.12 during a sustained bull market. The collapse to 1.14 represents a faster and deeper reversion than during any prior episode. While MVRV has not yet breached 1.0, the level that historically marked generational accumulation zones in 2015 and late 2018, the speed of the decline suggests capitulation.

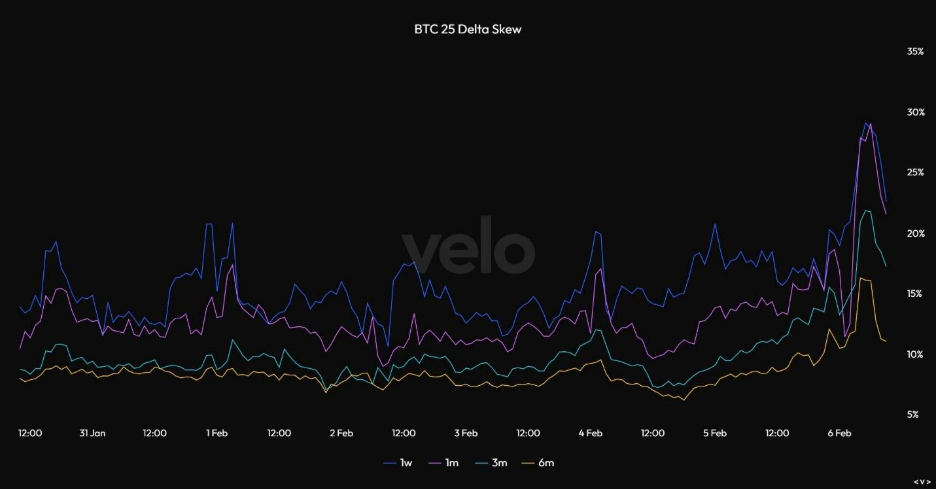

The options market is also reflecting extreme bearishness not seen since the 2022 bear market lows. One-month 25-delta put/call skew reached ~30% on Thursday, approaching readings last observed in November 2022.

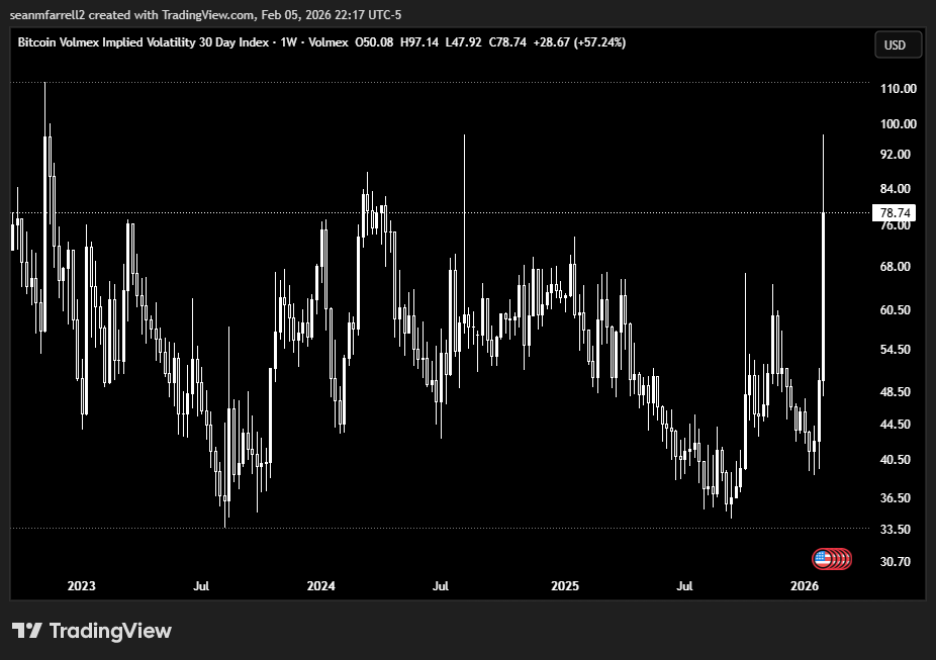

BVIV (the VIX for BTC) reached 97, one of the highest readings on record and the highest since the August 2024 Tokyo “Black Monday” event.

Sentiment Near All-Time Lows

From a sentiment perspective, comparisons across cycles are always imperfect, but anecdotally there is an outsized sense of fear and fatigue among crypto-native participants.

Regulatory tailwinds are broadly favorable, and institutional capital is finally entering the ecosystem in a meaningful way. However, prices do not reflect these positives. My interpretation is that much of this optimism was front run (think of it as a prolonged “sell the news” event).

At the same time, crypto-native positioning remains skewed toward the less fundamentally sound parts of the market, and vaporware is being displaced as market efficiency improves.

