Clues continue to emerge for weakening labor = bad news is good for market stability

WEBINAR ALERT: 5/19 at 2pm ET for FSinsight Members

We are delighted to announce we are hosting a webinar with Tom DeMark, founder of DeMark Analytics.

- Equities have been in a relentless downturn since the start of 2022.

- While valuations have become considerably more attractive, and sentiment rock bottom, investors are still hesitant to add risk until there are clearer signs the “worst is priced in”

- Tom DeMark and his DeMark indicators are exceptionally valuable tools in identifying these turning points

- Recall, Tom DeMark indicators called the precise bottom for stocks in March 2022

The link to register for this webinar is —> HERE

Market still debating wide outcomes, but consensus sees a recession and further downside…

In conversation after conversation, consensus generally sees Fed hiking cycle inevitably leading to a recession. But this is only the central case, and the reality is investors see massively wide outcomes.

- on the downside, many see Fed hiking leading to a breaking economy and a deeper recession given the advance of markets since 2020

- on the upside, an achievement “soft landing” would be a positive surprise, as the >25% decline in the NASDAQ (and 20% in S&P 500) means downside is baked in.

While stocks have been gut punched for 6 weeks straight, it should be no surprise that consensus has markedly shifted towards the doom camp. And pundit after pundit sees further downside. Granted, the technicals are pretty bad as well, so there is a buyers’ strike in place.

But as we look at incoming data, there are “green shoots” that point to mitigation of the bearish case. Granted, there are also “negative shoots” out there. And at the moment, this is the key statement:

- Fed Chair Powell speaking at the WSJ’s “Future of Everything Festival” reiterated the FOMC’s view on inflation

- They are not looking for “nuanced” signs inflation is cooling, but in a convincing way

…So “green shoots” on convincing declines is key — job openings

Obviously, the incoming data needs to point to a “convincing way” of a decline in inflation. In our view, this is where consensus might be underestimating the speed and velocity. Previously, we noted:

- Used car prices weakening = lower inflation

- China opening alleviates future supply chain problem = lower inflation (eventually)

- inflation breakevens are cooling off = market seeing lower inflation vs a month ago

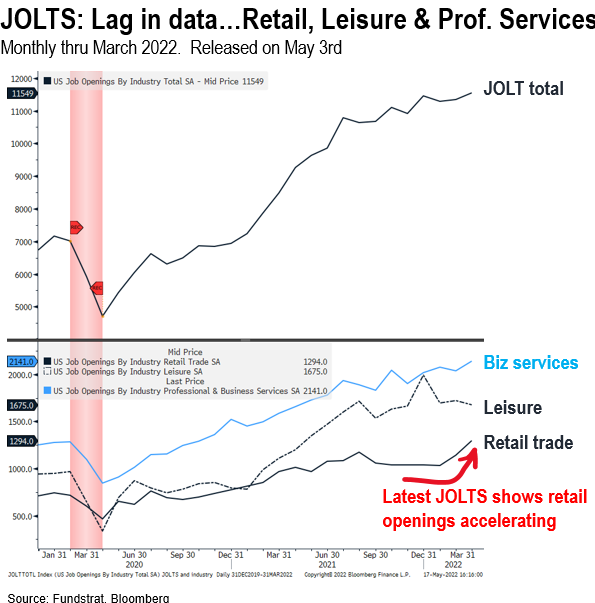

JOLTS data, used by Fed is only thru March or 6 weeks lagged…

The standard for job openings is the JOLTS survey and this metric is used by the Fed to talk about the tightness in labor markets. Powell reiterated that there is 2 jobs for every available worker.

