Equities have been punishing YTD, but sector leadership is clearly cyclical

The best way to describe the first 25 trading days of 2022 is treacherous. On many fronts, we are facing inflection points on monetary policy, COVID-19, inflation, geopolitics, elections (mid-terms) and even general mood. So it is not surprising to see investors apply a “hair trigger” to stocks and markets. And naturally, conviction remains low.

Of course, our base case for 2022 (from early Dec) was the 1H of 2022 would be treacherous, but this has been worse than we expected. But remember the following:

- if a stagflation or even a recession were looming, this is not the sector leadership one expects

- thus, we view the 1H turbulence as “anxiety about inflections” more than looming disasters

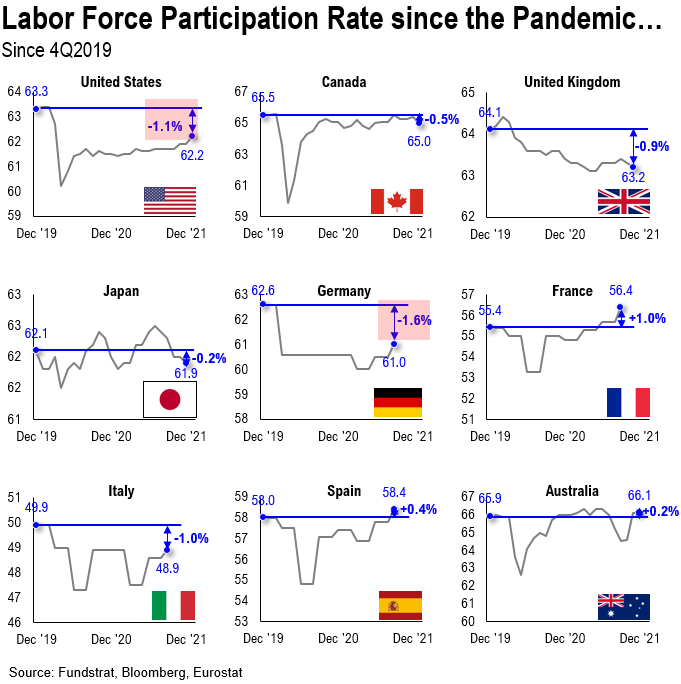

Let’s also zero in on wage inflation. Wages are rising in the US and that is the reason economists are saying the Fed has to act, as rising wages is a sign of a strengthening inflation trends. But as many are aware, the shortages of labor are not due to an actual shortage of labor:

- it is a sharp drop in participation rates

- many other nations are seeing participation rates recover to pre-pandemic levels

- but the in US and in Germany, these figures are lagging – if policymakers shift away from pandemic planning

- perhaps we could see policies incent a return of eligible workers into the workforce