Beyond anecdotal conversations, we have also seen:

- Several high-profile investors exiting the space

- Public concerns about Binance solvency (possible, but low probability in my view)

- Calls for MSTR to be “margin-called” (which would likely require BTC to sustain in the $20k to $30k range for an extended period)

Risk Starting to Clear in Equity Markets

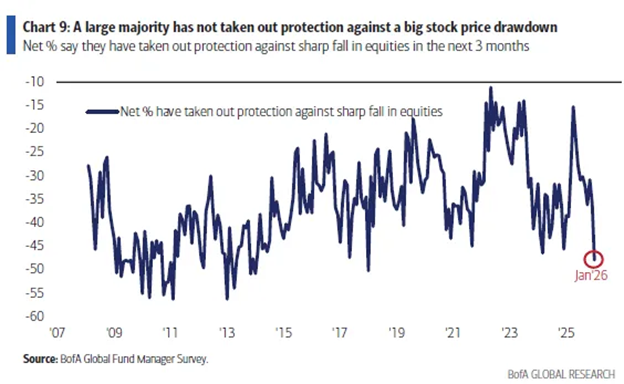

One of my primary concerns recently has been broader risk positioning. Cash allocations have been near all-time lows (per recent BofA fund manager surveys), high-yield spreads have been tight, and both the VIX and MOVE indices had been subdued.

We are finally starting to see some of this unwind. Deleveraging in precious metals and weakness across parts of technology have led to incremental derisking in equities.

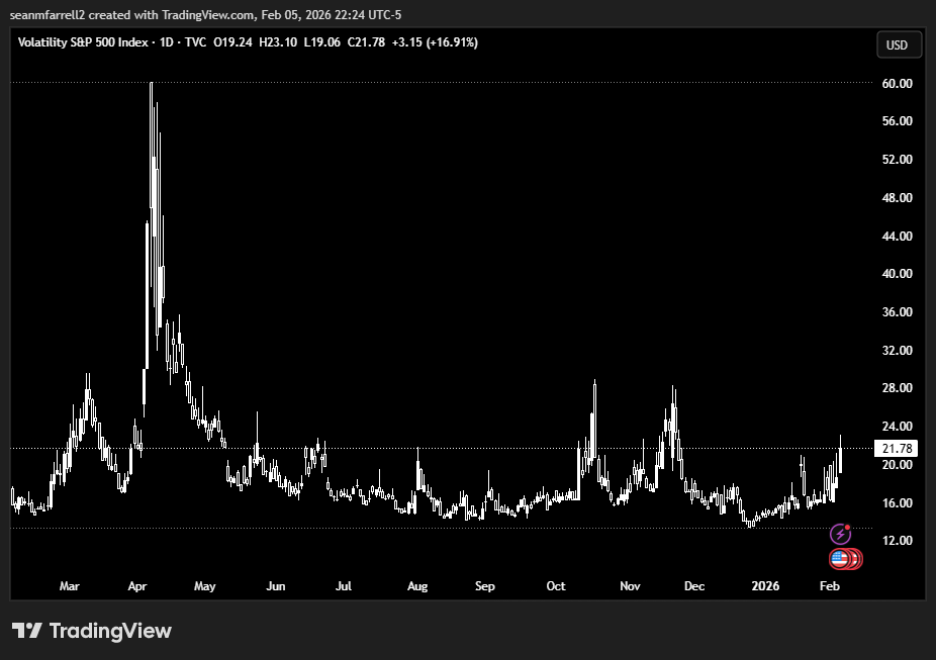

The VIX reached 23, its highest level since mid-November. While bond market volatility (MOVE) remains muted from a cycle perspective, it appears to be stabilizing in the 55 to 65 range.

Lingering Concerns: Bodies and Equities

If I had to isolate what still gives me pause, it comes down to two considerations:

- While broader risk markets have deteriorated somewhat, the S&P is only ~3% below all-time highs and high-yield spreads have yet to widen meaningfully, implying there is still room for positioning to unwind.

- There were clearly forced sellers in crypto this week. In past cycles, the market usually identifies where those stresses sit. This time, despite conversations with well-connected participants, there has been little visibility into who the “bodies” are.

That said, it is worth remembering two things. First, risk typically clears from crypto before it clears from equities. Crypto often bottoms first. Second, by the time the bodies are publicly identified, most of the selling pressure is already behind us, as we saw during the FTX collapse.