- the latest JOLTS data is only March report (reported in early May)

- JOLTS data, therefore, is already 6 weeks stale

- labor markets softening is key

- especially since labor market participation rates are still low

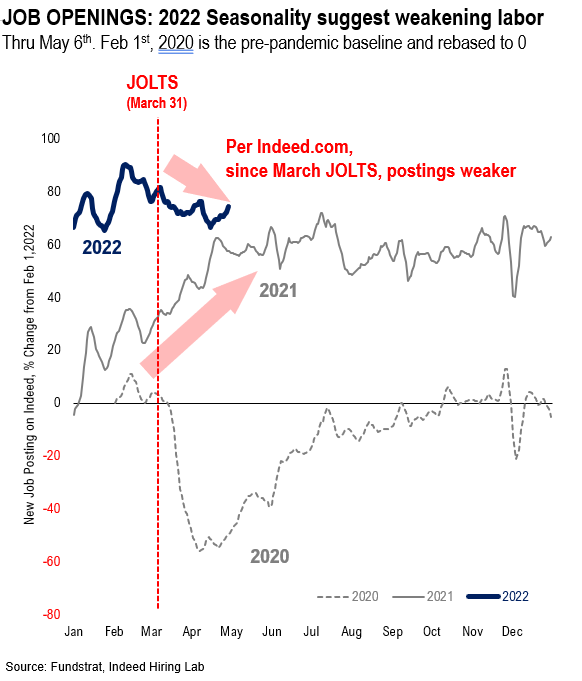

…Indeed.com data + Retailer earnings suggest hiring could be slowing

In this note, we highlight some signs that the labor market might be cooling, not due to financial conditions tightening, but due to “overhiring” due to Omicron:

- Indeed.com data shows job postings in 2022 are seasonally weaker than 2021 trends

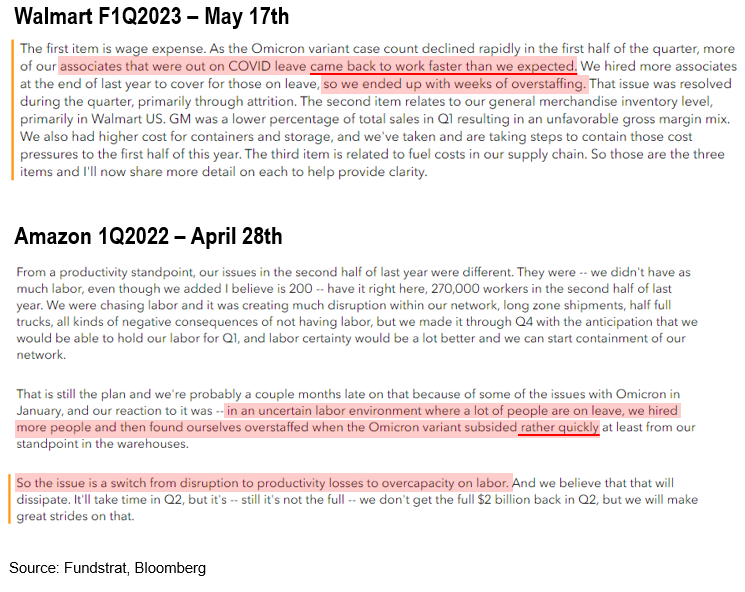

- Both Walmart (yesterday) and Amazon (4/28) both noted “overhiring” due to Omicron in 1Q2022

- And now both firms are “overstaffed” = future layoffs

Take a look at the data from Indeed.com. This is arguably a more “real time” barometer of JOLTS.

- Indeed.com data is thru May 6th

- that is 6 weeks additional data vs JOLTS

- Later this week, Indeed.com will show data thru 5/13

- See the weakness in job postings since 3/31?