- early retirement might be a factor

- but in a world of inflation, those retired will not have enough saved

- inflation hurts savers and benefits borrowers

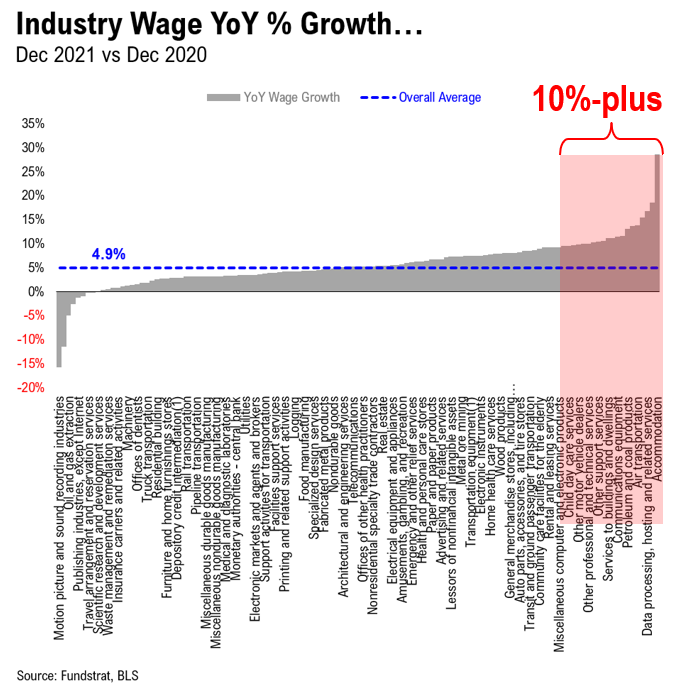

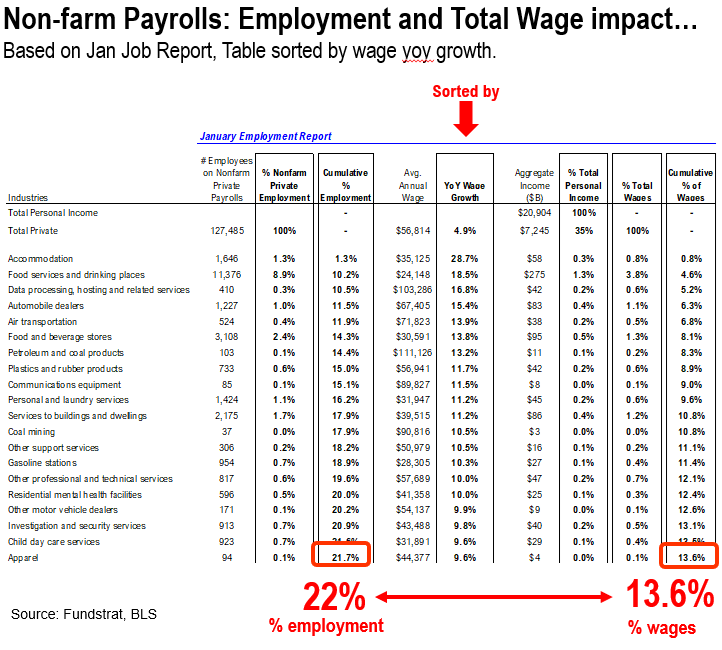

22% of the labor force is seeing +10% wage gains, but this 13% of total labor income

Wages are on the rise in the US. Our data science team, led by tireless Ken, listed the industries seeing 10%-ish wage gains. It is a large list.

- topping the list are service industries – accommodation, food services, auto dealers, etc

But this table below looks at the cumulative impact from these 10%-wage growth sectors.

- 22% of the labor force is seeing 10% wage gains, or 1 in 5 people

- this cohort is 13% of wage income

In other words, these are below average share of wages in general. This is consistent with what is well known. The best wage gains are among the lower tier of income earners. But this also suggests that the wage inflation risks are not as pervasive as one believes.

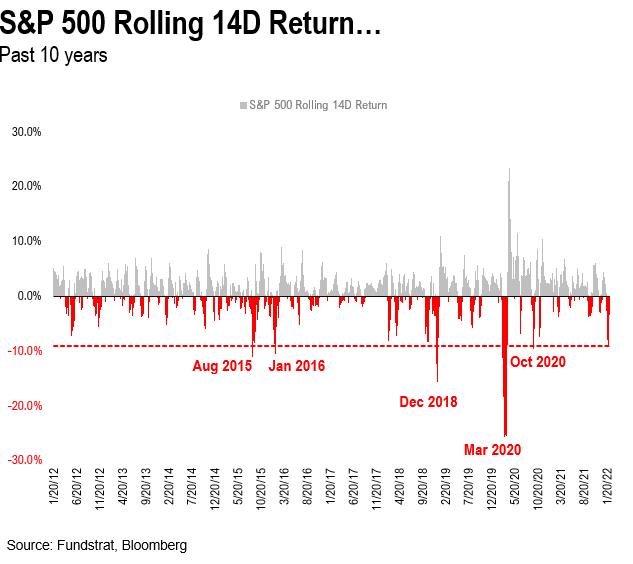

Reminder, after waterfall decline, history says +7%/ +13% next 3M/ 6M

Last week, we published some data around waterfall declines in equities. The S&P 500 posted a waterfall decline of 11% peak to trough over 14 days. On a closing basis, it would be a ~9%

decline. While many things seem common in this pandemic era, a fall of this velocity is actually rare:

- foremost, it shows the fragility of confidence

- sort of flies in the face of those saying markets are in a bubble and investors are too bullish

In fact, in the past 10 years, this velocity of fall has only happened 5 prior times and these are shown below:

- 5 of 5 times, this was at the end of a sell-off

- not the start

- and markets staged a fierce and violent rally after each of these

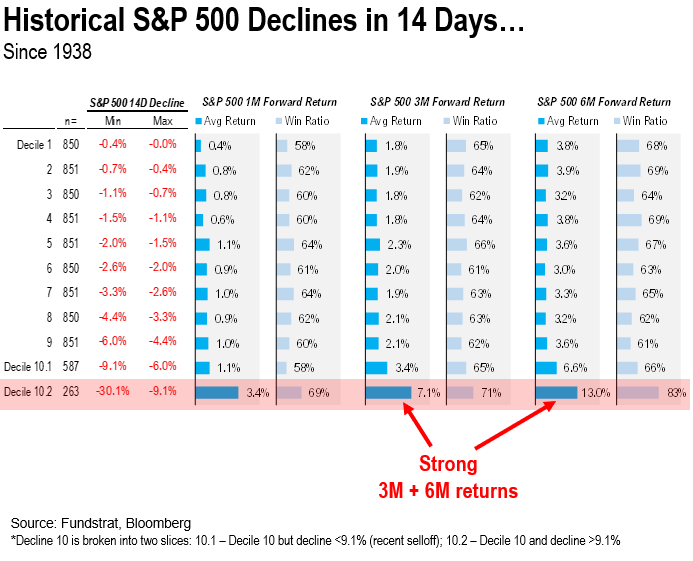

Tireless Ken and the data science team compiled forward market returns, following 14D market declines. These are tiered below into deciles:

- the ~9% fall ranks as the “worst decile” since 1938

- the worse the 14D decline, the larger the bounce

- the relationship holds as we move down the deciles

- at the worst decile, forward 1M, 3M and 6M returns are very strong

- forward 3M and 6M returns are 7.1% and 13.0% – this implies S&P 500 > 4,850 before 1H2022

- hence, this reinforces our view that markets can stage a strong rally from Jan lows into Feb

- but we believe 1H2022 remains treacherous

Figure: Way forward ➜ What changes after COVID-19

Per FSInsight

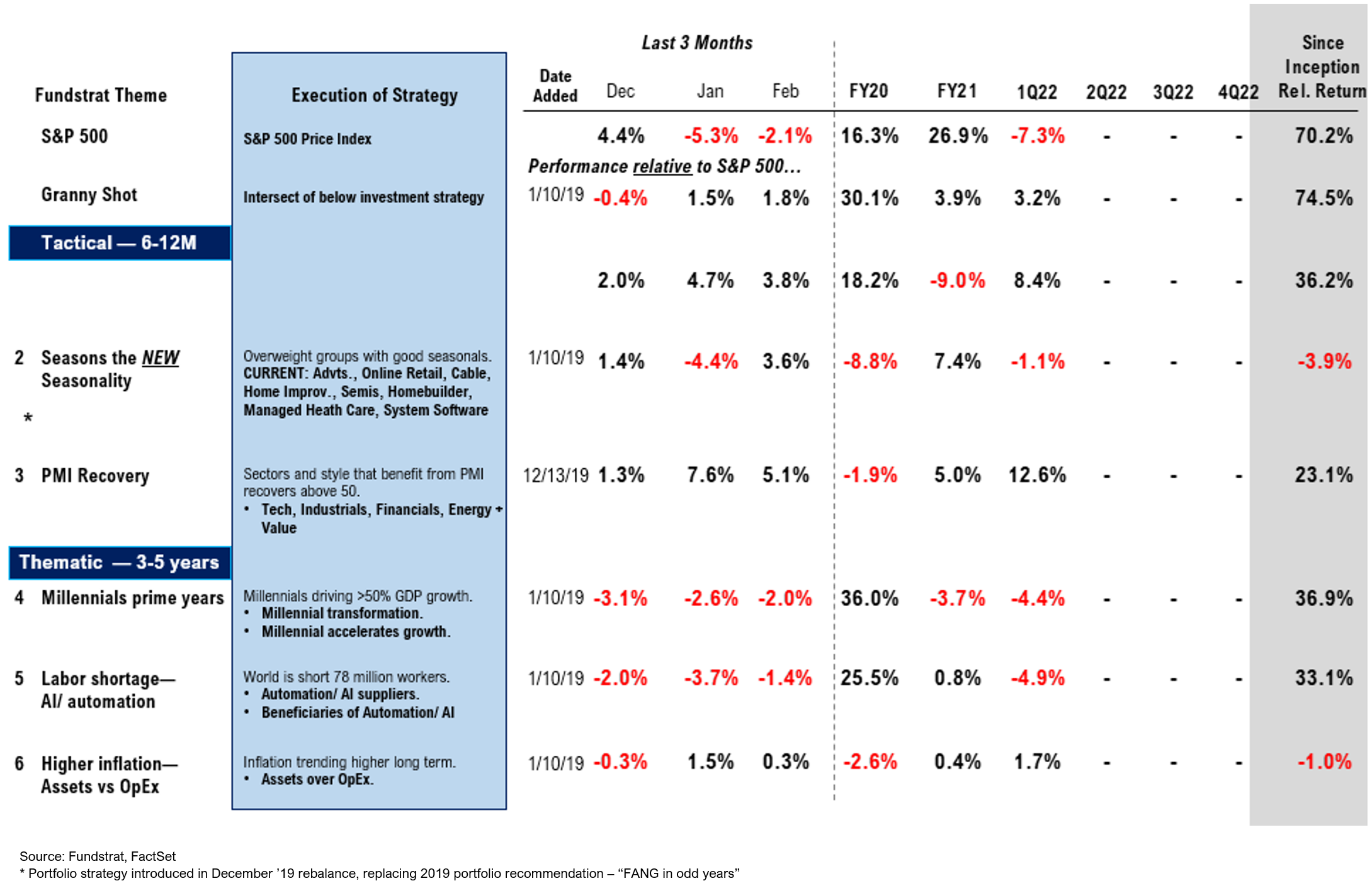

Figure: FSInsight Portfolio Strategy Summary – Relative to S&P 500

** Performance is calculated since strategy introduction, 1/10/2019