Farcaster Marks Eighth Unicorn of 2024

Weekly Recap

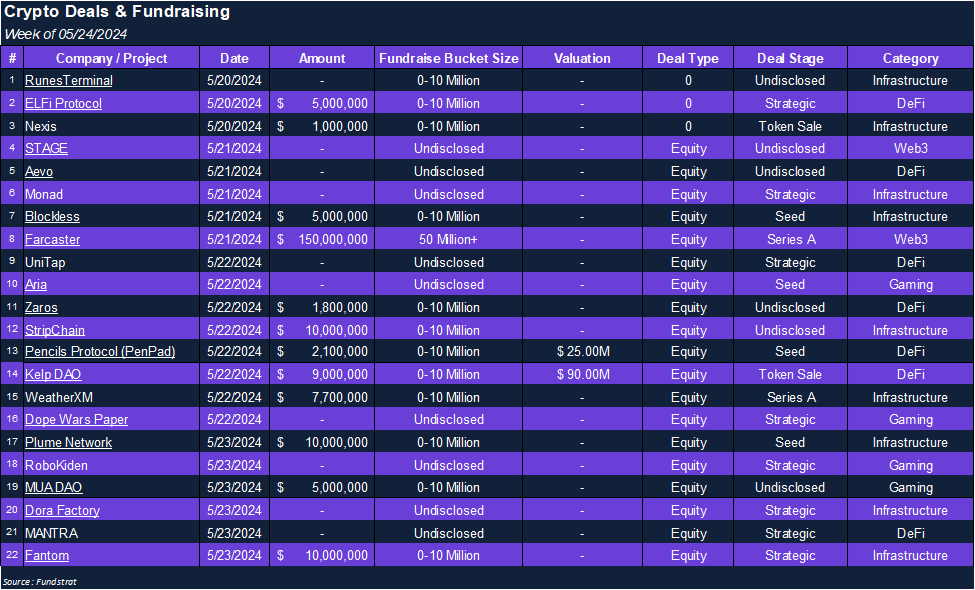

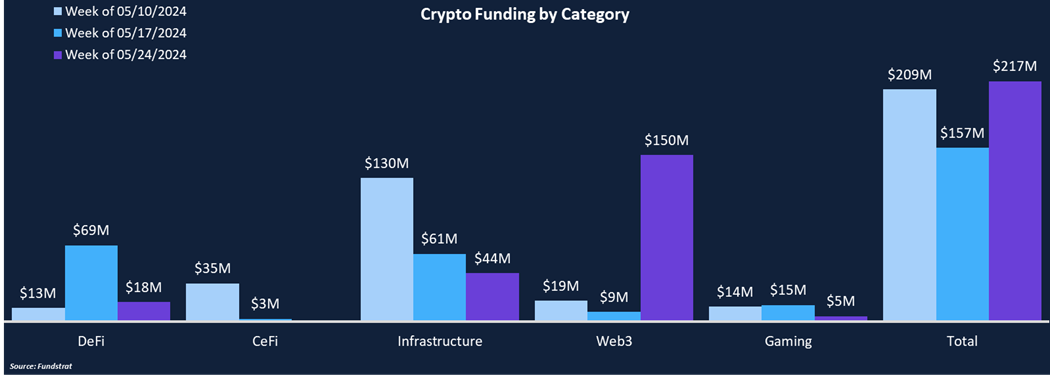

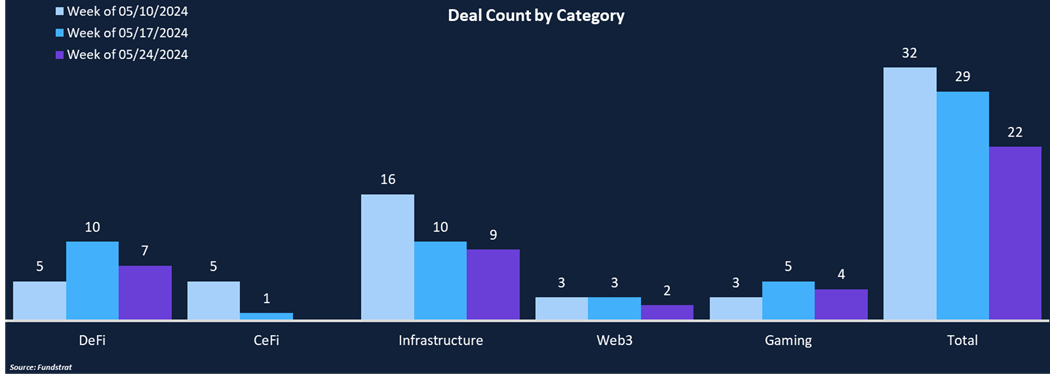

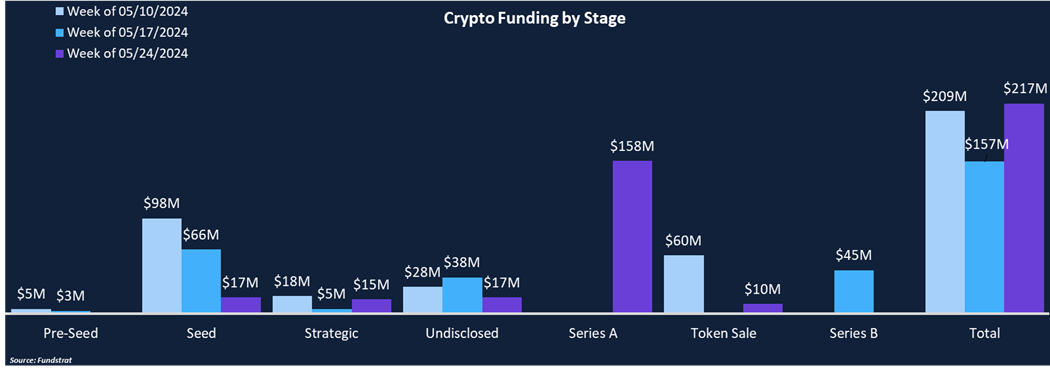

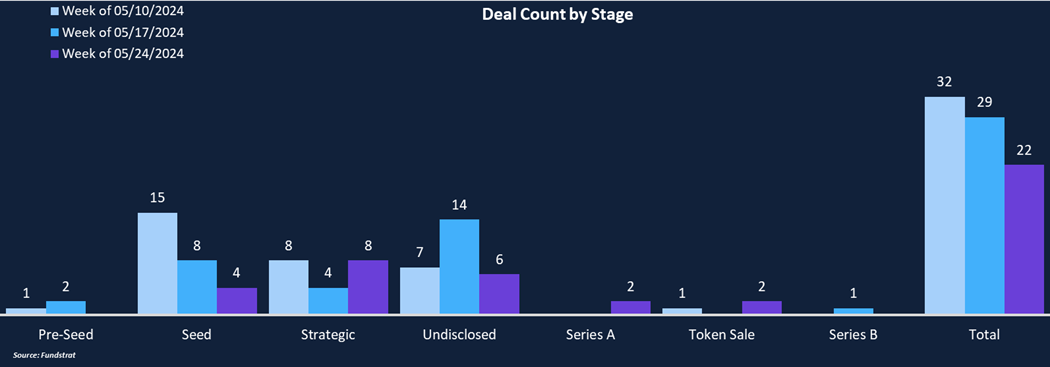

Despite 24% fewer deals this week, total funding rose 38% from $157 million to $217 million, largely due to Farcaster’s $150 million Series A round (DotW). There was only one other Web3 deal besides Farcaster, which was the leading category from a funding perspective. Similarly, Series A rounds were the leader in funding this week, totaling $158 million across just two deals: Farcaster and an $8 million fundraise completed by WeatherXM, a dePIN project focused on a new weather network. Infrastructure had $44 million in funding across nine deals, DeFi had $18 million across seven deals, and there were no CeFi deals this week. A deal stage other than Seed rounds tallied the most deals for the first time in a few weeks. Strategic rounds were the most popular, totaling eight deals, including deals completed by Fantom and Monad.

Funding by Category

Funding by Stage

Deal of The Week

Farcaster, a web3 social media platform, raised 150 million in a series A round led by Paradigm with participation from a16z, Haun Ventures, Variant Fund, Union Square Ventures, and Standard Crypto. The funding round values Farcaster at $1 billion, and the fresh capital will be used to add new product features, increase the number of daily active users, and hire additional engineers. We are beginning to see a rise in valuations across private markets. Farcaster is the second company to earn a $1 billion valuation in May and is the eighth so far in 2024, surpassing 2023’s total less than halfway through the year.

Why is This Deal of the Week?

Farcaster’s mobile app Warpcast is a new social media platform that gives users more data control, letting them easily monetize content and enhance customizability via its open-graph styling tool. Creators can design unique views called “frames,” where people can interact with polls, galleries, or mini-apps within the app. Farcaster’s adoption trends have been impressive since launching in October. Farcaster has seen over 350k paid signups and a 50x increase in network activity. It has accumulated over 40,000 daily active users, with an average of 1.2 million posts per day. For comparison, friend.tech, one of its