- This is a sharp contrast to 2021, when job postings surged in the 6 weeks post 3/31

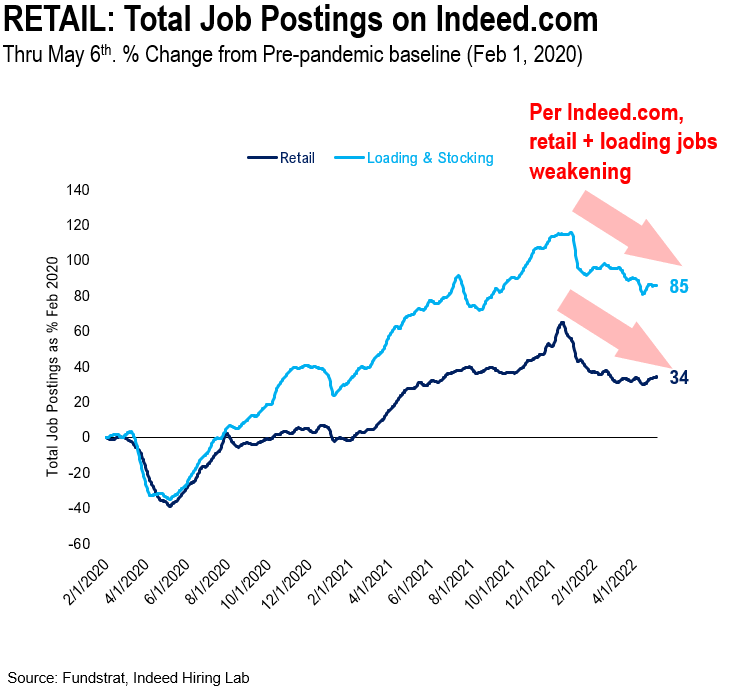

…Retail + loading job postings are where weakness emerging

The weakness is seen in retail and loading jobs. By the way, this dovetails exactly what Walmart and Amazon mentioned in their earnings calls in the past few weeks.

Walmart and Amazon both said they are “overstaffed” into March 2022 due to Omicron impact

Take a look at the commentary from both Walmart (yesterday) and Amazon (4/28) about staffing.

- both firms said they are now overstaffed

- the primary factor is the expected “outages” due to Omicron illness ended faster

- this is thru March 31

- both expect to trim after March

- JOLTS only reflects data through March 31

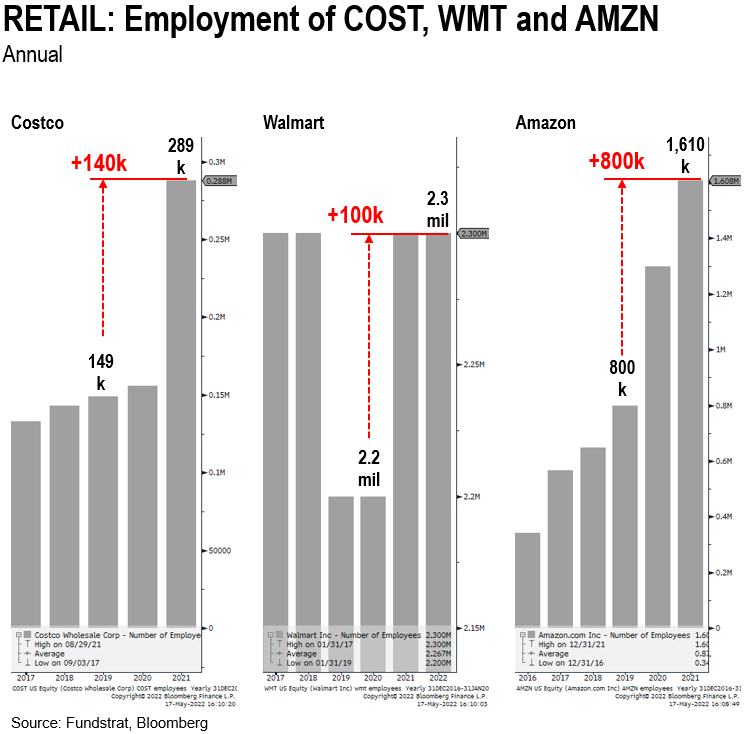

…reiterating retail added 1.3 million jobs since end of 2019, of which Amazon was >800k

And retailers hired like mad post COVID-19 to work around COVID-19 protocols and risks of outages. And as these protocols become less central, we expect hiring to weaken.