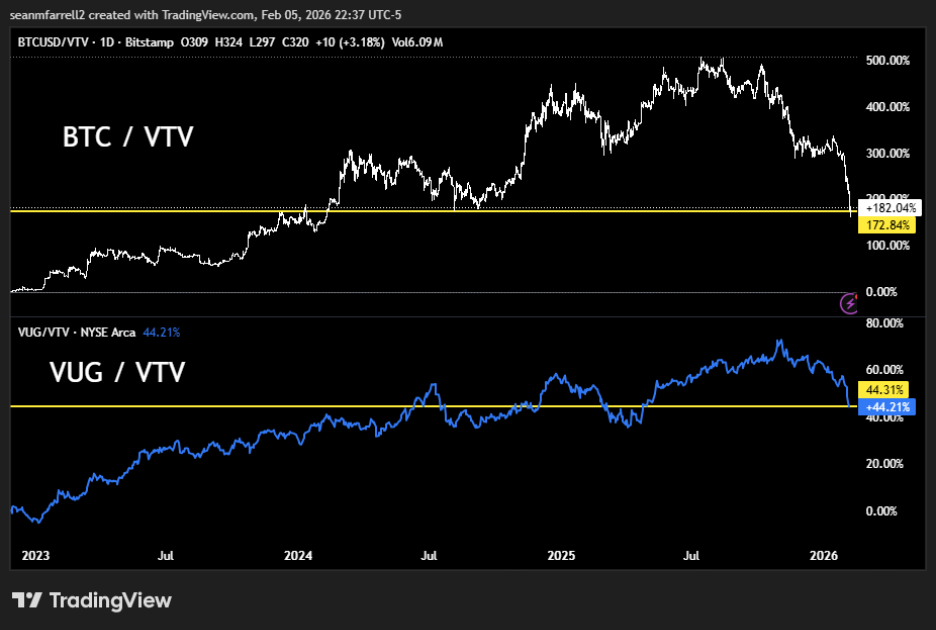

Final Chart: Growth vs Value

Finally, just to leave a few words of encouragement for the disillusioned, it is worth remembering that BTC’s performance reflects both monetary and growth dynamics. It tracks monetary trends well, similar to gold, but it also carries a meaningful risk premium due to its early stage of adoption (17 years versus several millennia for gold).

As a result, while some might point to gold’s recent strength and BTC’s divergence as evidence that the Bitcoin thesis has failed, I would argue the opposite. The gap largely reflects differences in asset maturity, the degree of optimism that had already been priced into BTC, incremental hawkishness being digested across markets following the Warsh nomination, and real, unresolved risks (e.g., quantum) that warrant a higher discount rate.

In fact, if we look at growth versus value performance since 2023, BTC’s directional path is not all that dissimilar. It has outperformed growth equities, likely due to the monetary component embedded in its price, but until it reaches broader adoption, it will probably continue to exhibit growth-like characteristics and the higher volatility that comes with them.

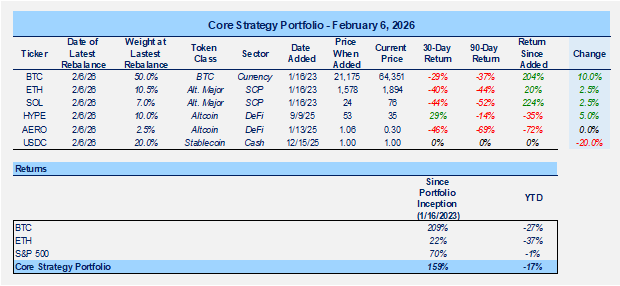

Portfolio Changes

In my token portfolio, I am increasing net long exposure to 80%. Despite the points outlined above, I like leaving some wiggle room for another visit into the $50k’s. We can always add on strength as well.

- Raising BTC to a 50% allocation given the capitulation and deeply oversold conditions outlined above

- Increasing SOL to 7%. It has been hit the hardest over the past few days, likely in part due to the largest and most visible SOL supporter (Samani) stepping away from the space. Price also reached the FTX estate sale level, which should serve as an important psychological reference point

- Increasing ETH to 10.5%. ETH has also struggled recently amid controversy around Vitalik’s comments on the protocol’s direction (which I believe are being misinterpreted), as well as public sales from wallets labeled as his

- Increasing HYPE to 10%. It has been the strongest name in the portfolio as of late. Its relative resilience over the past week suggests it is under-owned, and HIP-3 markets continue to show solid traction

In the crypto equities portfolio, I am making directionally similar adjustments.

- Increasing BTC exposure via MSTR, partially funded via spot BTC for the reasons cited above. I am shifting some BTC exposure into MSTR given its depressed mNAV (~1.07x), which offers more attractive relative value

- I am less confident that GLXY, and miners more broadly, have found a durable low given ongoing discussions around ERCOT potentially tightening data center grid approvals amid rising energy costs. That said, the current valuation embeds significant optionality, and I find the risk/reward compelling enough to add modestly

- Adding a small position in HOOD, now trading ~50% below its all-time high. I previously flagged it as the most expensive name in the basket, and this retracement brings valuation back to levels where adding exposure makes sense, as the longer-term thesis remains intact

- Adding to ETHA and PURR to better align our ETH and HYPE exposure with the token portfolio