largest competitors, has averaged slightly under 7,000 daily users over the past 30 days. Farcaster recently announced support for Arbitrum, bringing its functionality to the L2 in addition to Ethereum and Solana. Crypto is still waiting for its killer consumer app that brings a mass audience on-chain, and Farcaster is on the right track working towards that goal.

Selected Deals

Weather XM, a decentralized weather network, raised $7.7 million in a Series A round led by Lightspeed Faction. Other investors include Protocol Labs, Borderless Capital, Arca, Alumni Ventures, Placeholder VC, and others. WeatherXM produces various weather station hardware devices that collect local environmental data and creates cryptographic proofs that are stored on Filecoin. The data can be queried and processed to create hyperlocal weather forecasts and create on-chain weather prediction markets, and parametric weather insurance products. The funding will be used to advance the network and further develop on-chain weather derivatives.

IVX, a 0-days-til-expiration (0DTE) options protocol for crypto assets, raised $1.2 million in a seed round led by Animoca Brands and Avid. Other investors include Big Brain holdings, Cogitent Ventures, Forbole, Web3Sport and others. IVX is being built on Berachain, an EVM chain powered by proof-of-liquidity that is expected to launch on mainnet this year. 0DTE options are extremely popular in traditional markets and bringing them to crypto has the potential to steal market share from perpetual future traders. The funding will be used to continue building a user-friendly, accessible, and liquid 0DTE options market.

Blockless, a decentralized compute network, raised $5 million in a seed round led by M31 Capital and Frachtis with participation from Chorus One, Interop Ventures, and No Limit Holdings. Blockless is aiming to provide cross-chain computing power to empower all blockchain applications. Blockless Network is the orchestration layer between daps, networks, and users. Similar to how Uber connects riders to drivers, Blockless will connect dapps to computing power. Blockless was founded by former Akash Network and Binance employees and its mainnet and token launch (BLESS) are expected to go live in Q3 of this year. The funding will be used to add additional hires to its team of ten and accelerate its product development ahead of its testnet launch in the next few weeks.