…But weaker jobs is only partially the problem, as participation rate needs to come up…

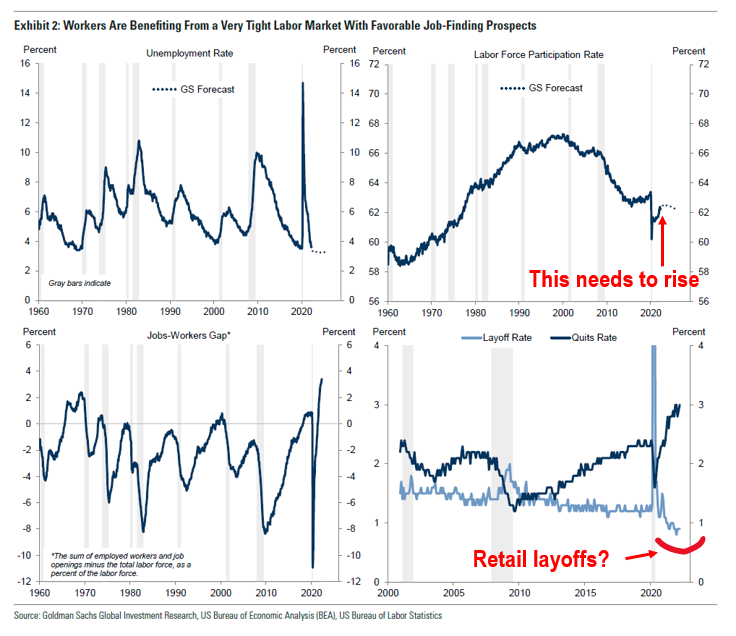

As Goldman Sachs labor dashboard makes clear, it is not just job openings that are an issue:

- labor participation rate is too low

- there are 684,000 FEWER people working today vs end of 2019

- will higher wages bring back workers?

- will falling 401Ks bring back retirees?

- maybe

STRATEGY: Stocks acting better, but still in “zone of despair”

Equities are still in that “zone of despair” below the S&P 500 4,114 level as shown below. This level is both the 2/24 low (invasion) and the shelf before stocks went into a horrific decline:

- S&P 500 has risen last few days

- and within 25 points of this level

- closing above this would improve investor appetite for stocks

- this is an IMAGINARY LINE by the way

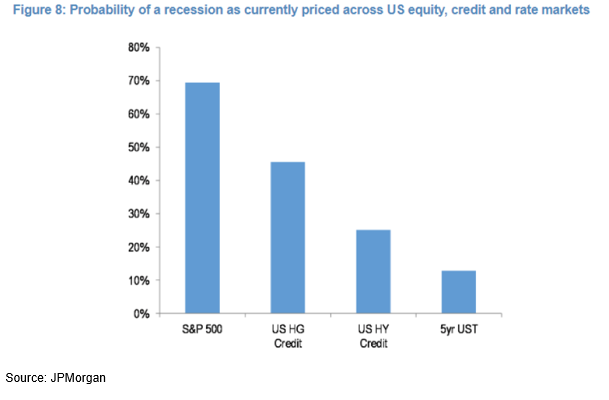

But the levels of S&P 500 speak to the excessive pessimism of stocks versus other asset classes. As this chart from JPMorgan shows, stocks have discounted a far higher chance of a recession:

- S&P 500 priced 70% chance

- High-yield 25%

- High-yield and equities are 80% correlated. So the gap means one of two things

It is either:

- Fed policy currently is far more negative for equities than bonds

- High-yield is about to get walloped

Either way, this means stocks are better than bonds.

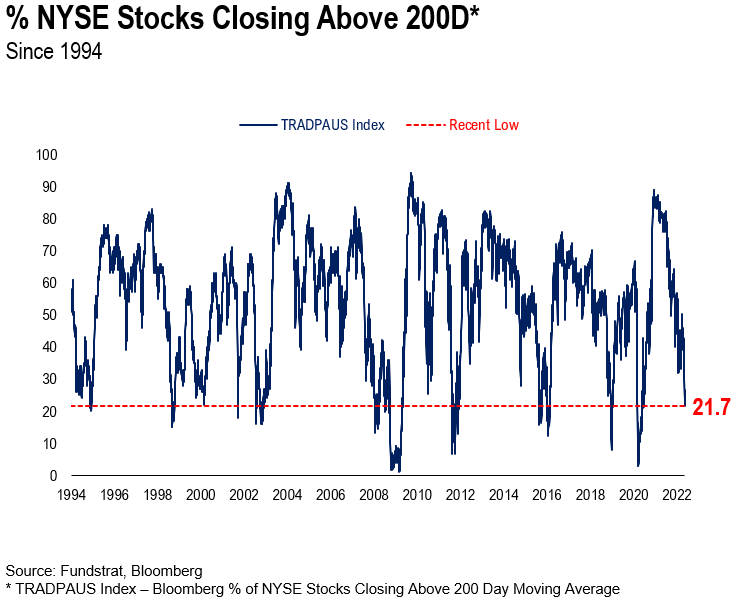

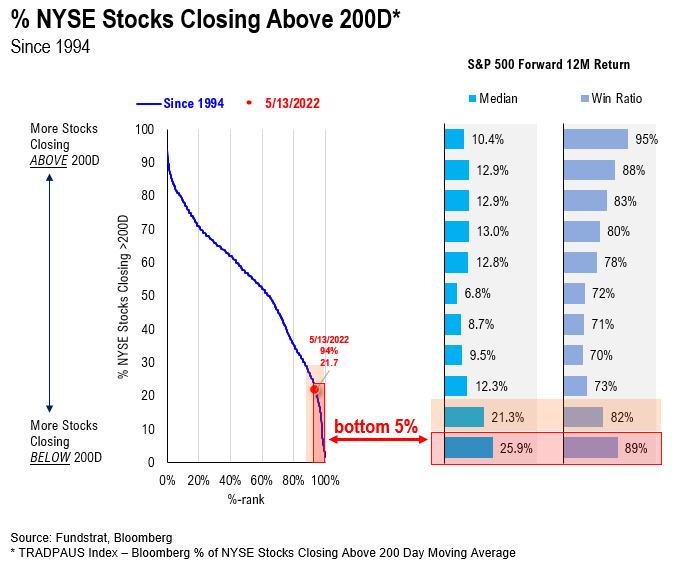

RISK-REWARD: 21% of stocks are above 200D moving average = 89% chance stocks higher in 12 months

The punishment in stocks has been so severe that on 5/13, only 21% of stocks were above their 200D moving average:

- since 1994, this is a bottom 6% reading

- this figure was lower in 2018 (soft landing) and 2022 (pandemic low)

- but DeMark analysis suggests the 2022 low might be “21%”

This is a bottom 6% reading. And as shown below, stocks historically have strong forward returns.

- median gain at bottom decile is 21% with 82% win ratio

- median gain at bottom percentiles (this is 6th) is 26% and win-ratio of 89%

- as this chart below highlights, the worse this level, the stronger the forward returns

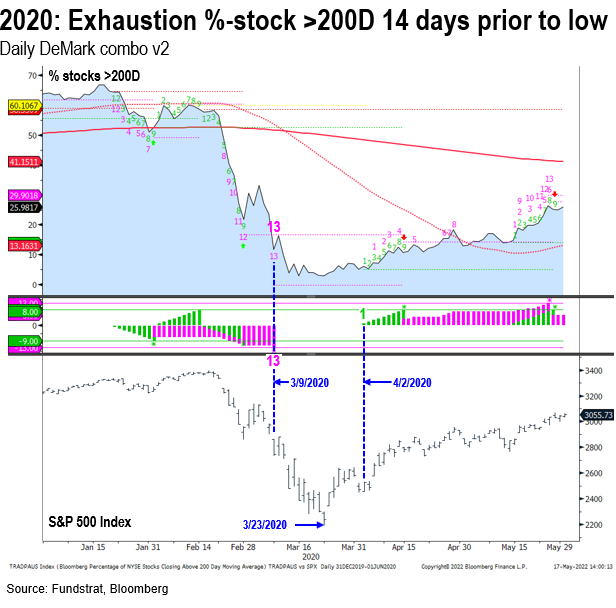

DeMark analysis suggests the “% below 200D” in 2022 might have bottomed at 21%

We like to use DeMark analysis, tools developed by Tom DeMark. By the way, we are hosting a webinar with DeMark this coming Thursday.

- the “13” buy setup, or exhaustion of trend, was triggered on 5/12/2022

- and since then on 5/13/2022, the “sequential” indicator turned green

- this suggests that this series might have established its bottom

- if this has bottomed, it raises odds the overall market has bottomed

In 2018 and 2020, this % stocks >200D bottomed and subsequent “green” confirmed bottoms

Take a look at 2018 and 2020 below, on the behavior of stocks >200D.

- the “13” was registered before the bottom (sign of a bottom near)

- green “1” confirmed the uptrend

- this was true in 2018 — bottom was 12/26/2018 and green “1” was 12/28

- this was true in 2020 — bottom was 3/23/2020 and green “1” was 4/2

…Take this to mean that stocks are not “hopeless” and a “basket case”

To me, this affirms what we have been saying. Stocks are offering good risk/reward here. While they have been horrific over the past 6 weeks, this doesn’t mean the next 6 weeks will be the same:

- moreover, consensus pundit after pundit says 10%-15% more downside ahead

- future is uncertain

- but it seems like many are positioned this way

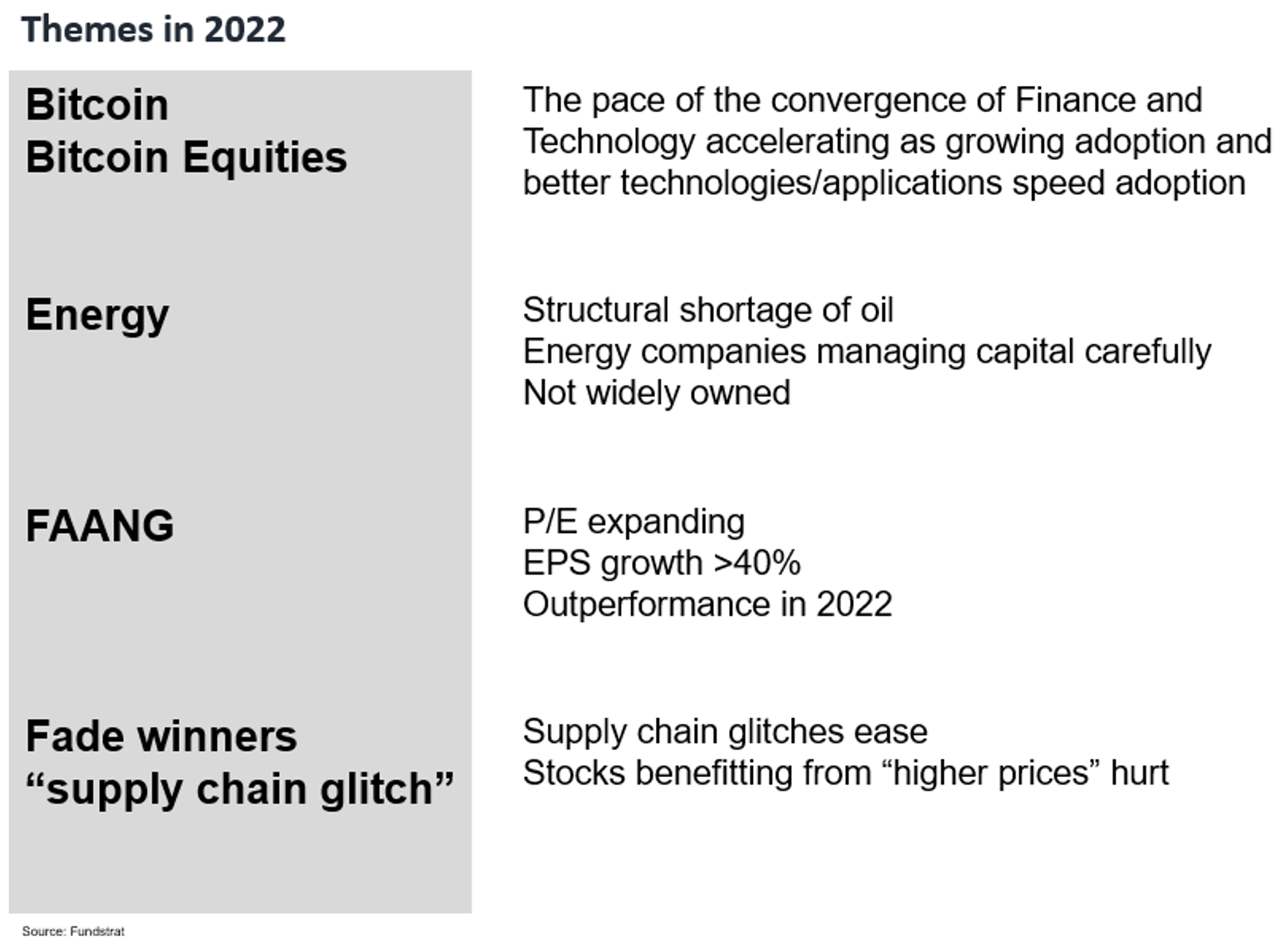

STRATEGY: We lean relatively “bullish” into 2H2022 (but also 2Q22), but warn of jagged next few months… Stick with BEEF

To recap on equity strategy, we are leaning bullish into 2Q2022.

Stocks have continued to be treacherous in 2022. Investors are on a hair trigger.

– this is in context to a challenging 1H2022

– so jagged next 3 months

Broadly, our existing sector strategy of BEEF remains valid. Even in war. Even with inflation. In fact, the last few weeks are strengthening the case for our “BEEF” strategy. That is, BEEF is

– Bitcoin + Bitcoin Equities BITO-1.10% GBTC-1.10% BITW-2.13%

– Energy

– FAANG FNGS-0.28% QQQ0.54%

Combined, it can be shortened to BEEF.

Why is this making stronger BEEF?

– Energy supply is now a sovereign priority

– this helps Energy stocks

– Ukraine and Russia both want access to alternative currencies

– this strengthens case for Bitcoin and bitcoin equities

– if Global economy slows, growth stocks lead

– hence, FANG starts to lead FB AAPL-1.86% AMZN-0.03% NFLX1.95% GOOG0.11%

All in all, one wants to be Overweight BEEF

_____________________________

31 Granny Shot Ideas: We performed our quarterly rebalance on 4/5. Full stock list here –> Click here

_____________________________

We publish on a 3-day a week schedule:

Monday

SKIP TUESDAY

Wednesday

SKIP THURSDAY

Friday

More from the author

Articles Read 1/2

🎁 Unlock 1 extra article by joining our Community!

Stay up to date with the latest articles. You’ll even get special recommendations weekly.

Already have an account? Sign In 1e4929-da9b02-2823d0-9b5c13-f6fc83

Already have an account? Sign In 1e4929-da9b02-2823d0-9b5c13-f6fc83